The SaaS M&A Market in 2026: What the “SaaSpocalypse” Really Means for Founders

A founder-focused analysis of what the 2026 SaaS M&A market really means, why the market is splitting between strong and vulnerable companies, and what buyers still value most in an AI-shaped environment.

If you’re a SaaS founder trying to make sense of the market in 2026, the headlines are not especially helpful.

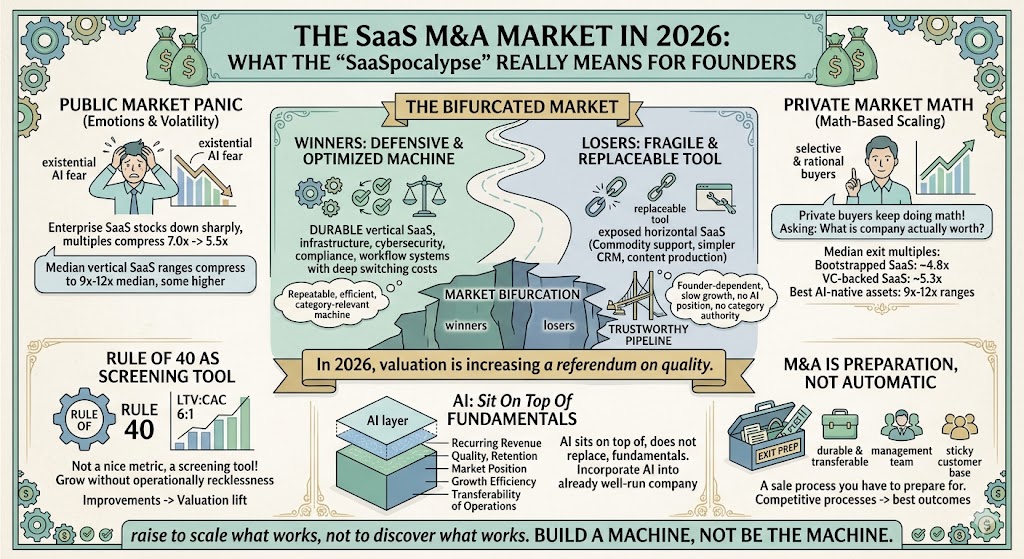

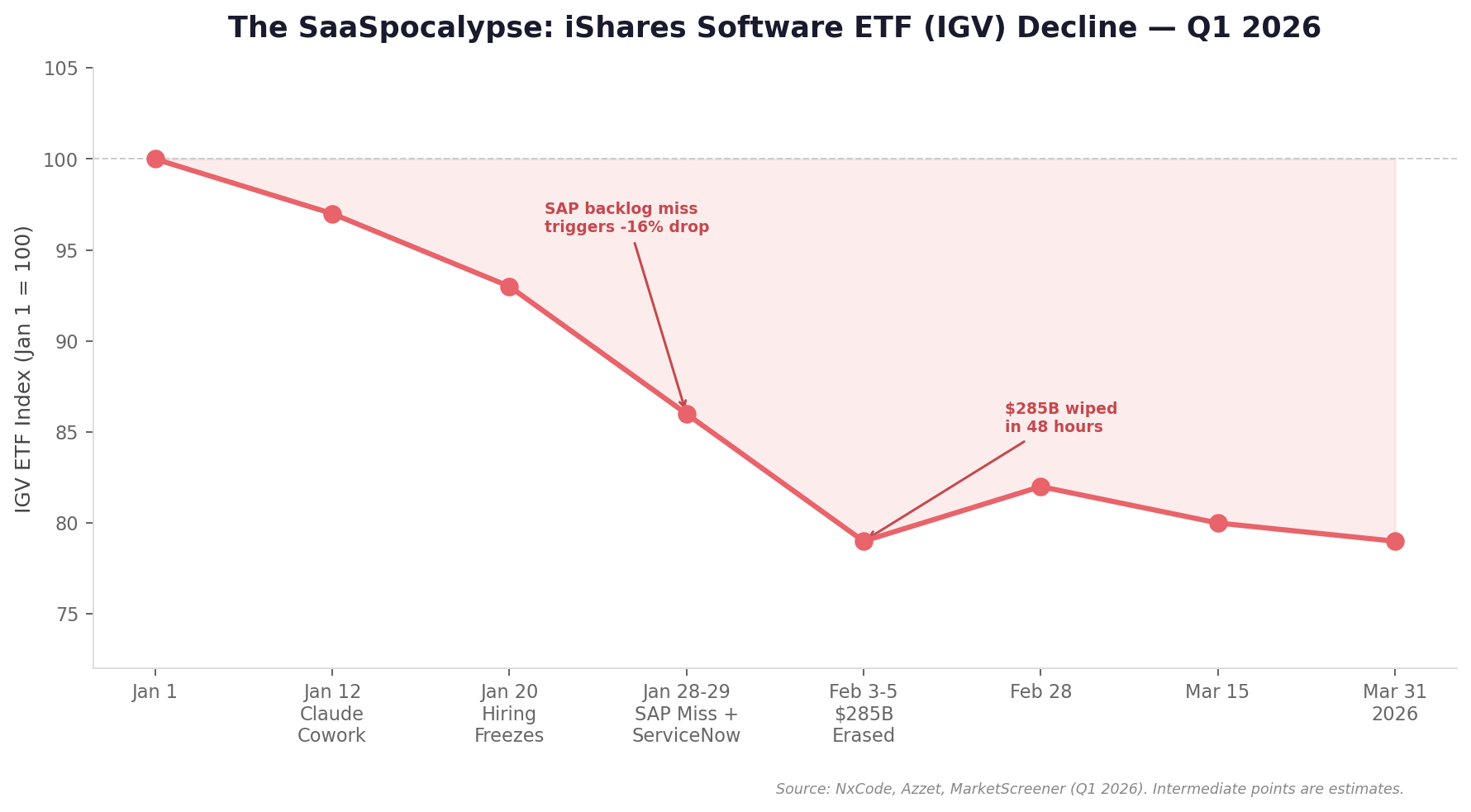

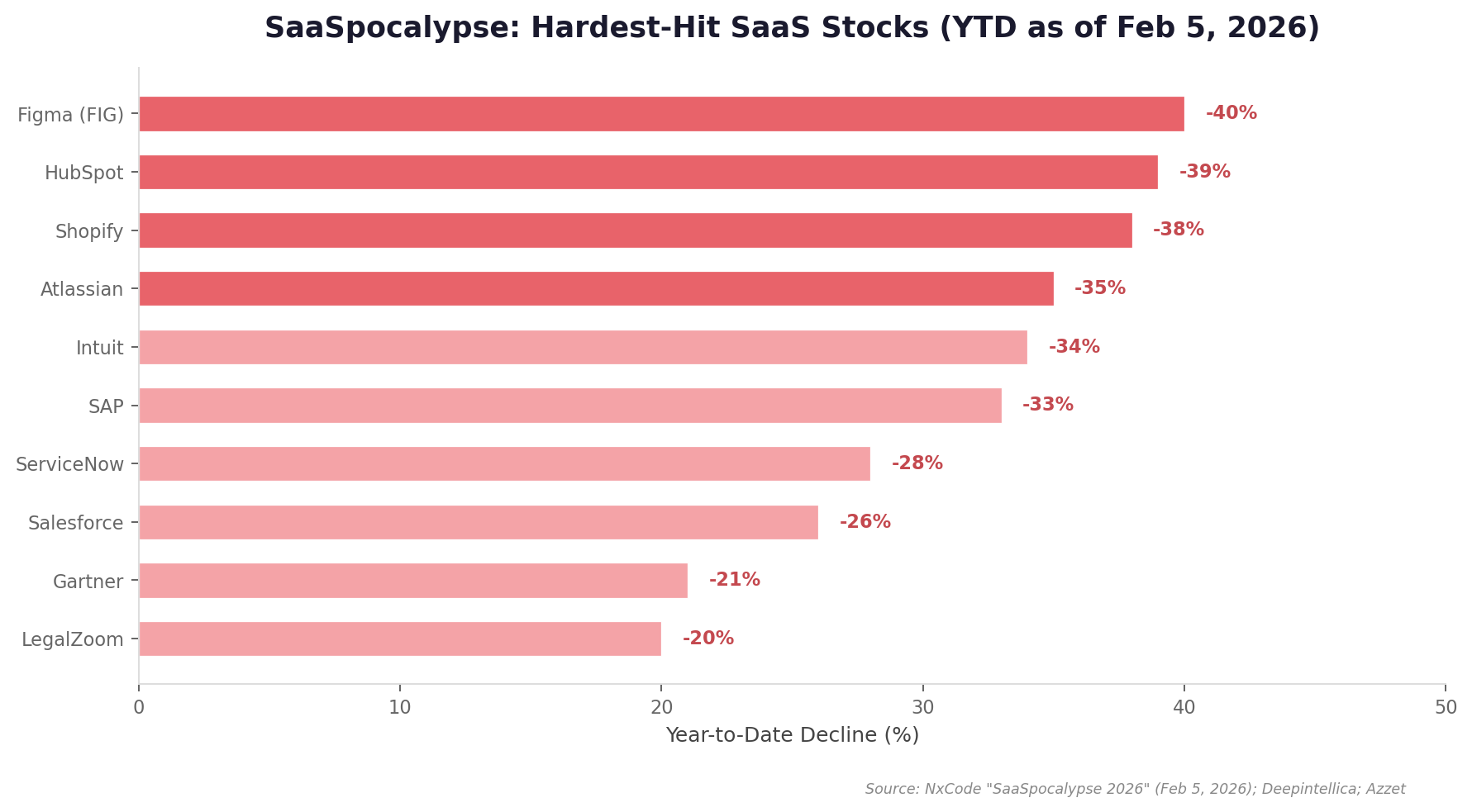

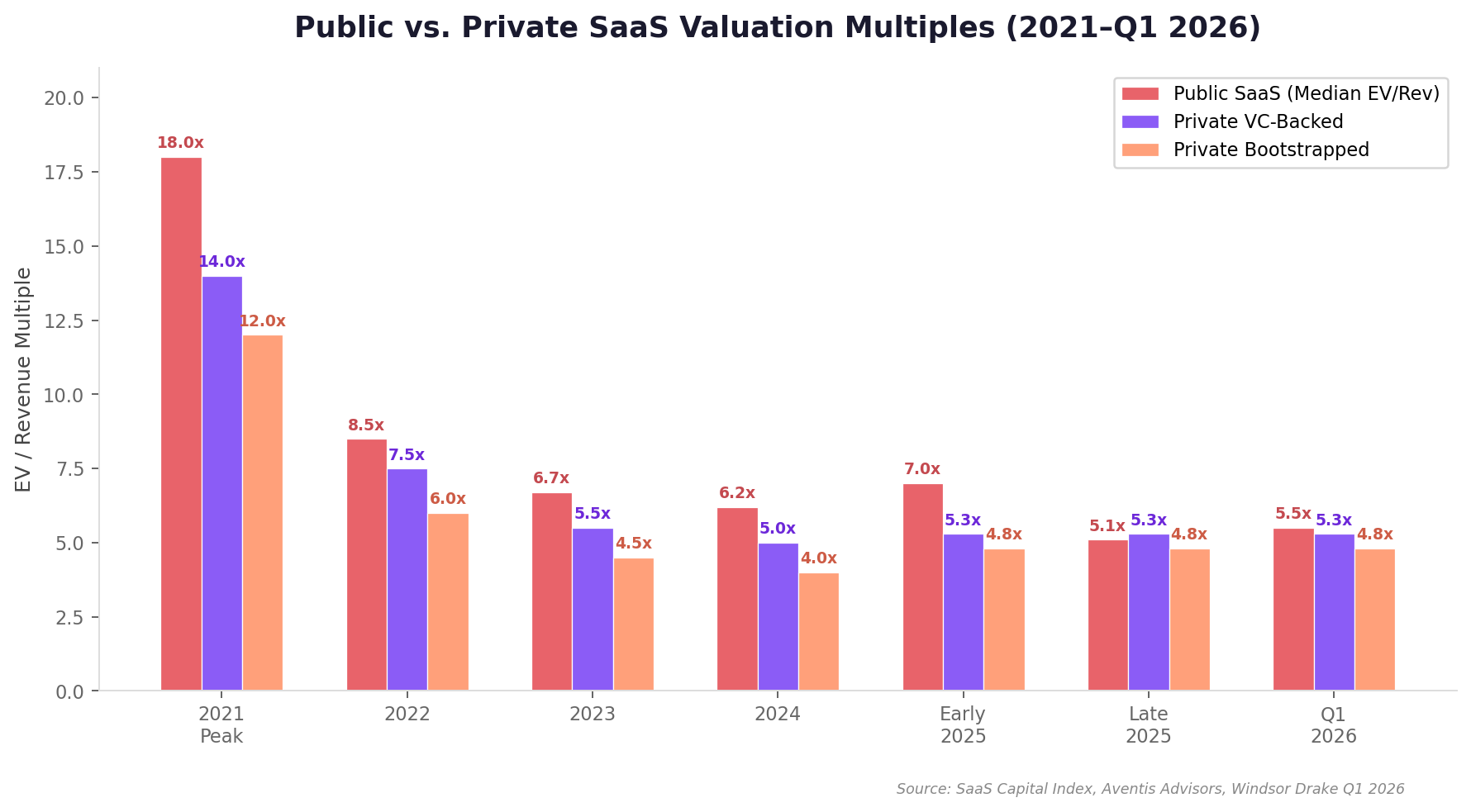

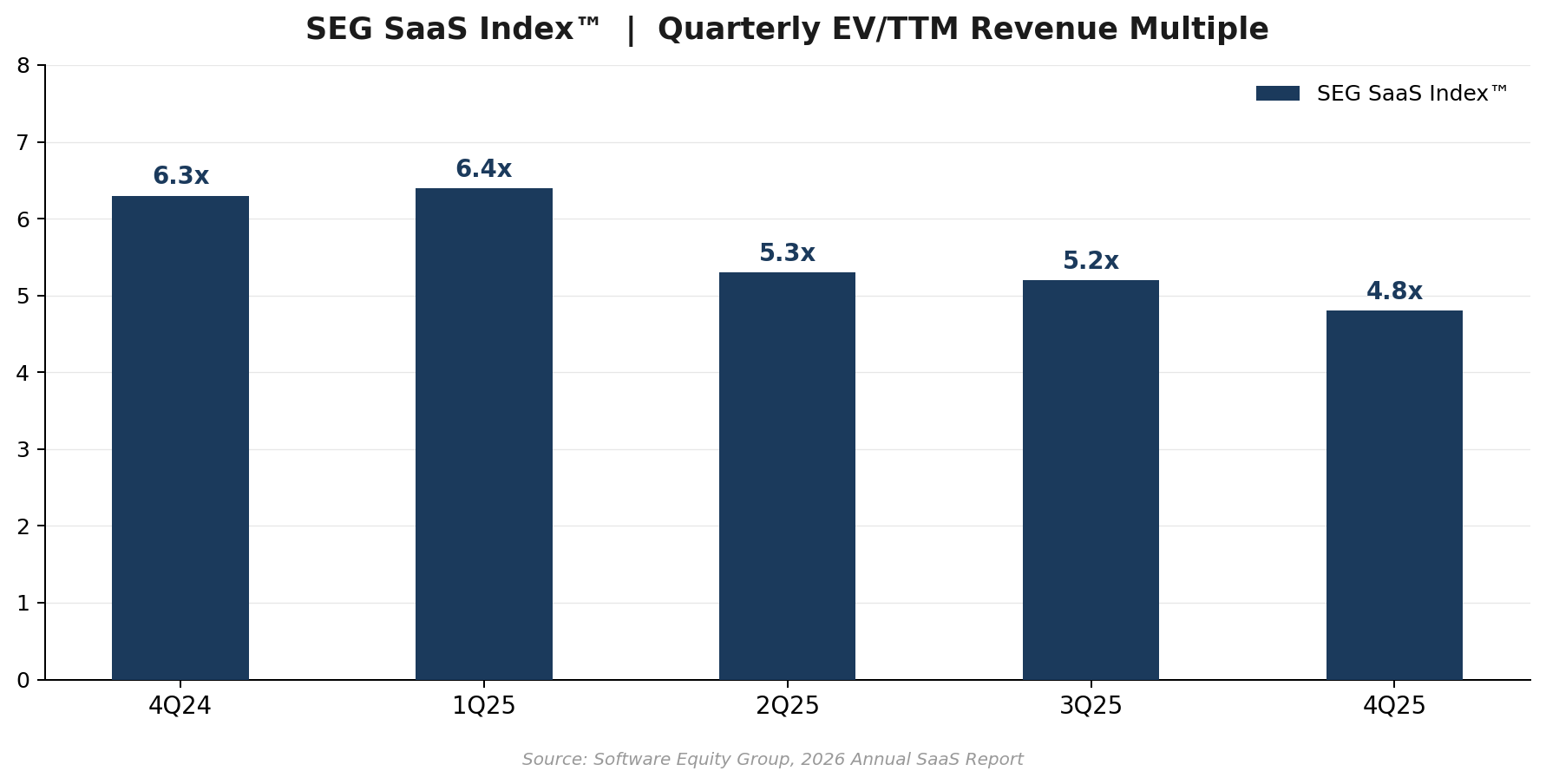

On one side, you have panic. Public software stocks sold off hard. AI launches triggered existential fear across large parts of the SaaS market. Commentators started throwing around terms like “SaaSpocalypse,” and suddenly every founder was supposed to believe that software as a category had entered a structural decline. The report you shared captures that mood well: after Anthropic’s Claude Cowork launch