The first quarter of 2026 was defined by a single paradox: the SaaS industry experienced its most significant market disruption since the 2022 rate-hike correction, yet M&A activity remained remarkably resilient. While the "SaaSpocalypse" triggered by Anthropic's Claude Cowork launch on January 12, 2026 erased approximately $1 trillion in aggregate SaaS market capitalization and compressed public multiples from ~7.0x to ~5.5x, dealmakers kept writing checks. The quarter saw an estimated 620+ SaaS transactions worth over $95 billion in aggregate SaaS and software deal value (excluding non-SaaS mega-deals), headlined by Google's $32 billion acquisition of Wiz, Palo Alto Networks' $25 billion purchase of CyberArk, and Thoma Bravo's $12.3 billion take-private of Dayforce.

If you enjoy data-driven in-depth research like this on SaaS and AI, apply to join the community here. You can see the full research report below.

Table of Contents

- Executive Summary: Q1 2026 at a Glance

- The Macro Context: SaaSpocalypse Meets Record M&A

- Deal Volume & Aggregate Value

- Revenue Multiples: The New Pricing Reality

- Sector Breakdown & Multiples by Category

- The Rule of 40: The Defining Metric

- Geographic Analysis

- Buyer Dynamics: Strategic vs. Private Equity

- Table: All Q1 2026 SaaS Deals $1B+

- Table: All Q1 2026 SaaS Deals $100M–$999M

- Three Case Studies: The Most Interesting Deals

- Outlook: What Comes Next

- Sources & Methodology

1. Executive Summary: Q1 2026 at a Glance

Q1 2026 was the quarter where fear and fundamentals collided head-on. On one side, the SaaSpocalypse sent shockwaves through public SaaS markets after Anthropic launched Claude Cowork — an autonomous AI agent capable of performing many tasks previously handled by SaaS applications — on January 12, 2026. Investor panic erased approximately $1 trillion in aggregate market capitalization from enterprise SaaS stocks within weeks. HubSpot fell 48%. Salesforce dropped 25%. The BVP Nasdaq Emerging Cloud Index plunged to its lowest level since 2020.

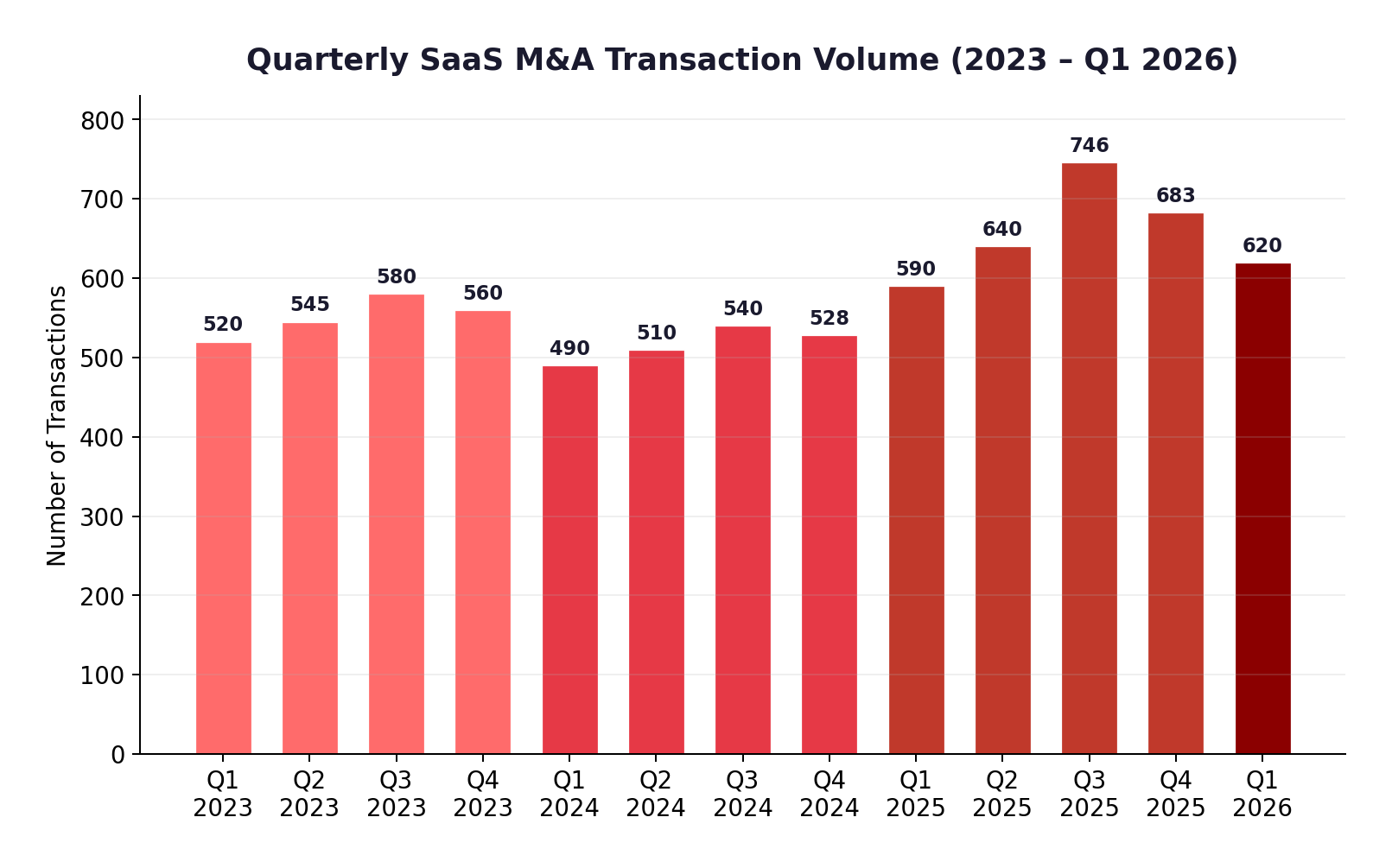

On the other side, the M&A market barely flinched. Private equity firms, flush with over $2.5 trillion in dry powder, saw the public selloff as an unprecedented buying opportunity. Strategic acquirers — particularly in cybersecurity, AI infrastructure, and financial services — continued executing on multi-year acquisition strategies. The result: an estimated 620+ SaaS-specific M&A transactions in Q1 2026, maintaining the elevated pace set during 2025's record year of 2,698 deals (per Software Equity Group).

The broader software M&A market was even more dramatic. Berkery Noyes reported 443 total software transactions in Q1 2026, with an aggregate value of $287.2 billion — a 3x increase from Q4 2025's $83 billion. However, this headline figure was massively inflated by SpaceX's $250 billion acquisition of xAI on February 2, 2026 — the largest corporate merger in history by valuation, but not a SaaS transaction. Strip out that single deal, and the quarter's software M&A was solid but not extraordinary, roughly in line with 2025's pace.

2. The Macro Context: SaaSpocalypse Meets Record M&A

To understand Q1 2026's M&A landscape, you need to understand the two forces that defined the quarter:

The SaaSpocalypse (January 12, 2026)

When Anthropic launched Claude Cowork — an AI agent that could autonomously handle complex multi-step workflows previously requiring dedicated SaaS applications — the market reaction was swift and brutal. Within weeks, approximately $1 trillion in aggregate market capitalization was erased from enterprise SaaS stocks. Public SaaS multiples compressed from approximately 7.0x to 5.5x EV/Revenue. Individual stocks were hit even harder: HubSpot fell 48%, as investors feared that AI agents could replace CRM workflows; Salesforce dropped 25%; and many mid-cap SaaS companies saw even steeper declines.

The narrative was straightforward: if AI could autonomously perform the tasks that SaaS companies charged monthly subscriptions for, what was the long-term value of those subscriptions? The panic was real, even if the full impact of AI on SaaS business models will take years to unfold.

