The Vertical SaaS M&A & VC Report 2026

If you’re a vertical SaaS CEO, your company is worth more than you think — and the gap is widening.

In 2025, vertical SaaS companies sold for a 41% premium over horizontal SaaS — the largest gap ever recorded. Healthcare IT platforms changed hands at 8.5x revenue. Construction tech hit 7.5x. Legal tech reached 7.0x. Meanwhile, generic horizontal SaaS languished at 4.1x, increasingly commoditized by AI.

The message from the market is unmistakable: depth beats breadth. Buyers and investors are paying record premiums for software that owns the workflow, the compliance layer, the data, and the payment rails of a specific industry. If your SaaS product is the operating system for your customers’ businesses — the thing they literally cannot turn off — you are sitting on a highly valuable asset.

This report breaks down exactly what that asset is worth. We analyzed 1,275+ M&A transactions and 2,300+ VC rounds in vertical SaaS from January 2025 through May 2026, profiling 24 major M&A deals and 17 notable VC rounds where valuations are known. Inside you’ll find median revenue multiples by vertical, the formula for premium valuations, how M&A and VC pricing differs (and why), and the eight trends every vertical SaaS founder needs to understand heading into the second half of 2026.

Whether you’re considering a raise, exploring M&A, or simply want to benchmark where your company stands — this is the data you need.

This report is published by SaasRise, the #1 mastermind community for B2B SaaS CEOs with $1M–$100M+ in ARR. Our members have collectively raised over $1B and represent $3B+ in combined ARR. We publish original research like this report regularly, and our CEO masterminds bring together the founders behind the fastest-growing vertical SaaS companies in the world.

Vertical SaaS M&A Revenue Multiples (Buyout Transactions)

Vertical SaaS VC Deal Multiples (Minority Investment Rounds)

Vertical vs. Horizontal SaaS Premium

Why does vertical SaaS command higher multiples than horizontal SaaS? Vertical software is purpose-built for a single industry with specialized workflows, regulatory compliance, and embedded fintech capabilities that create exceptionally high switching costs. Windsor Drake’s Q4 2025 Vertical SaaS Valuation Report found that premium vertical SaaS companies trade at a median of 7.8x EV/Revenue — a 46% premium over public horizontal SaaS at 5.3x. Gross revenue retention above 90%, embedded payment processing, and deep workflow integration make vertical SaaS businesses significantly more defensible than generic horizontal tools.

📋 Table of Contents

- Vertical SaaS Market Overview (Jan 2025 — May 2026)

- The Biggest Vertical SaaS M&A Deals

- M&A Revenue Multiples by Vertical Sub-Segment

- Vertical SaaS Venture Capital & Funding Rounds

- M&A vs. VC Multiples: Why the Gap Exists

- Vertical vs. Horizontal Multiples Over Time (2020–2026)

- Deal Volume & Market Activity

- Notable Deal Case Studies

- Top Vertical SaaS Trends Shaping 2026 & Beyond

- 2026 Outlook & Predictions

- Sources & Methodology

Key Report Findings

- Vertical SaaS M&A multiples hit 5.8x — a 41% premium over horizontal SaaS (4.1x), the widest gap ever recorded

- Healthcare IT leads all verticals at 8.5x, followed by construction tech (7.5x), legal tech (7.0x), and field services (7.0x)

- $10.55B Boeing Digital Aviation deal led 24 profiled M&A transactions — five exceeded $2B

- Clio’s $850M Series G at $5.0B valuation topped 17 profiled VC rounds worth a combined $4.5B+

- VC multiples exceed M&A multiples by 35–50% — we explain the four structural reasons why

- Vertical SaaS captured 54% of all SaaS M&A volume and 53% of all VC deal volume in 2025

- Embedded fintech adds 33–60% to valuations — it’s now the single most important value driver

- 8 major trends reshaping vertical SaaS in 2026, from AI-powered execution to pricing model revolution

1. Vertical SaaS Market Overview

The vertical SaaS market experienced record-setting consolidation and investment activity between January 2025 and May 2026. According to Software Equity Group’s 2026 Annual SaaS Report, overall SaaS M&A reached an all-time high of 2,698 transactions in 2025 — a 28% increase over 2024. Vertical SaaS companies represented an estimated 46–54% of those deals depending on the quarter, making it the dominant category in SaaS M&A for the first time.

Several macro forces shaped the vertical SaaS deal environment:

- Embedded fintech as a value driver: BCG research found that 59% of U.S. SMEs adopted vertical software in 2024, and SaaS providers with embedded payments captured 36% of SME acquiring revenues. Vertical SaaS companies with embedded fintech commanded 33–60% valuation premiums over pure software-only peers.