on January 12, 2026, enterprise SaaS stocks sold off sharply, around $1 trillion in aggregate market cap was erased, and public SaaS multiples compressed from roughly 7.0x to 5.5x.

On the other side, you have what buyers and operators are actually doing.

And that story is more interesting.

Because under the fear, the market has not frozen. It has become more selective. More rational in some areas. More brutal in others. The M&A market remained active through 2025, with more than $180 billion in announced SaaS deal value and 17 mega-deals above $2.5 billion. Private buyers did not disappear. Strategic acquirers did not disappear. High-quality companies did not suddenly become worthless.

What changed is that the market now cares a lot more about what kind of SaaS company you built.

That distinction is everything.

For founders, 2026 is not really a story about whether SaaS is alive or dead. It is a story about separation. The market is dividing between software businesses that feel durable and software businesses that feel replaceable. Between companies that look transferable and companies that still look founder-dependent. Between firms that can explain their place in an AI-shaped future and firms that are hoping buyers won’t ask too many questions.

That is the real takeaway.

And if you are building toward a large outcome, this can actually be clarifying.

As I’ve said in another context, “build a machine, not be the machine.” That idea matters even more in a market like this, because what buyers are purchasing is not just your current revenue. They are purchasing confidence in future revenue.

The public market panicked, but the private market kept doing math

One of the most useful things in your report is the contrast between public volatility and private behavior. Public investors moved fast and emotionally. Private buyers, as they usually do, asked a slower and more practical question: what is this company actually worth if I own it and operate it?

That leads to a very different lens.