The Record M&A Backdrop

Simultaneously, the broader M&A market was experiencing its most active quarter in nearly two decades. Total completed deal value across all sectors hit $438 billion — a five-year high and 155% increase year-over-year. The quarter featured 12 mega-deals valued at $10 billion or more, the highest volume of such massive transactions since 2008. Global M&A surpassed $1.2 trillion for the quarter.

Several factors drove this surge: stabilizing interest rates (with the Fed expected to reach 3.00–3.25% in 2026), record private equity dry powder exceeding $2.5 trillion, and the SaaSpocalypse itself creating a unique buying window where high-quality SaaS assets were suddenly available at discounted public multiples.

Generative AI also fueled record venture capital activity. S&P Global Market Intelligence reported that generative AI companies attracted a record $145 billion in venture capital funding in Q1 2026 alone — though two megadeals accounted for nearly 98% of that total: OpenAI's $122 billion round (first announced at ~$110B in February, closing at $122B on March 31) and xAI's $20 billion round in January. This concentration of capital in a handful of AI platforms is reshaping the competitive landscape for every SaaS company, as the largest AI players accumulate resources that dwarf the market capitalization of many mid-cap SaaS companies.

Key Insight: The SaaSpocalypse created what may prove to be a generational buying opportunity. Public SaaS companies trading at 5.5x revenue or lower — with strong retention, AI integration capabilities, and Rule of 40+ profiles — became prime take-private targets for PE firms that could buy at a discount and sell once sentiment normalizes.

3. Deal Volume & Aggregate Value

Despite the market turbulence, SaaS M&A transaction volume in Q1 2026 remained strong, continuing the elevated pace established during 2025's record year.

Software Equity Group's 2026 Annual SaaS Report confirmed that 2025 set the all-time record with 2,698 SaaS M&A transactions, a 28% increase over 2024's 2,107 deals. SaaS accounted for approximately 58% of total software M&A activity. Q3 2025 was the peak quarter with 746 deals — a 26% year-over-year increase — driven by pent-up demand and stabilized interest rates.

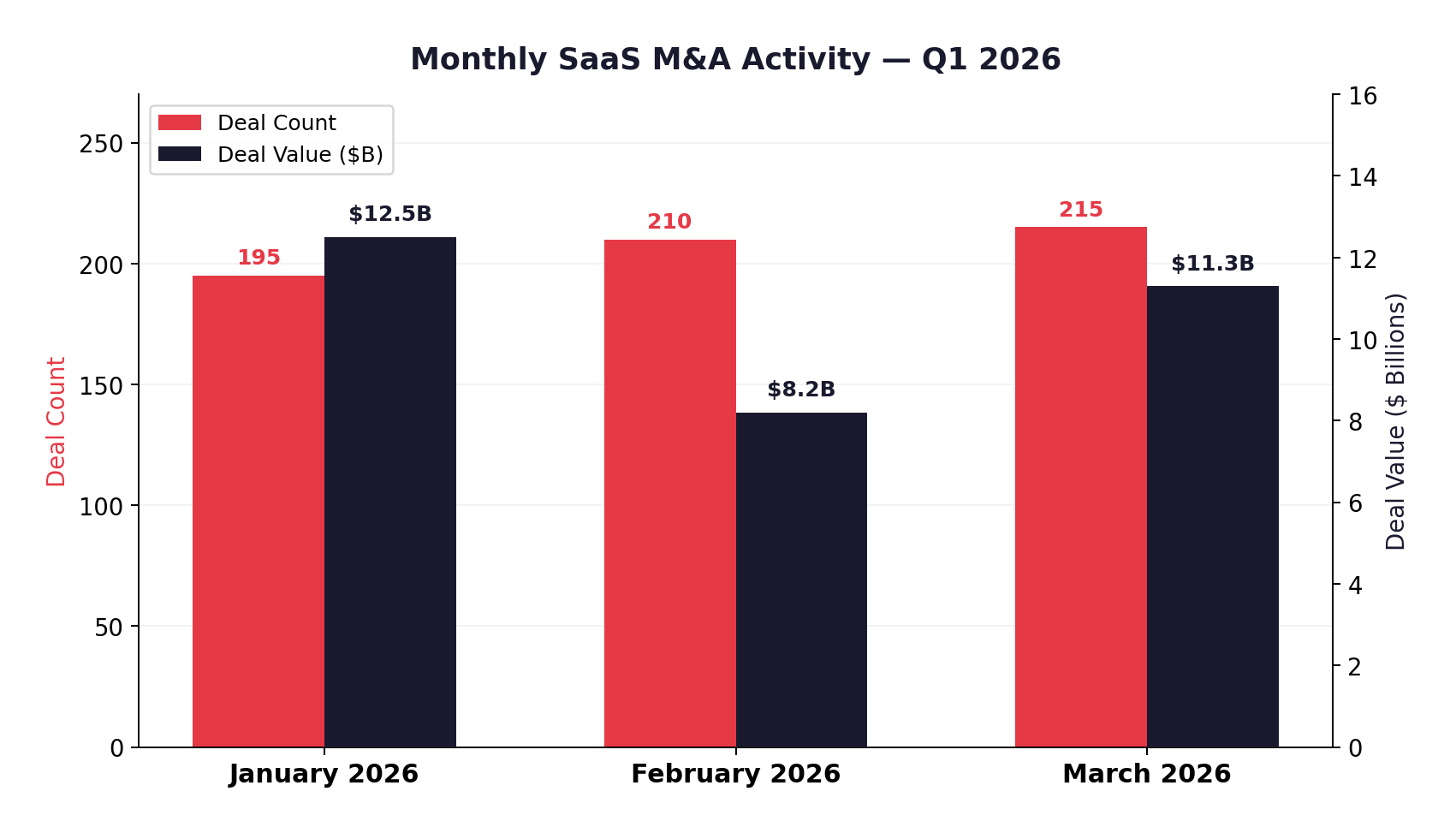

Q1 2026 saw an estimated 620+ SaaS transactions, a slight sequential decline from Q4 2025 but still above Q1 2025 levels. The modest quarterly dip reflected two factors: the uncertainty caused by the SaaSpocalypse temporarily pausing some processes, and the natural seasonal pattern where Q1 typically trails Q3-Q4 deal volumes.

