This Week in SaaS May 19 - 25, 2026

The top M&A deals, venture deals, news, and blog posts of the week

💻 AI Coding Bootcamp - June 22-25, 2026

Registration is open for the SaasRise AI Coding Bootcamp (June 22–25), a four-day live Zoom workshop teaching companies how to implement AI-first agentic engineering workflows with QA, testing, security, CI, and Claude Code best practices. Separate beginner and advanced tracks help founders, PMs, engineers, and CTOs accelerate R&D velocity 5–10x. Four hours per day. Apply to join here. We recommend enrolling at least two engineers and one product manager per company.

📚 New Blog Posts

- Setting up your Claude Code Development Environment

- Building an AI App with AI Coding

- Prototyping with Claude Code and Lovable

- Reading Existing Codebases with Claude Code

- Refactoring Your Existing SaaS App with Claude Code

- CEO Mastermind Recaps for the Week of May 18 - 21, 2026

💸 Big SaaS VC Rounds

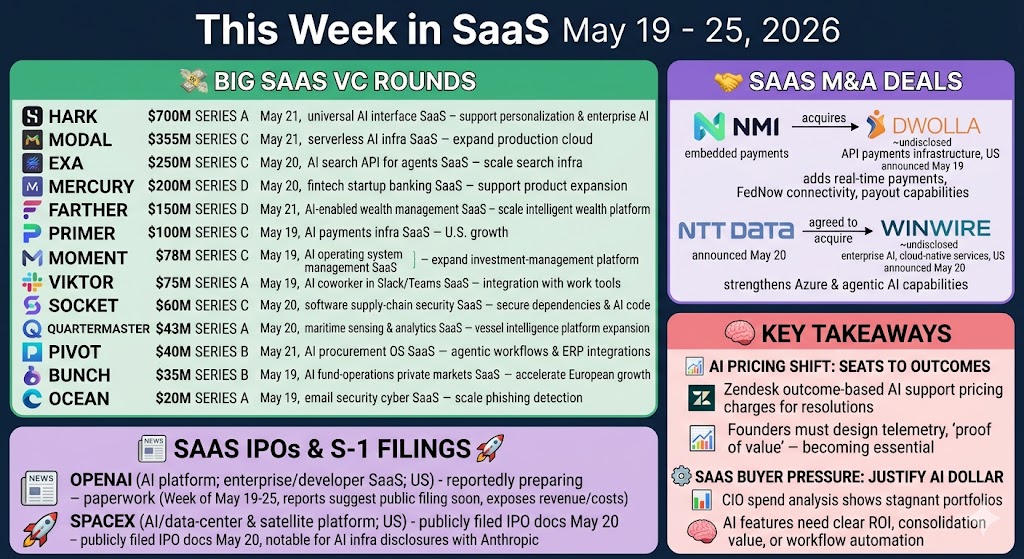

- Hark (universal AI interface; SaaS) – raised a $700M Series A on May 21; funds will support development of its personalized AI interface and enterprise-scale AI product expansion.

- Modal (serverless AI infrastructure platform; SaaS) – raised a $355M Series C on May 21; funds will expand its production cloud for AI, including infrastructure for AI-generated code, inference, and sandboxed workloads.

- Exa (AI search API and search engine for agents; SaaS) – raised a $250M Series C on May 20; funds will scale its search infrastructure for AI agents and developer adoption across AI-native applications.

- Mercury (business banking and finance platform for startups; fintech SaaS) – raised a $200M Series D on May 20; funds will support product expansion as Mercury positions itself as the operating bank for AI-era startups.

- Farther (AI-enabled wealth-management platform; fintech SaaS) – raised a $150M Series D on May 21; funds will scale its intelligent wealth platform for financial advisors and expand platform capabilities.

- Primer (AI-enabled payments infrastructure; fintech SaaS) – raised a $100M Series C on May 19; funds will expand its AI payments operating layer, develop Primer Companion, and accelerate U.S. growth.

- Moment (AI operating system for investment management; fintech SaaS) – raised a $78M Series C on May 19; funds will expand its AI investment-management platform for trading, compliance, and portfolio workflows.

- Viktor (AI coworker embedded in Slack and Microsoft Teams; SaaS) – raised a $75M Series A on May 19; funds will bring its AI coworker to more teams and deepen integrations across 3,000+ workplace tools.

- Socket (software supply-chain security platform; SaaS) – raised a $60M Series C on May 20; funds will help enterprises secure open-source dependencies and AI-generated code as software supply-chain risk rises.

- Quartermaster (maritime sensing and analytics platform; SaaS-enabled vertical AI) – raised a $43M Series A on May 20; funds will expand its SmartMast maritime-awareness network and real-time vessel intelligence platform.

- Pivot (AI procurement operating system; SaaS) – raised a $40M Series B on May 21; funds will scale agentic procurement workflows, deepen ERP and finance integrations, and expand enterprise adoption.

- bunch (AI-native fund-operations platform for private markets; fintech SaaS) – raised a $35M Series B on May 19; funds will accelerate European growth, deepen automation, and expand across geographies and asset classes.

- Ocean (AI-based email-security platform; cybersecurity SaaS) – raised a $20M Series A on May 19; funds will scale its agent-based phishing and social-engineering detection platform.

🤝 SaaS M&A Deals

- NMI completed the acquisition of Dwolla (~undisclosed; API-first account-to-account payments infrastructure, fintech SaaS, US) – announced on May 19; this acquisition adds real-time payments, FedNow connectivity, and payout capabilities to NMI’s embedded payments platform.

- NTT DATA agreed to acquire WinWire (~undisclosed; enterprise AI, data engineering, and cloud-native software services, US) – announced on May 20; this acquisition strengthens NTT DATA’s Microsoft Azure, agentic AI, and cloud-transformation capabilities.

🚀 SaaS IPOs & S-1 Filings

- OpenAI (AI platform; enterprise and developer SaaS; US) – reportedly prepared IPO paperwork during the week of May 19–25, with reports indicating a possible filing within days or weeks; a public filing would expose revenue, compute costs, risk factors, and AI platform economics at unprecedented scale.

- SpaceX (AI/data-center and satellite infrastructure; software-enabled platform; US) – publicly filed IPO documents on May 20; while not a pure-play SaaS company, the filing was notable for AI infrastructure disclosures, including cloud-compute arrangements with Anthropic.

🧠 Key Takeaways

- AI pricing is shifting from seats to outcomes. Zendesk’s new outcome-based AI support pricing charges only for verified resolutions, signaling that AI-agent monetization may increasingly depend on measurable work completed rather than user count or token volume. Founders should design pricing telemetry early, because “proof of value” is becoming part of the product.

- SaaS buyers are pressuring vendors to justify every AI dollar. CIO’s analysis of SaaS spend highlights that enterprise software portfolios are not expanding much even as spend rises, meaning AI features need clear ROI, consolidation value, or workflow automation to avoid budget scrutiny.

📰 Community News

- Apply to join the SaasRise community for SaaS CEOs and Founders with $1M+ in ARR

- Apply to join the GrowthRise community for B2B Marketing Leaders

- Join Pulse, our AI-curated tech news reader, to see the latest SaaS, AI, and tech news and deals

See you next week with the next edition ofThis Week in SaaS.

-Ryan Allis, CEO of SaasRise