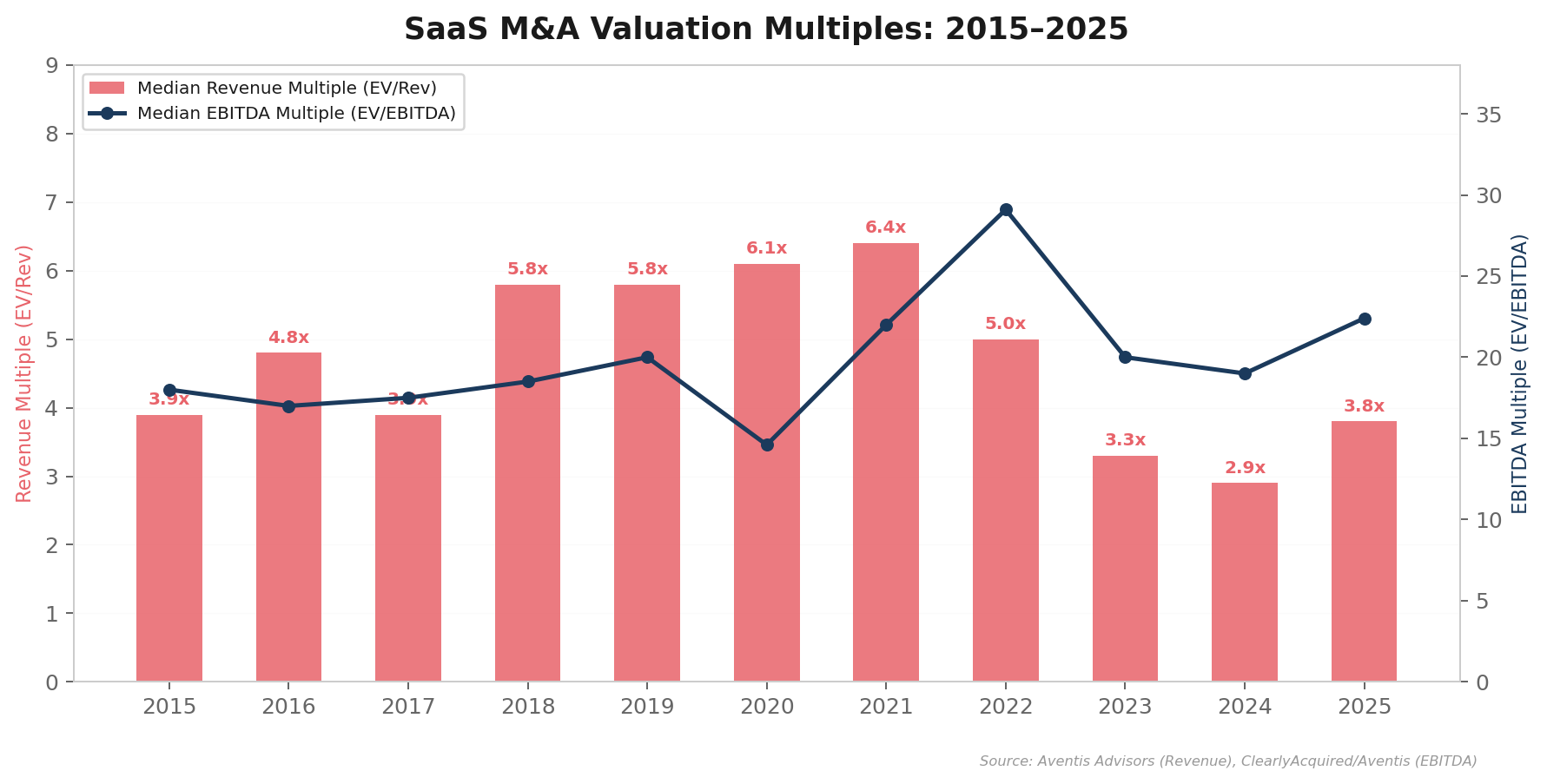

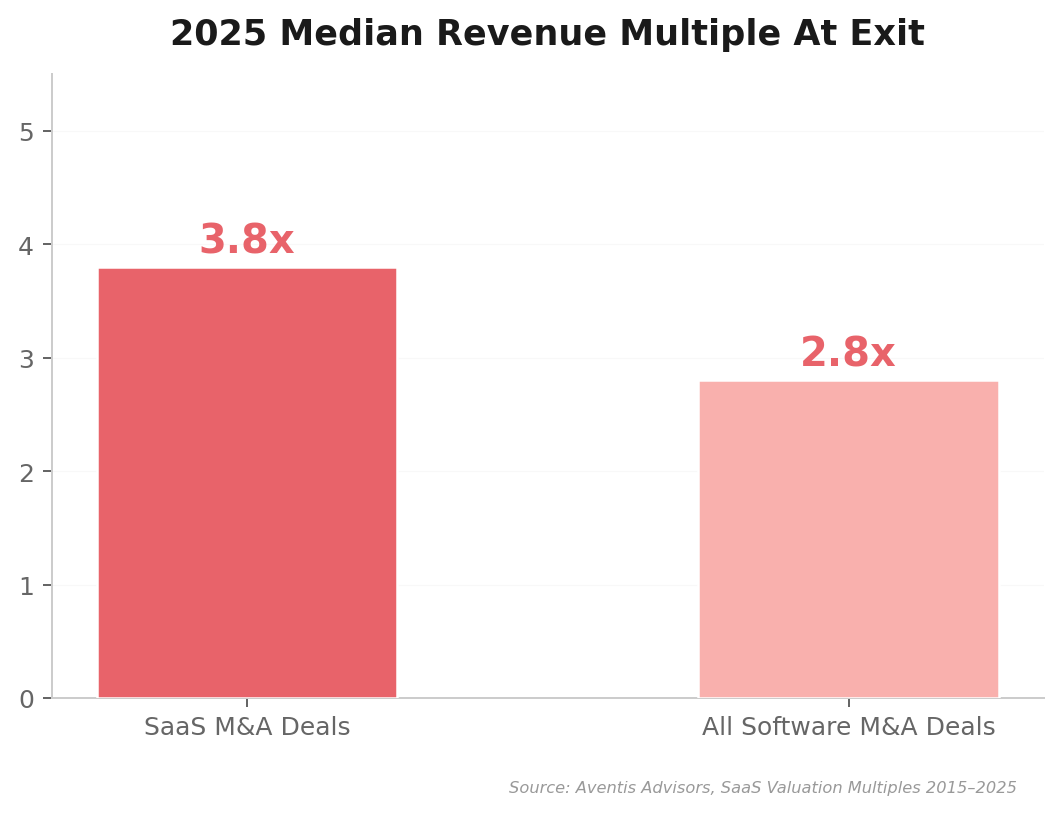

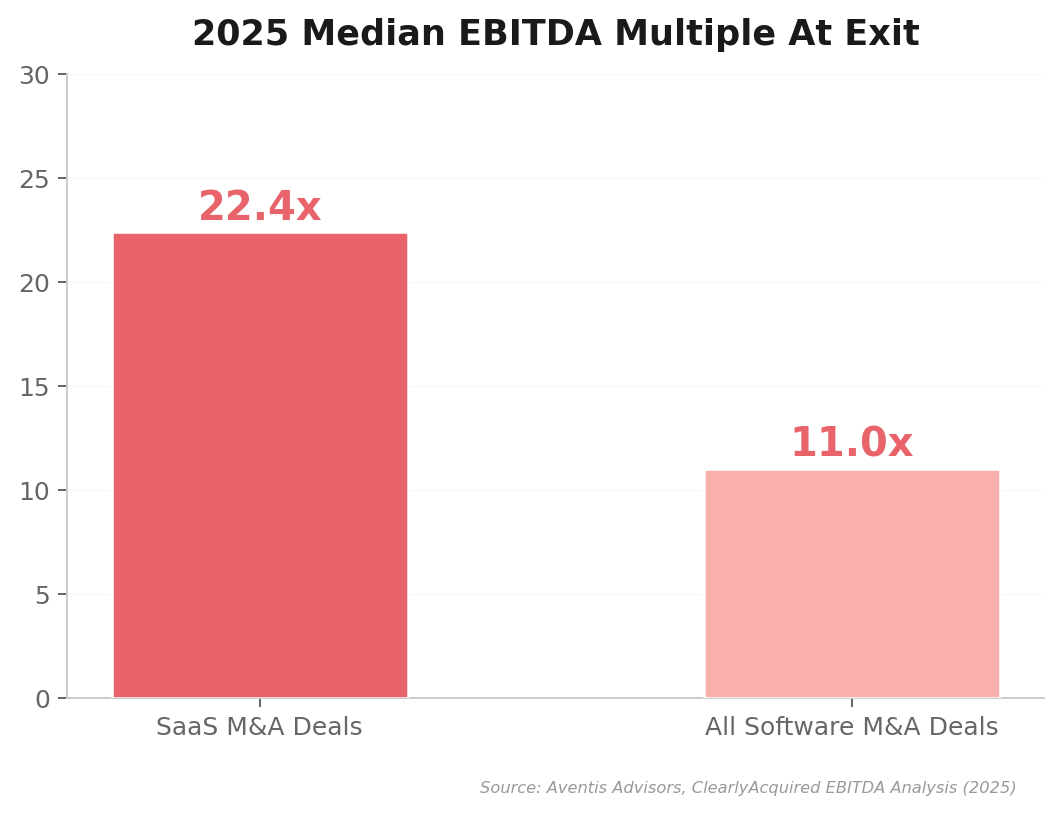

The report shows median private SaaS exit multiples around 3.8x, up from 2.9x in 2024, with bootstrapped SaaS around 4.8x, VC-backed SaaS around 5.3x, and AI-native or top-quartile vertical SaaS businesses reaching much higher ranges. In some premium cases, the best AI-native assets are still getting 9x to 12x median ranges, with elite names pushing further.

That does not mean the market is generous. It means the market is discriminating.

And that is a healthier way to think about 2026. This is not a market where “SaaS” is one bucket. It is a market where quality, category position, retention, and transferability are driving huge spread between winners and losers.

A founder with weak retention, slowing growth, no AI positioning, no category authority, and a company that still depends on personal heroics is going to get treated very differently from a founder who has built a repeatable, efficient, category-relevant machine.