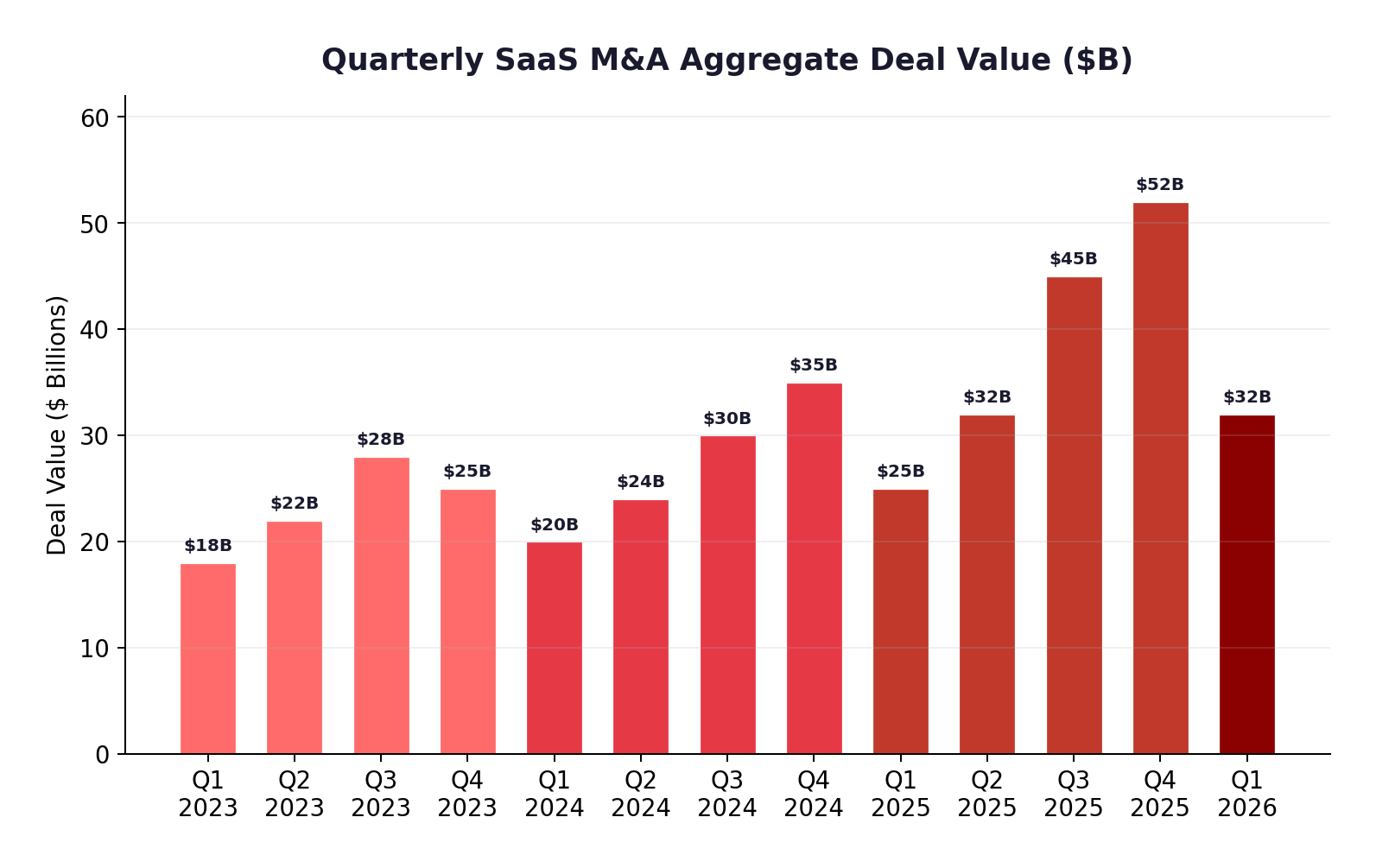

Aggregate deal value tells a more dramatic story. Berkery Noyes reported $287.2 billion in total software M&A value for Q1 2026, more than tripling Q4 2025's $83 billion. However, this was almost entirely driven by SpaceX's $250 billion acquisition of xAI. Excluding that single transaction, software M&A value was approximately $37 billion — healthy, but more in line with 2025's quarterly averages.

For SaaS and software specifically, we estimate aggregate deal value of approximately $95 billion+ in Q1 2026, headlined by Google/Wiz ($32B), Palo Alto/CyberArk ($25B), Thoma Bravo/Dayforce ($12.3B), IBM/Confluent ($11B), Clearwater Analytics ($8.4B), ServiceNow/Armis ($7.75B), and at least a dozen more billion-dollar transactions. This represents the most active quarter for software M&A deal value since 2021.

4. Revenue Multiples: The New Pricing Reality

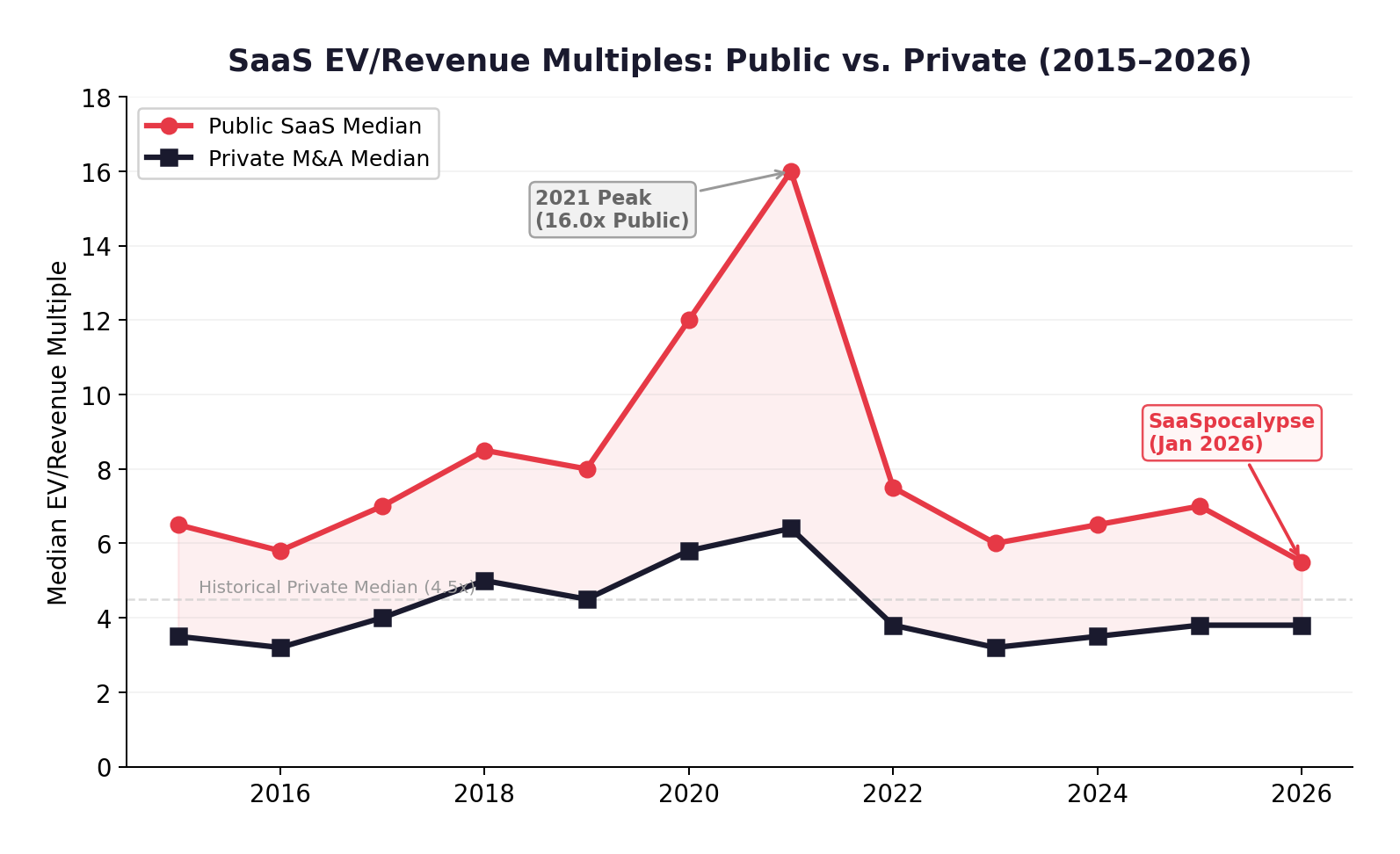

Q1 2026 marked a significant inflection point for SaaS valuations. The SaaSpocalypse compressed public multiples, and the ripple effects are beginning to reach private markets — though private valuations remain more resilient than their public counterparts.

Public SaaS Multiples

As of March 2026, the median public SaaS EV/Revenue multiple stood at approximately 5.5x, down from roughly 7.0x at the end of 2025. This represents a 21% compression in just three months — the sharpest quarterly decline since the 2022 rate-hike correction. According to Windsor Drake's Q1 2026 SaaS M&A Report, the public SaaS index traded at approximately 7.0x on a trailing basis, though forward multiples were closer to 5.0–5.5x.

Notably, for the first time since Aventis Advisors began tracking in 2015, U.S. SaaS companies no longer trade at a premium to global SaaS — a major structural shift reflecting the concentrated AI disruption fears around American-headquartered enterprise software companies.