- AI integration across verticals: Every major vertical — healthcare, construction, legal, restaurant — saw AI become a deal catalyst. Procore acquired Datagrid for construction AI, Veeva acquired Ostro for AI-powered brand engagement, and OfferFit’s AI marketing optimization attracted a 10.8x premium from Braze.

- Private equity dominance: PE buyers were involved in nearly 57–58% of all SaaS transactions in 2025, with firms like Thoma Bravo, Clearlake Capital, TPG, and Francisco Partners actively building vertical platforms through acquisitions and take-privates.

- Regulatory moats driving premium valuations: Healthcare IT (HIPAA), financial services (SOC 2, PCI), and legal tech (bar compliance) verticals commanded the highest multiples because regulatory requirements create natural barriers to entry and switching.

💡 Key Finding: Vertical SaaS companies traded at a 41% premium to horizontal SaaS in M&A transactions in 2025 (5.8x vs. 4.1x median EV/Revenue). Premium verticals — healthcare IT, construction tech, and legal tech — commanded 7.0x–8.5x revenue, nearly double the horizontal SaaS median. The gap widened from 2024, when vertical SaaS traded at only a ~10% premium (3.3x vs. 3.0x per The Growth Elements), reflecting accelerating buyer preference for niche, defensible software businesses.

2. The Biggest Vertical SaaS M&A Deals

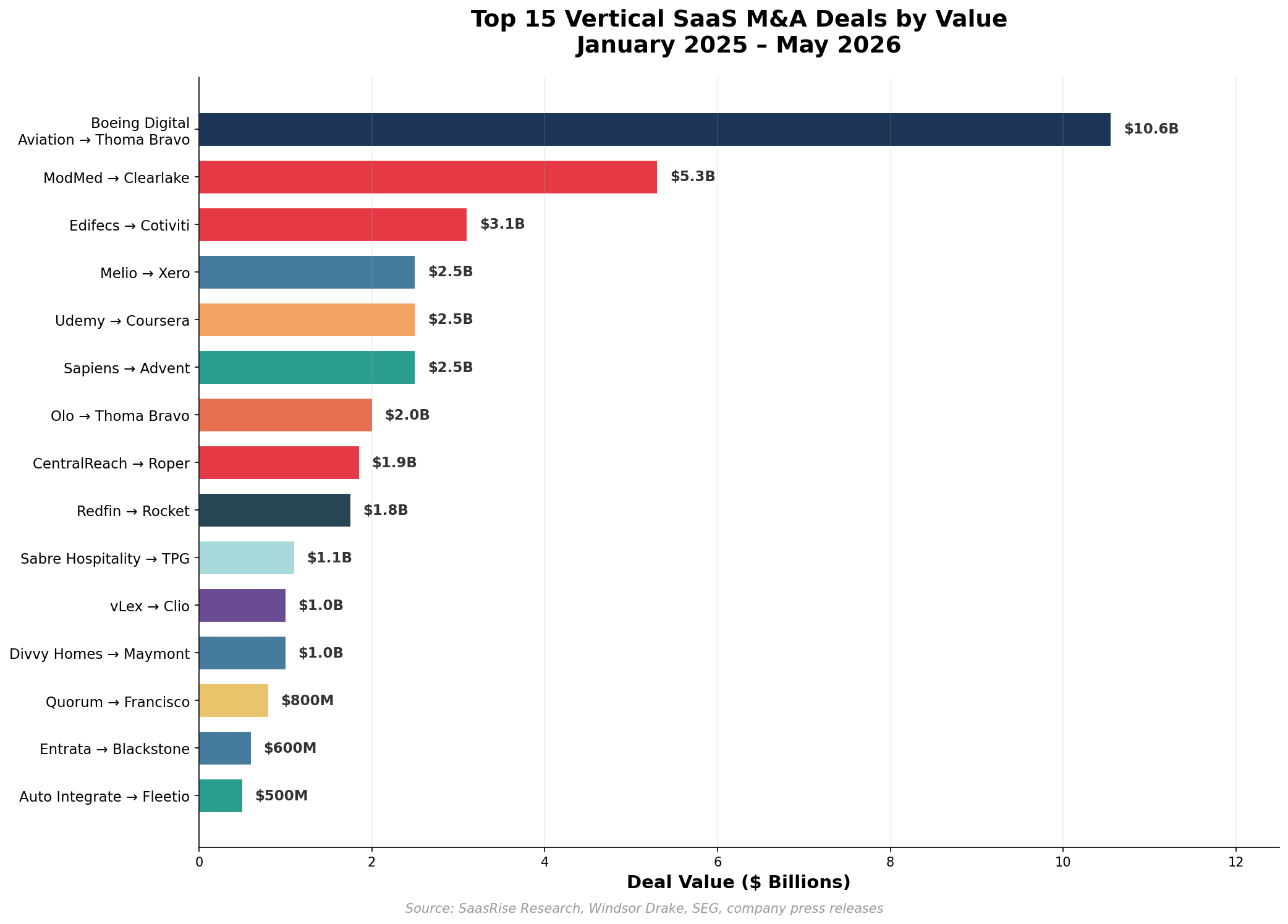

Despite macro uncertainty and public SaaS multiple compression, the vertical SaaS M&A market produced several landmark transactions. Healthcare SaaS led with two mega-deals exceeding $3 billion, while restaurant tech, PropTech, and legal tech each generated billion-dollar transactions. Below are the 24 notable vertical SaaS M&A deals from January 2025 through May 2026 where the deal value or valuation is known, ranked by transaction size.

Figure 1: The largest Vertical SaaS M&A transactions from January 2025 — May 2026 with disclosed deal values

| Date | Target | Acquirer | Deal Value | Vertical | Est. Multiple |

|---|---|---|---|---|---|

| Apr 2025 | Boeing Digital Aviation | Thoma Bravo | $10.55B | Aviation Software | ~8.0x |

| Mar 3, 2025 | ModMed | Clearlake Capital | $5.3B | Healthcare IT | ~10.6x |

| Feb 10, 2025 | Edifecs | Cotiviti (KKR) | $3.1B | Healthcare Data | ~8.0x |

| Jun 24, 2025 | Melio | Xero | $2.5B | SMB Payments | ~16.3x |

| Dec 17, 2025 | Udemy | Coursera | $2.5B | EdTech | ~1.7x |

| Aug 2025 | Sapiens | Advent International | $2.5B | Insurance SaaS | ~5.5x |