That may sound obvious, but many founders still think about valuation too broadly. They ask what “the SaaS multiple” is, as if the answer will somehow apply evenly across the market. It won’t.

In 2026, valuation is increasingly a referendum on quality.

That is uncomfortable if you have built something fragile. It is encouraging if you have built something real.

The market did not collapse. It bifurcated.

I think the cleanest way to describe the moment is this: the market did not break, it split.

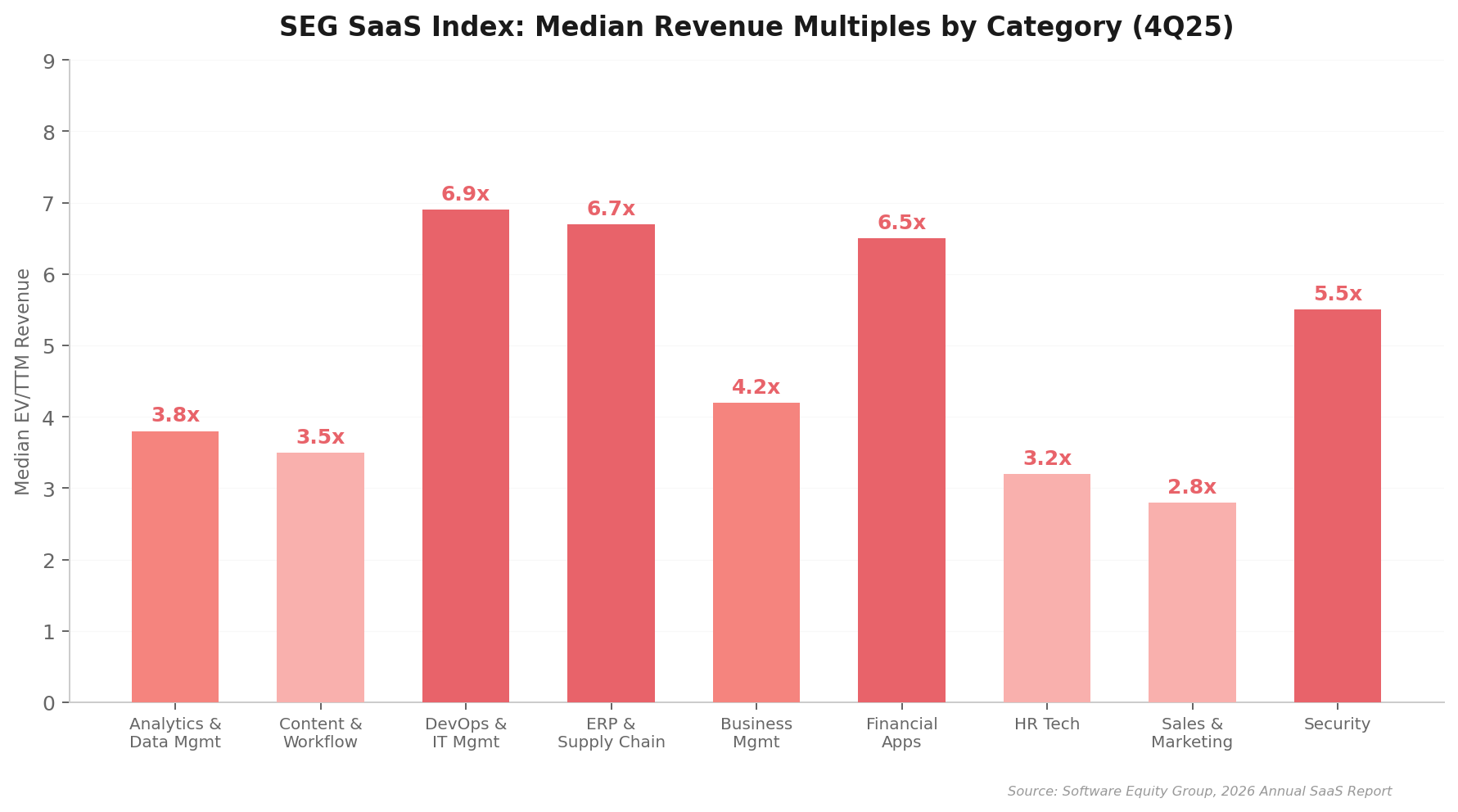

The report makes this point through its valuation framework. It distinguishes between commodity horizontal SaaS, healthy vertical SaaS, AI-enhanced incumbents, and AI-native firms. That framing is important because it explains why two software companies with similar revenue can now receive dramatically different reactions from buyers.