Private SaaS Multiples

Private SaaS M&A multiples have been more stable, though the data reveals meaningful variation depending on the source and dataset. Aventis Advisors reported the median private EV/Revenue multiple at 3.1x as of March 2026, based on their tracked universe of 543 transactions (2015–2026), where the historical median is 4.5x. However, that figure includes a long tail of very small transactions and appears to understate multiples for the $20M+ ARR segment that drives most deal value.

SaasRise's own 2026 M&A Report found median private SaaS exit multiples of approximately 3.8x, up from 2.9x in 2024, with bootstrapped SaaS businesses around 4.8x and VC-backed SaaS around 5.3x. AI-native or top-quartile vertical SaaS businesses commanded significantly higher multiples, reaching 9x–12x for the best assets. Windsor Drake reported a private median of 5.3x on a trailing basis, reflecting their dataset's tilt toward larger, higher-quality transactions.

The takeaway: the "true" median private SaaS multiple in Q1 2026 is best expressed as a range of 3.8x–5.3x, depending on deal size, company quality, and dataset composition. Small-deal and all-inclusive datasets produce lower medians (~3.1x–3.8x), while datasets focused on transactions above $20M in enterprise value produce higher medians (~4.8x–5.3x). AI-native, security, and top-quartile Rule of 40 companies trade well above any of these medians.

The Public-Private Gap Is Narrowing. With public SaaS multiples compressing to 5.5x and private medians at 3.8–5.3x, the traditional public premium has shrunk dramatically. This creates fertile ground for PE take-private strategies: buy public companies at depressed multiples, improve operations, and exit when sentiment recovers. Expect more Dayforce/Smartsheet-style deals in Q2-Q3 2026.

EV/EBITDA: The New Standard

A critical shift in Q1 2026: EV/EBITDA multiples are rapidly becoming the primary valuation metric for SaaS, supplanting the revenue-based multiples that dominated for the past decade. Aventis Advisors noted this was "something that was almost never said before" in SaaS. Their SaaS index currently trades at approximately 26.6x EBITDA — fairly reasonable by historical standards and broadly in line with traditional economy businesses. This shift reflects the market's insistence on profitability over growth-at-all-costs, a trend accelerated by the SaaSpocalypse.

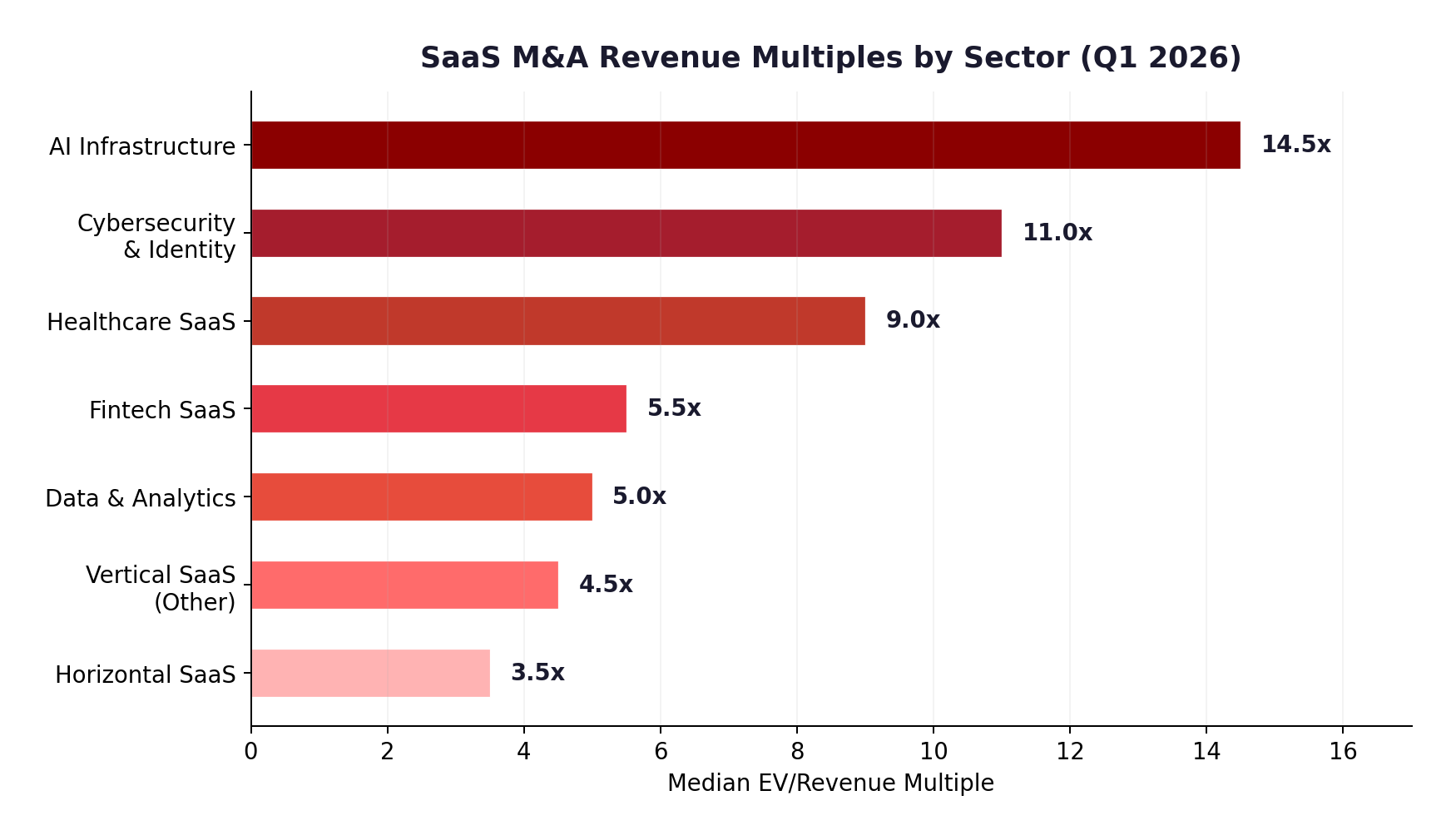

5. Sector Breakdown & Multiples by Category

Not all SaaS is created equal — and Q1 2026 made that more apparent than ever. The valuation dispersion between sectors has reached historic highs, with a nearly 4x spread between the highest and lowest-valued sectors.

AI Infrastructure: 14.5x (Premium)

AI-native infrastructure companies command an approximately 85% premium over legacy infrastructure, per Windsor Drake. These are the "pick-and-shovel" businesses of the AI era: data labeling, model training platforms, AI observability, and compute orchestration. The premium reflects both scarcity value and the belief that AI infrastructure will be the most durable layer of the technology stack.

Cybersecurity & Identity: 11.0x

Cybersecurity remained the single largest category by deal value in 2025, accounting for over $70 billion across deals like Google/Wiz ($32B) and Palo Alto/CyberArk ($25B). Q1 2026 continued this trend at high multiples, as AI-generated threats increase the urgency for advanced security solutions. Berkery Noyes reported 111 cybersecurity M&A deals in Q3 2025 alone.

Healthcare SaaS: 9.0x

Vertical SaaS in healthcare continues to command premium multiples, driven by deep regulatory moats, high switching costs, and large addressable markets. Thoma Bravo's $5.3 billion acquisition of ModMed in 2025 set the benchmark for the sector.

Fintech SaaS: 5.5x

Fintech SaaS maintained mid-range multiples, supported by deep regulatory moats and complex integration requirements. Capital One's $5.15B acquisition of Brex and Permira/Warburg Pincus's $8.4B Clearwater Analytics deal both reflect the enduring value of financial infrastructure software. Brink's $6.6B acquisition of NCR Atleos — while more fintech infrastructure than pure SaaS — underscores that financial services technology commands consistent buyer interest regardless of market sentiment.

Horizontal SaaS: 3.5x

At the other end of the spectrum, commodity horizontal SaaS — generic CRM, basic project management, simple customer support tools — faces the most severe compression. These are the categories most directly threatened by AI agents, as Claude Cowork and similar products can increasingly handle the workflows these tools address. Multiples for this category are at or below 2023 lows. Windsor Drake's Q1 2026 data confirms that mature horizontal SaaS compressed toward historical means of 5–6x for public companies and even lower for private transactions, while top-quartile AI and security platforms commanded 11x–15x premiums — a sharp bifurcation that is unlikely to narrow anytime soon.

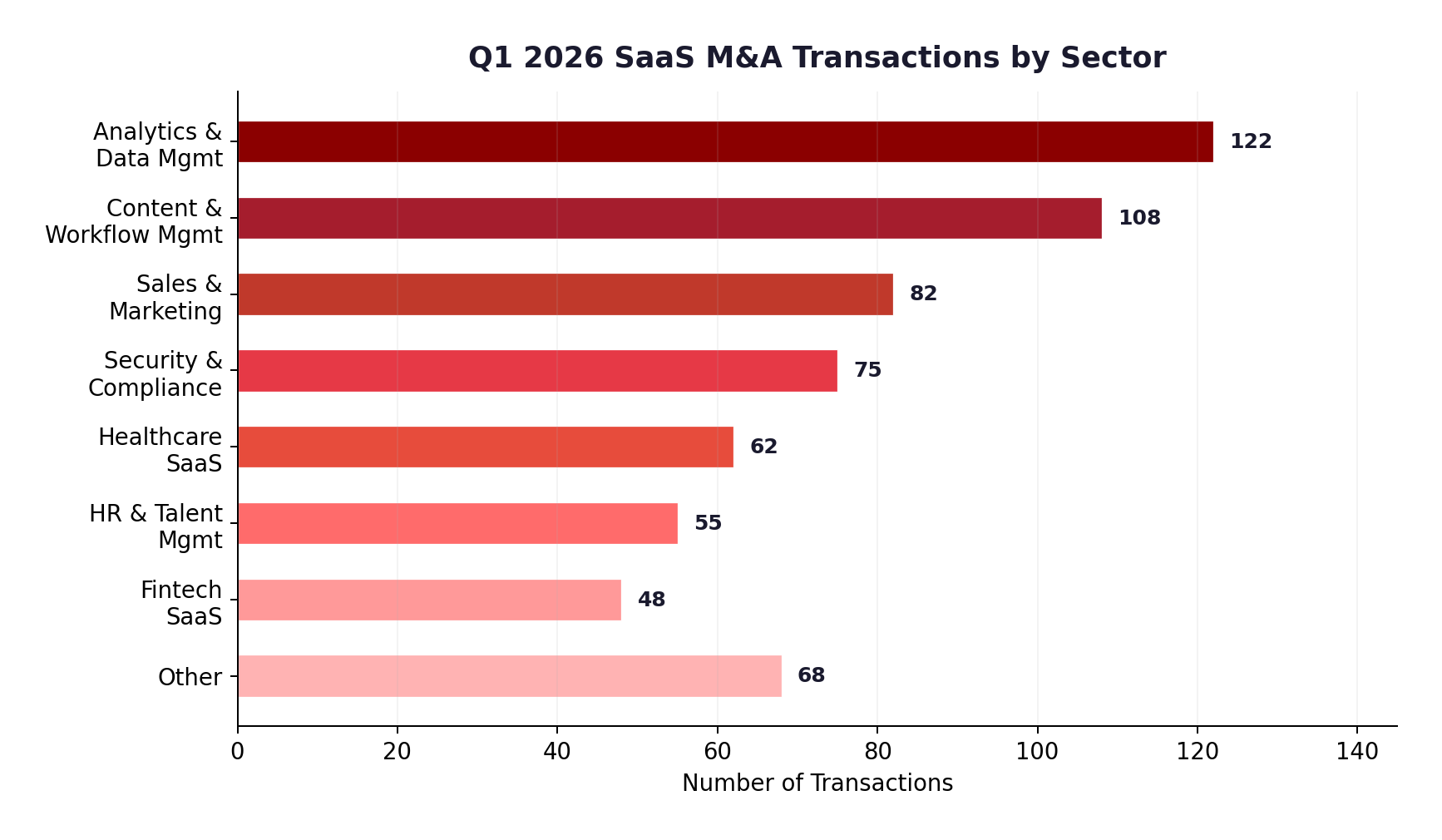

By transaction count, Analytics & Data Management and Content & Workflow Management were the two most active SaaS M&A product categories, together accounting for nearly 38% of total SaaS deal volume — consistent with the trend observed throughout 2025. Sales & Marketing also remained active, though deal counts declined from Q3 2025's peak of 100 transactions to an estimated 82 in Q1 2026.