This is not just about AI hype. It is about perceived durability.

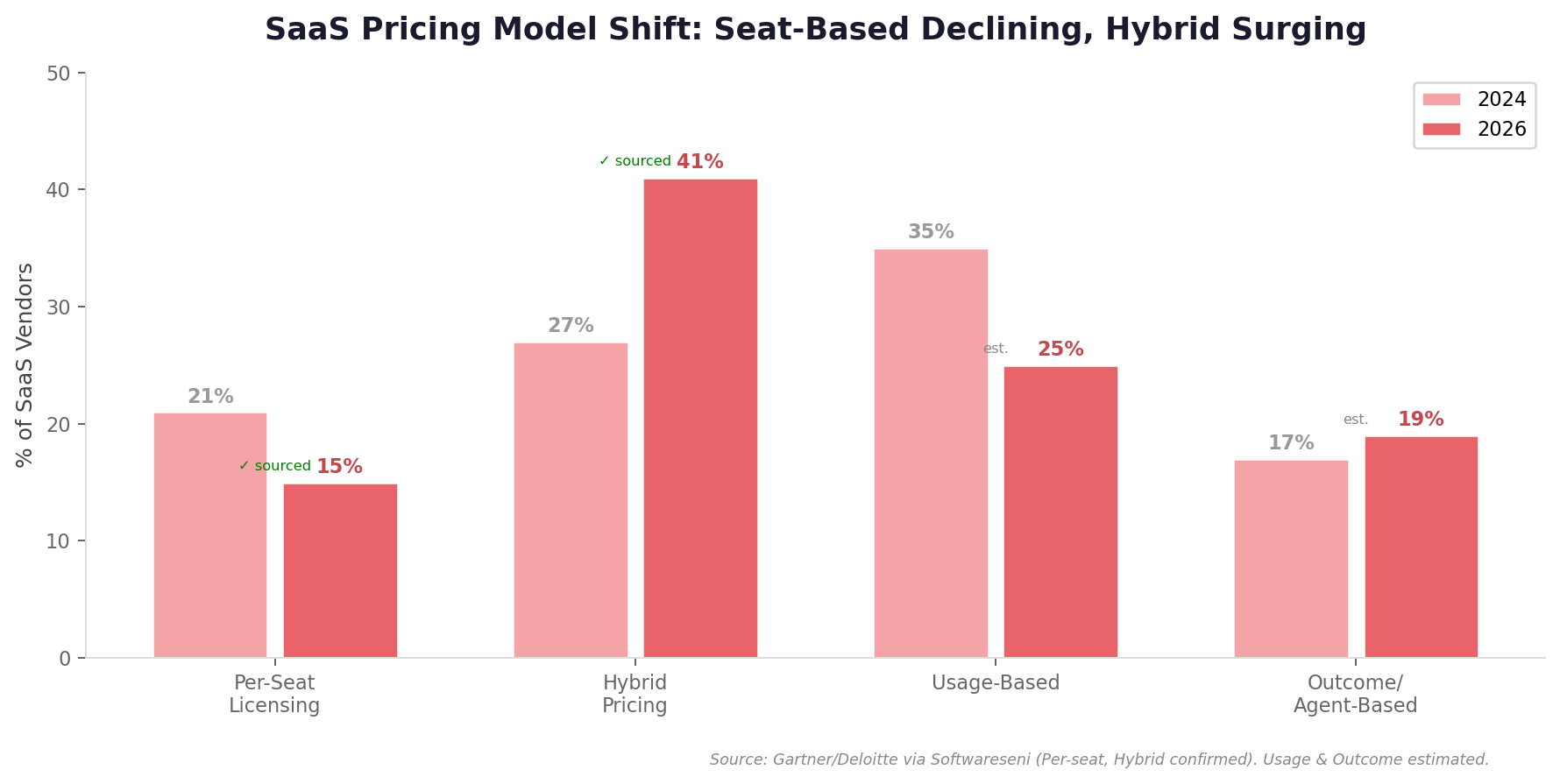

If your product can be flattened into a feature inside a larger workflow, you have a problem. If your software depends on a user behavior that generative AI can simplify or automate away, buyers are going to price that risk in. The report specifically calls out customer support software, simpler CRM layers, and content-production tooling as exposed categories.

At the same time, infrastructure, cybersecurity, compliance, workflow systems with deep switching costs, and strong vertical SaaS platforms still look attractive because they solve problems that are durable, embedded, and expensive to replace.

That leads to the bifurcation we are now seeing:

- The best firms are still being rewarded for quality, efficiency, and defensibility.

- The middle is being compressed.

- Weak firms are being discounted fast.

That is why broad panic narratives are often misleading. They blur together categories that buyers are actively separating.

If you are a founder, you do not need to predict the entire software market. You need to understand which side of the separation your company is currently on.

Rule of 40 is no longer a nice metric. It is a screening tool.