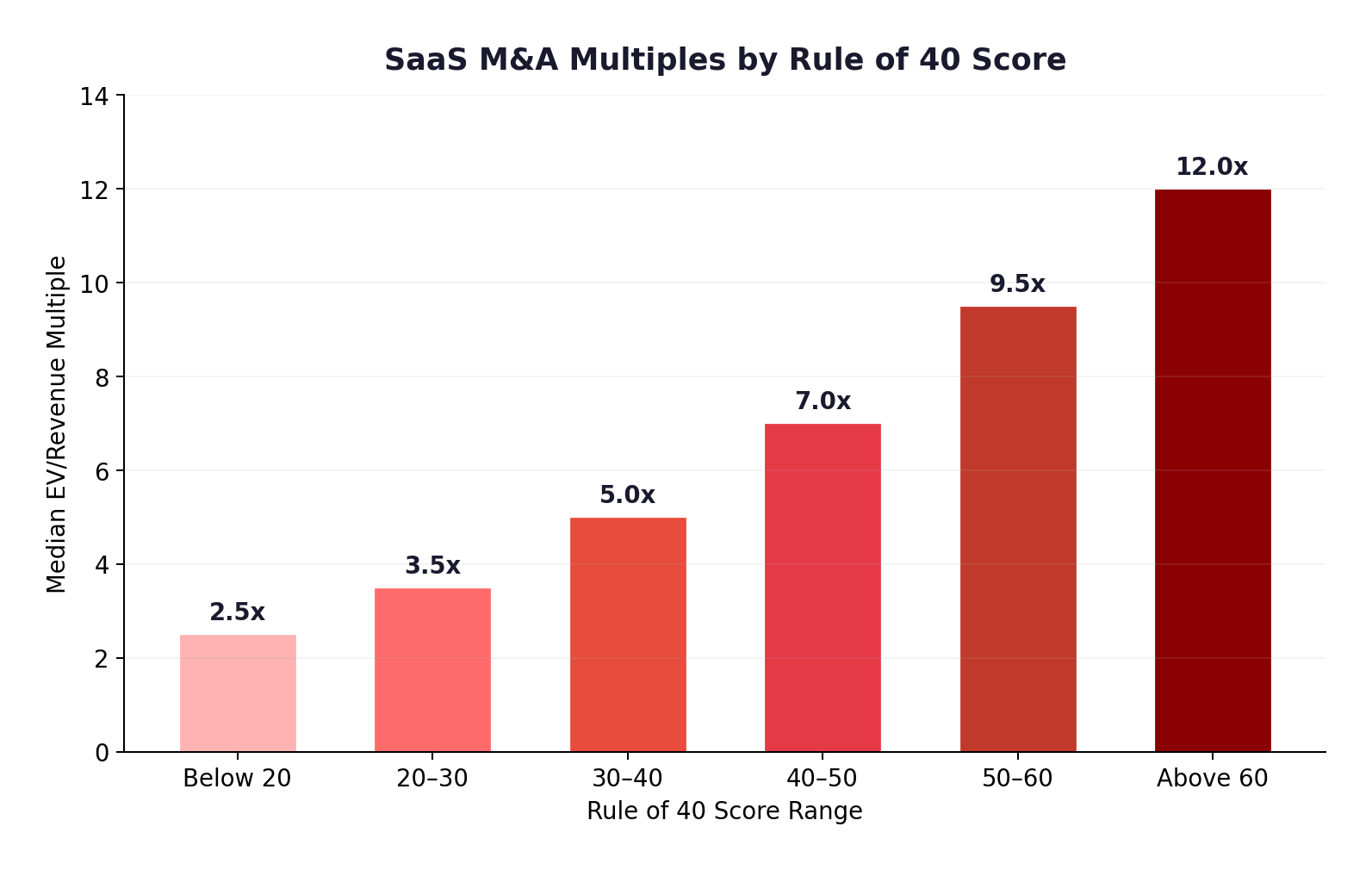

6. The Rule of 40: The Defining Metric

The Rule of 40 — the sum of a company's revenue growth rate and EBITDA margin — has become the single most important predictor of valuation multiples in Q1 2026. The data is unambiguous: companies scoring above 40 attract dramatically higher multiples than those below.

The relationship is steep and nearly linear:

- Below 20: 2.5x median multiple — these are distressed or declining businesses

- 20–30: 3.5x — below-market performers

- 30–40: 5.0x — at-market, "average" SaaS companies

- 40–50: 7.0x — premium valuations, strong buyer interest

- 50–60: 9.5x — elite companies, competitive auction processes

- Above 60: 12.0x+ — rare, top-quartile assets commanding premium multiples

Companies scoring above 40 attract premium valuations and stronger investor interest, while those below 40 face lower multiples and tougher fundraising or exit negotiations. In Q1 2026, the bar has effectively risen: Rule of 40+ combined with a credible AI integration strategy is the new minimum for commanding premium multiples.

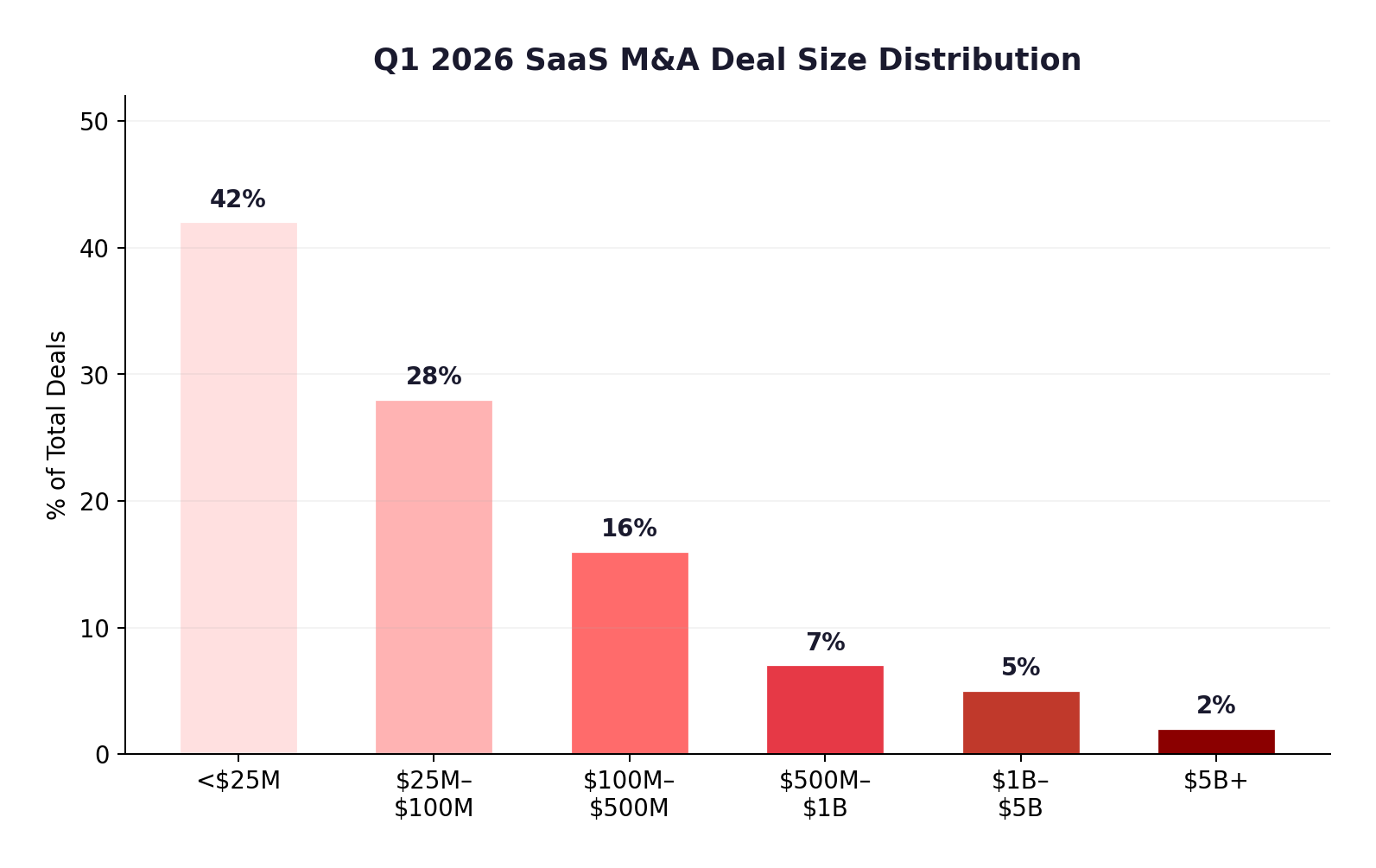

For Founders Considering an Exit: The data shows that deal size is the single strongest predictor of valuation multiples — the median multiple was nearly 2x higher for deals in the $50–100M range vs. $20–50M. Combined with Rule of 40 performance, this means that growing to scale before selling is more important than ever. Competitive processes with multiple interested buyers also produce meaningfully better outcomes than passive or founder-led conversations.

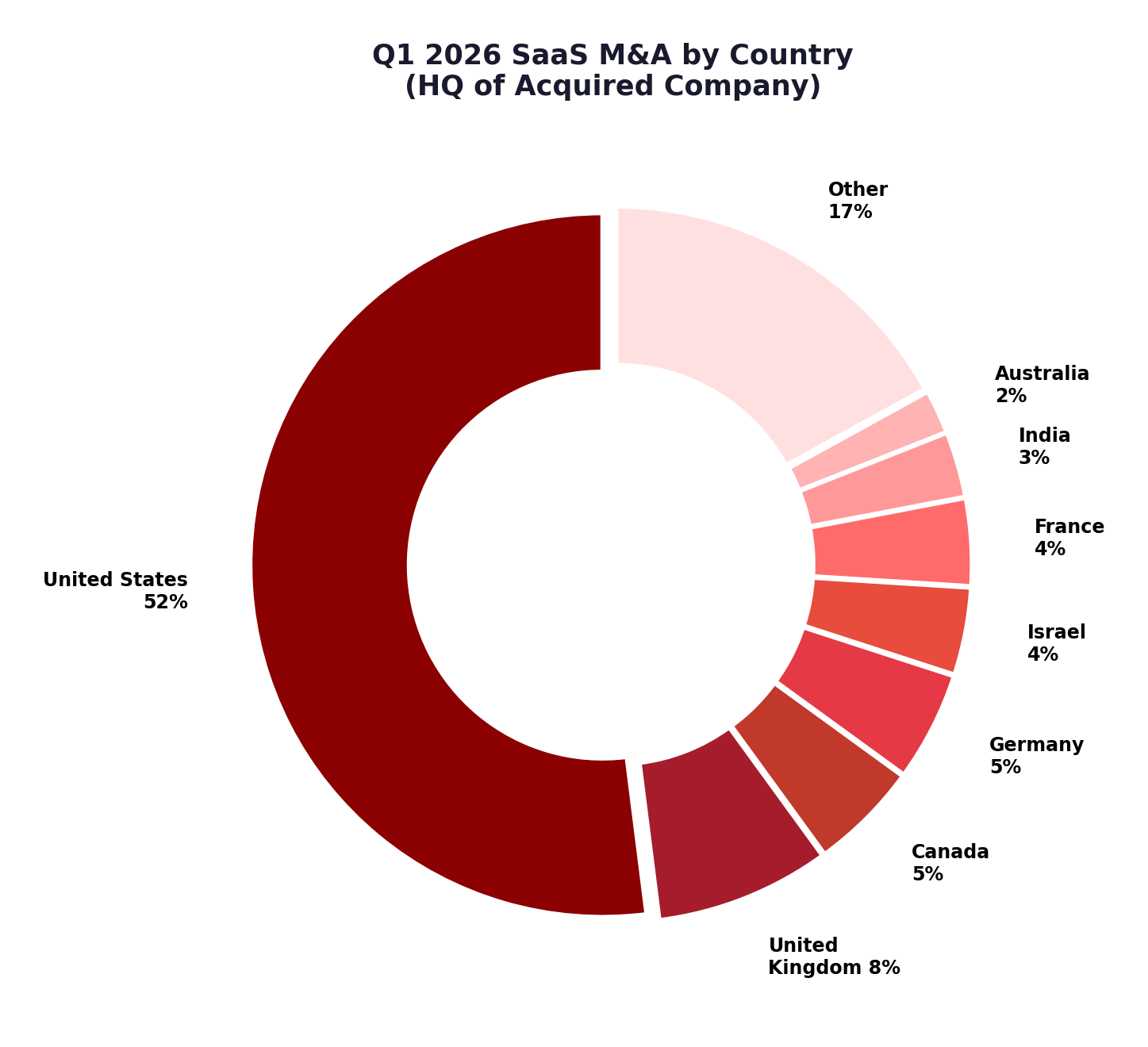

7. Geographic Analysis

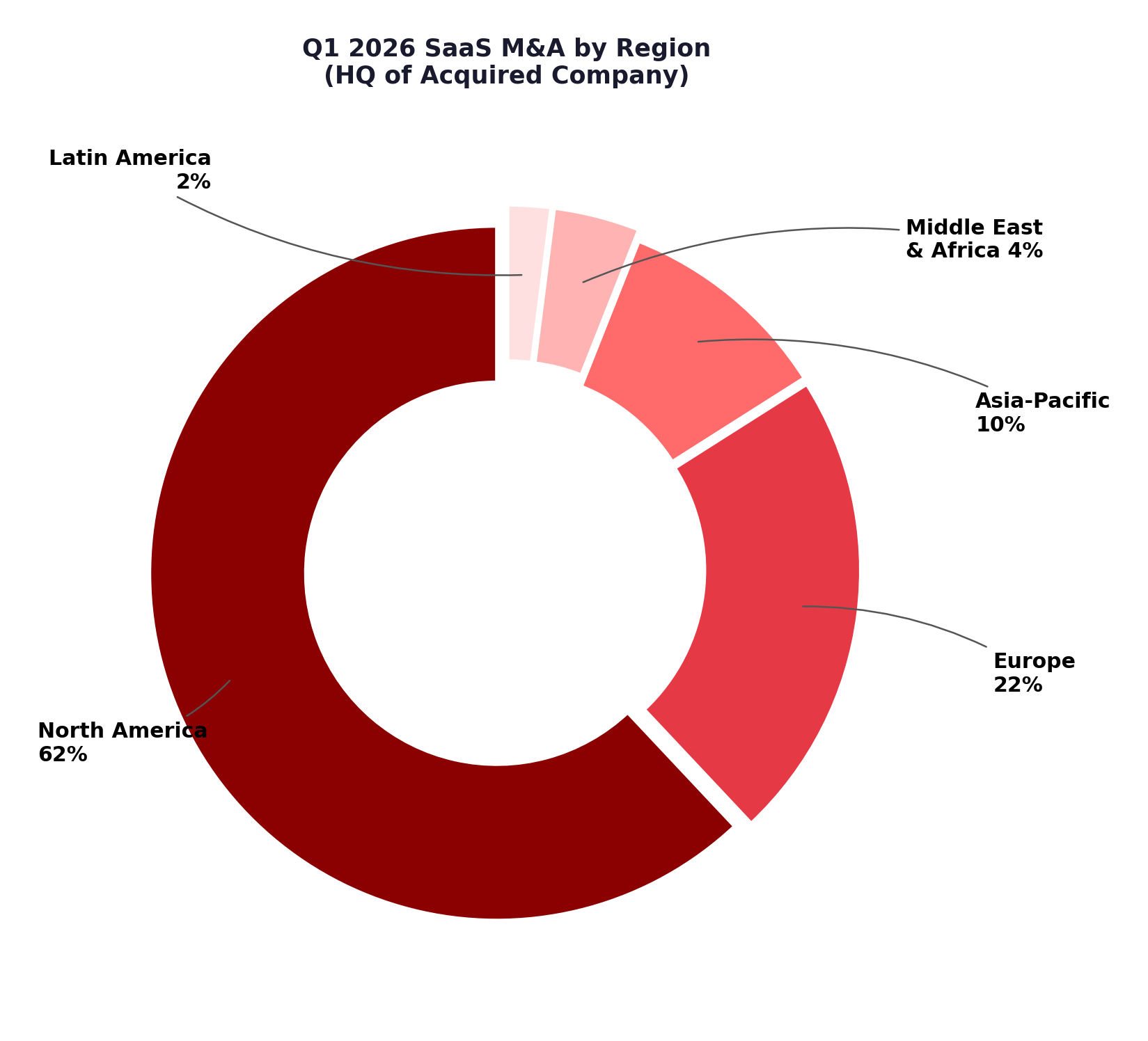

North America continued to dominate SaaS M&A activity in Q1 2026, though European and Asian-Pacific deals showed notable growth.

North America (62%) remained the dominant geography for both deal volume and value, led by the United States (52% of global deals). The U.S. SaaS market's depth, favorable regulatory environment, and concentration of both buyers and sellers continues to make it the center of gravity for global SaaS M&A.

Europe (22%) saw continued consolidation activity, led by the UK (8%), Germany (5%), and France (4%). Notable Q1 2026 European deals included team.blue's triple acquisition of Windsor.ai (Switzerland), Storyclash (Austria), and Saleskit (Czech Republic), as well as Hg's $6.4 billion take-private of OneStream (a US company, but Hg is a London-based PE firm investing from its European-focused Saturn Fund).

Asia-Pacific (10%) saw growing activity, particularly in India, where private equity and venture capital investment climbed to $7.19 billion in Q1 2026, up from $4.57 billion in Q1 2025. The number of Indian PE/VC deals grew to 296 from 291, and the median deal value rose to $3.8 million from $3 million — reflecting strengthening structural fundamentals and a deepening corporate technology ecosystem. Israel (4%) continued punching well above its weight in the SaaS M&A landscape, with notable transactions including PayPal's acquisition of Cymbio (estimated at hundreds of millions) and Base's acquisition of EverAfter AI (~$20M). Israeli tech exits below $20M reached $363M across 120 deals in 2025, sharply up from $128M in 79 deals the prior year.