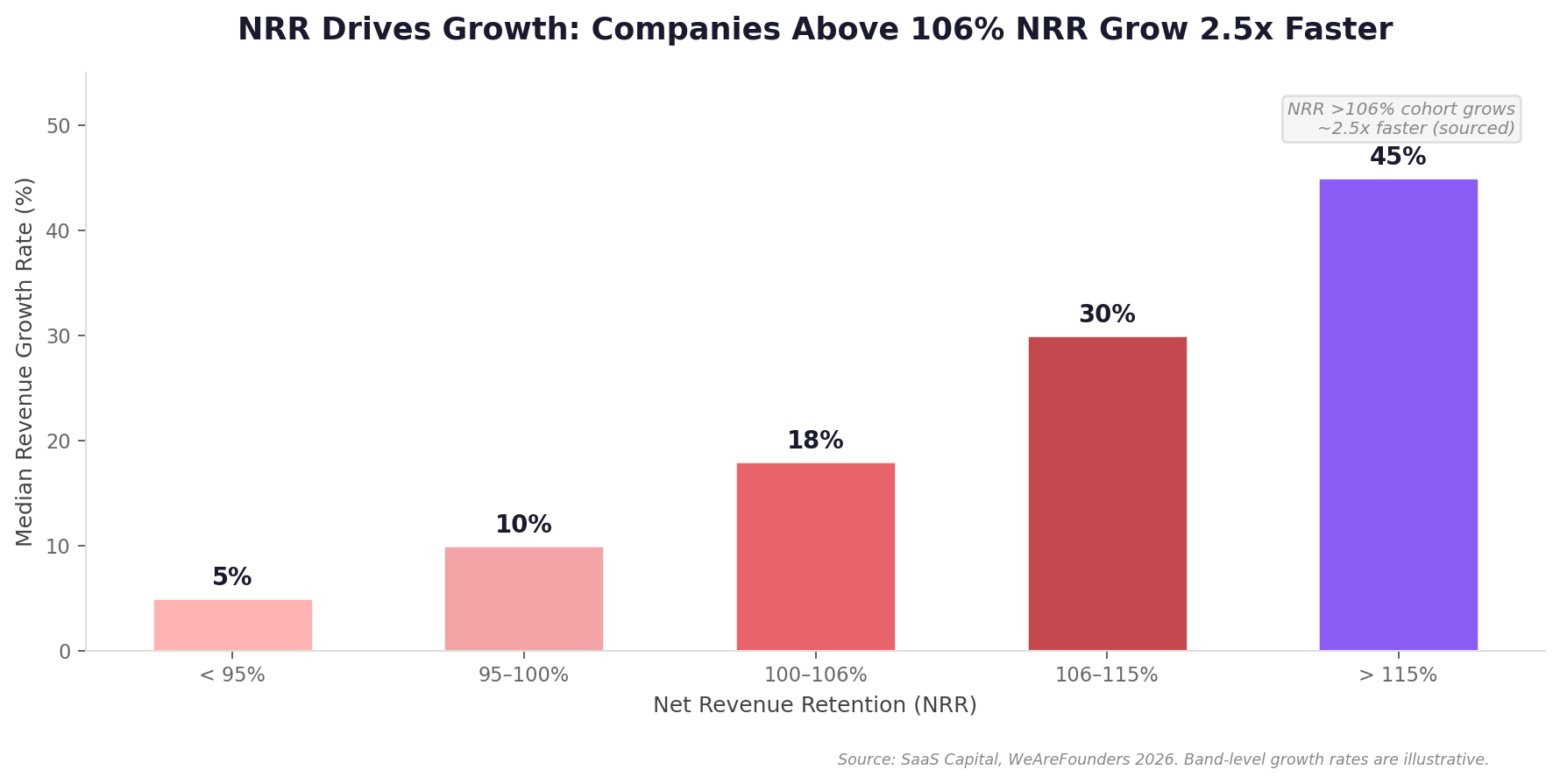

One reason the market is becoming stricter is that there is less tolerance now for “growth at any cost” stories without strong supporting economics. Your report is right to emphasize the Rule of 40 as one of the defining lenses of this period. It has become shorthand for something buyers care about deeply: can this company grow without looking operationally reckless?

The report also notes that every 10-point improvement in Rule of 40 can materially increase valuation, and that NRR above 106% is associated with meaningfully stronger company outcomes.

That matters because in noisy markets, buyers look for metrics that reduce ambiguity.

A clean Rule of 40 story tells them this is not smoke and mirrors. A healthy NRR profile tells them existing customers are validating the business every month. Strong payback periods and sensible CAC tell them growth is engineered, not subsidized accidentally.

This is where unit economics stop being something you review in a board deck and start becoming part of the acquisition narrative itself.

I’ve said before, “profitable paid customer acquisition where LTV:CAC is 6:1 or better is the holy grail of scaling.” That is still true, but in 2026 it matters for another reason too: it helps a buyer believe they can step into the company and keep the machine working.

That is the real question behind the number.

Does the business work because the founder is extraordinary, or does it work because the operating system is sound?

AI changed the conversation, but not the basic rules of company-building

A lot of founders are overcorrecting right now. They see what happened in public markets and assume they need to completely reinvent their identity around AI. That is often a mistake.

AI matters. It absolutely matters. The report is correct that firms with strong AI narratives or truly AI-native workflows are getting premium attention. Buyers want to know whether your company can benefit from AI, defend itself against AI substitution, or build leverage because of AI rather than in spite of it.

But there is a big difference between having an AI strategy and having an AI costume.

If your whole answer is “we added a copilot,” buyers will see through that quickly. If you can explain how AI improves your margins, increases switching costs, deepens your moat, accelerates onboarding, improves outcomes, or expands your product surface in a durable way, that is much more valuable.

The basic rules have not changed.

Buyers still care about:

- recurring revenue quality

- retention

- market position

- growth efficiency

- leadership depth

- transferability of operations

AI now sits on top of those fundamentals. It does not replace them.

The founders who will benefit most from the AI shift are not the ones who shout the loudest. They are the ones who can incorporate AI into an already well-run company.

M&A is still happening because good assets are still rare

One thing I liked about the report is that it does not treat M&A like an automatic consequence of hitting some revenue milestone. It presents the sale process as what it really is: an outcome you have to prepare for.

That is the right mindset.

There is a line in the other source material that I think fits well here: “buyers pay for things that are durable and transferable.” That is one of the simplest ways to think about exit prep.

The companies that get strong outcomes are usually not just the ones with decent ARR. They are the ones that feel ownable.

That means the buyer can imagine:

- the company continuing to hit numbers without the founder in every decision

- a sales and marketing engine that is measurable and repeatable

- reporting that does not feel improvised

- a management team that can run the business

- a customer base that is sticky enough to trust the forecast

Your report highlights that competitive processes with multiple interested buyers produce much better outcomes than passive or founder-led conversations. That is exactly right. A strong process changes not just valuation, but leverage.

Founders often underestimate how much the sale process itself matters. They focus on building the business, which is obviously the main thing, but then treat the actual transaction as if a great asset automatically sells itself.

It does not.

At scale, process is part of value creation.