Middle East & Africa (4%) and Latin America (2%) remained smaller markets by deal count, though Saudi Arabia's Savvy Games Group made headlines with its $6B acquisition of Moonton — a gaming rather than SaaS transaction, but indicative of the region's growing appetite for technology acquisitions. The Middle East's sovereign wealth funds (ADIA, GIC, Temasek) are also increasingly active as co-investors in Western SaaS take-privates, providing scale capital that enables larger deal sizes.

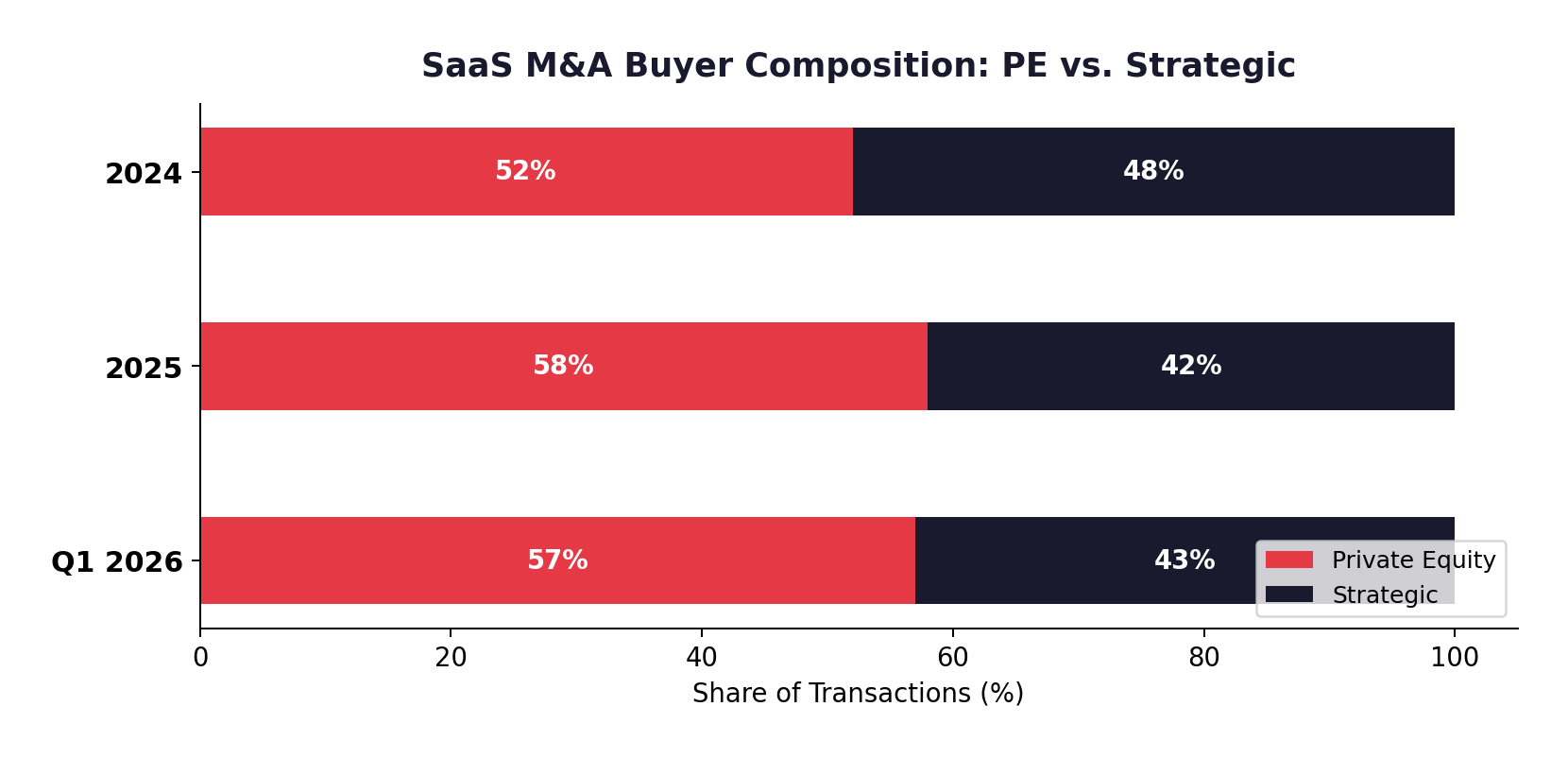

8. Buyer Dynamics: Strategic vs. Private Equity

Q1 2026 continued 2025's trend of PE-heavy deal activity. Private equity buyers were involved in nearly 57% of all SaaS transactions, making it one of the most sponsor-heavy periods on record.

Private Equity: The Dominant Force

PE firms are executing three primary strategies in Q1 2026:

- Take-Privates: The SaaSpocalypse created a unique window to buy public SaaS companies at depressed multiples. Hg's $6.4B OneStream deal (31% premium) and Thoma Bravo's $12.3B Dayforce acquisition (32% premium) exemplified this approach. Permira and Warburg Pincus's $8.4B Clearwater Analytics take-private (announced Dec 2025, expected to close H1 2026) is another example, with a 47% premium to the pre-leak share price.

- Platform Buy-and-Build: Add-on acquisitions dominated PE activity, accounting for approximately 72% of total PE deal volume. This reflects the persistent "buy-and-build" strategy across fragmented vertical SaaS markets — healthcare IT, legal tech, GovTech — to achieve scale and drive valuation multiple expansion.

- Profitability Pivot: PE firms are heavily scrutinizing targets for unit economics, prioritizing companies with EBITDA margins above 15% or clear paths to profitability within 12 months.

Strategic Acquirers: AI-Driven Urgency

Corporate strategic buyers (43% of deals) remained selective but aggressive when they found the right targets. The AI imperative drove acquisitions: companies like Salesforce (which acquired Momentum in February 2026), Flexera (which completed a double acquisition of ProsperOps and Chaos Genius in January 2026), and Apollo.io (which acquired Pocus in March 2026) were all adding AI-native capabilities to existing platforms.

Thoma Bravo continued to dominate as the single most active PE buyer in SaaS. In 2025 alone, the firm executed seven transactions over $1 billion, including the acquisitions of PROS Holdings, Verint Systems, Dayforce, itel, Olo, Hornetsecurity, and Boeing's Digital Aviation Solutions. Orlando Bravo, the firm's founder, described it as "the hardest I've ever worked in 30 years of being in private equity." With more than $181 billion in assets under management as of September 2025, Thoma Bravo's scale allows it to pursue the largest SaaS take-privates while simultaneously executing multiple mid-market deals. Valsoft ranked as the most active strategic buyer in SaaS by deal count for the second consecutive year.

Deal Structure Trends

Several notable deal structure patterns emerged in Q1 2026:

- All-cash take-privates dominate mega-deals: Both Thoma Bravo/Dayforce ($12.3B) and Hg/OneStream ($6.4B) were structured as all-cash transactions, reflecting PE firms' access to debt financing and the desire to move quickly. Goldman Sachs provided Thoma Bravo with a $6 billion debt package ($5.5B term loan + $500M revolving credit facility) for the Dayforce deal alone.

- Go-shop periods remain standard: Clearwater Analytics included a 45-day go-shop period ending January 23, 2026, during which the company was permitted to solicit competing bids. Go-shop provisions have become expected in take-private transactions, giving boards legal protection and occasionally generating superior offers.

- Sovereign wealth co-investment rising: The Abu Dhabi Investment Authority (ADIA) participated as a minority investor in the Dayforce take-private. Temasek and Francisco Partners supported the Clearwater Analytics deal. Sovereign wealth funds are increasingly providing co-investment capital alongside traditional PE sponsors, enabling larger deal sizes and sharing risk.

- Hybrid cash-and-stock for strategic acquirers: Capital One/Brex ($5.15B, 50/50 cash/stock) and Brink's/NCR Atleos ($6.6B, cash + stock + debt assumption) used mixed consideration, reflecting the desire of strategic buyers to preserve balance sheet flexibility while offering sellers upside through equity participation.