The growth engine still matters more than the mood

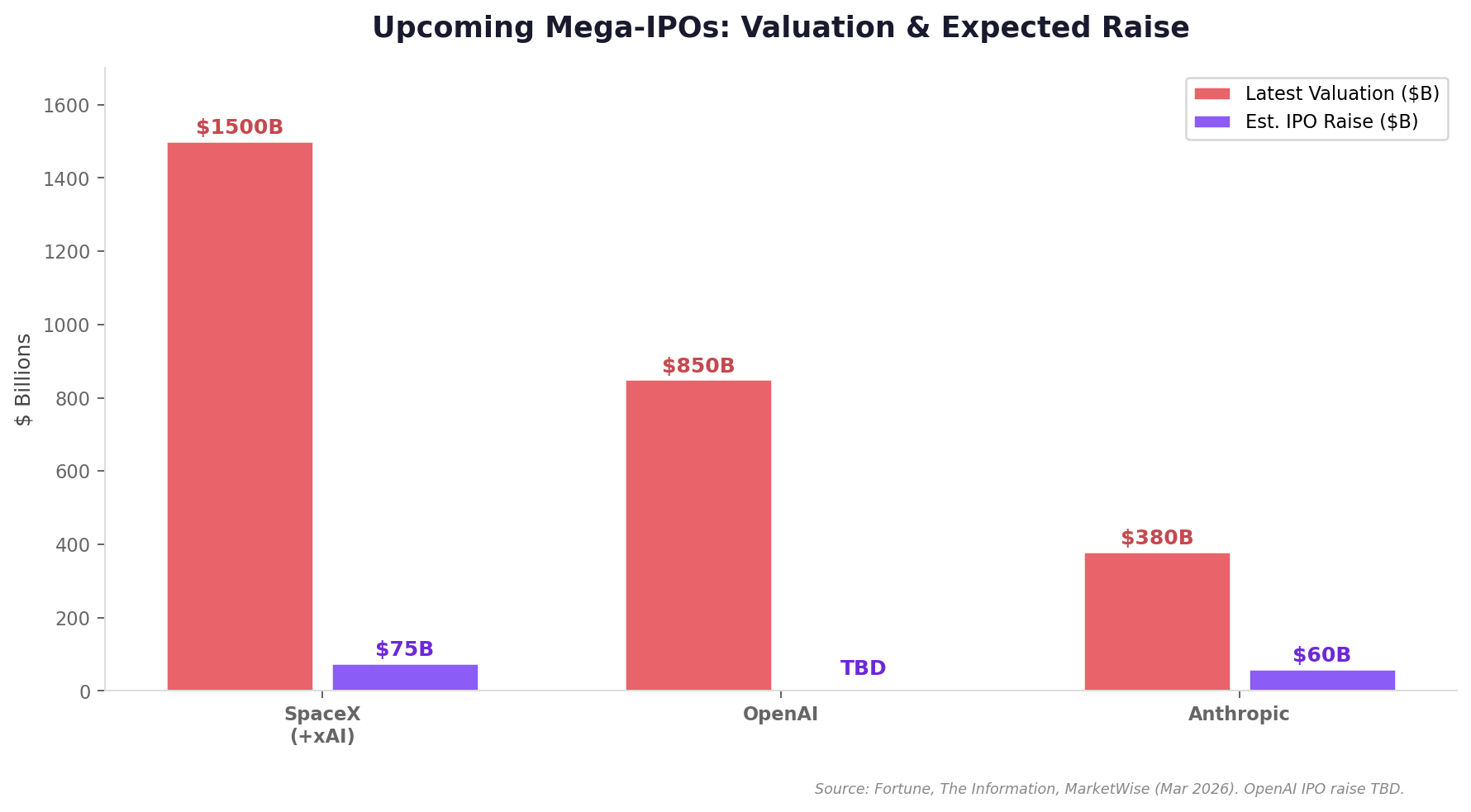

A lot of founders today are waiting for sentiment to improve. They want the IPO window to reopen, public multiples to bounce, AI enthusiasm to settle, and buyers to become more confident. Some of that may happen. Your report predicts a stabilizing public market, more AI and SaaS IPOs in the second half of 2026, and M&A volume passing $200 billion as take-privates and strategic transactions continue.

That may all be right directionally.

But founders should be careful not to outsource their strategy to market mood.

The more useful question is: if sentiment improved tomorrow, would your business actually be ready to benefit?

Because if the answer is no, then macro optimism is not your bottleneck.

This is where I come back to the growth system thinking from the other materials. The strongest SaaS firms are not relying on one channel, one heroic seller, or one lucky quarter. They are building coordinated revenue engines that can scale predictably through outbound, paid acquisition, content, ABM coverage, and disciplined economics.

Or put more simply, “the goal is ICP omnipresence.”

That kind of market presence does two things. It grows revenue now, and it makes the business look stronger later. A buyer is always more attracted to a company that clearly knows how demand is created, captured, and expanded.

In a difficult market, that confidence is worth even more.

What founders should actually do from here

If I were advising a SaaS founder based on this report, I would not tell them to obsess over the phrase “SaaSpocalypse.” I would tell them to use this market as a forcing function.

Ask hard questions.

Not performative ones. Real ones.

For example:

- If a buyer looked at my company today, would they see a defensible category position or a replaceable tool?

- Is our retention good enough to survive serious diligence?

- Do our economics tell a scaling story, or a cautionary one?

- Can I explain our AI strategy in terms of business value, not just product features?

- If I disappeared for 30 days, would the company still run?

That last question is one of the most revealing. Buyers discount founder dependence aggressively. They want the founder to matter, of course. They do not want the founder to be the operating system.

That is why one of my favorite lines in the exit material remains so useful: “Your job becomes ‘build a machine,’ not ‘be the machine.’”

That is not abstract advice. It is operational valuation advice.

The founders who win this market will be the disciplined ones

There is always a temptation in chaotic markets to search for a new trick. A new tactic. A new story that lets you escape the hard work of fundamentals.

I do not think 2026 is going to reward that approach.

This is a market that is rewarding discipline. Not perfection, but discipline.

Discipline in company design.

Discipline in economics.

Discipline in positioning.

Discipline in growth.

Discipline in how you prepare for an eventual exit.

The report’s final takeaway is that the roadmap is not actually complicated. It is disciplined. I agree with that. Bootstrap or preserve leverage early when you can. Learn your unit economics cold. Build outbound and paid acquisition into a repeatable machine. Educate the market consistently. Hire leaders. Build systems. Raise only when it accelerates what already works. Then run a real exit process when the time is right.

That is still the game.

And in some ways, a market like this makes that easier to see. When loose capital fades and hype becomes unstable, the underlying shape of the business becomes much more visible.

That is good news for serious builders.

My bottom line

I do not think founders should read this report and panic.

I think they should read it and sharpen up.

Yes, public SaaS got hit hard. Yes, AI is changing category boundaries. Yes, buyers are asking harder questions. But the private market is still buying. Quality still matters. Efficient growth still matters. Transferability still matters. Good businesses still get rewarded.

At iContact, “our method of math-based scaling worked.” In our final year before the exit, we added 216,000 new trial users, 36,000 new customers, spent $20 million on sales and marketing, generated $50 million in revenue, and sold the business for $169 million.

That exact path will not be every founder’s path now. The market is different. The tools are different. The AI layer changes a lot.

But the principle underneath it is not different.

Know your numbers.

Build a real machine.

Invest in growth when the payback is there.

Make the company transferable.

Prepare early for the exit you say you want.

And remember this line, because it is even more relevant in a selective market: “raise to scale what works, not to discover what works.”

That is how you avoid becoming one of the companies the market discounts.

And that is how you build one of the companies buyers still want badly.