| Sep 12, 2025 | Olo | Thoma Bravo | $2.0B | Restaurant SaaS | ~6.2x |

| Mar 2025 | CentralReach | Roper Technologies | $1.85B | Autism / IDD Care | ~9.0x |

| Mar 10, 2025 | Redfin | Rocket Companies | $1.75B | Real Estate Tech | ~3.5x |

| Apr 2025 | Sabre Hospitality | TPG | $1.1B | Hospitality Tech | ~5.5x |

| Nov 10, 2025 | vLex | Clio | $1.0B | Legal Tech | ~8.0x |

| Jan 22, 2025 | Divvy Homes | Maymont Homes | $1.0B | PropTech / Fintech | ~6.0x |

| Mar 4, 2025 | Quorum Software | Francisco Partners | ~$800M* | Energy SaaS | ~5.0x |

| May 15, 2025 | Entrata (minority) | Blackstone | $4.3B val. | PropTech | N/A |

| Mar 25, 2025 | Auto Integrate | Fleetio | ~$500M | Fleet Management | ~8.0x |

| Nov 13, 2024 | JobNimbus | Sumeru Equity | $330M | Construction SaaS | ~8.0x |

| Oct/Nov 2025 | Sojern | RateGain | $250M | Travel / Hospitality SaaS | ~5.0x |

| Jan 20, 2026 | Datagrid | Procore | ~$250M* | Construction AI | ~10.0x |

| Aug 2025 | intelliflo | Carlyle Group | ~$200M | Wealth Management | ~6.0x |

| Jul 2025 | SuranceBay | Verisk | $163M | Insurance Software | ~7.0x |

| Mar 10, 2026 | Ostro | Veeva Systems | $100M | Life Sciences | ~10.0x |

| Jan 2026 | Insurance Verif. Co. | i3 Verticals | ~$80M | Insurance Software | ~6.0x |

| Sep 2025 | Quorum Info Tech | Valsoft | ~$60M | Automotive SaaS | ~4.0x |

| May 2026 | Scala | Vertiseit | ~$27M | Retail SaaS | ~3.5x |

* Estimated value; financial terms not officially disclosed.

Deal Highlights

Clearlake → ModMed ($5.3B) — The largest vertical SaaS deal of the period. Clearlake Capital acquired a majority stake in ModMed, a healthcare SaaS platform specializing in specialty-specific electronic health records, practice management, and revenue cycle management. With revenue north of $500 million and 40,000+ providers, the deal valued ModMed at roughly 10.6x revenue — reflecting the premium the market places on healthcare vertical SaaS with deep regulatory moats, high switching costs, and embedded payment capabilities.

Cotiviti/KKR → Edifecs ($3.1B) — Cotiviti, backed by Veritas Capital and KKR, acquired Edifecs, a healthcare data interoperability pioneer serving nearly 300 million people in the U.S. healthcare market. The deal creates a comprehensive healthcare SaaS platform spanning claims processing, data management, and value-based care solutions — underscoring PE’s appetite for mission-critical healthcare infrastructure.

Thoma Bravo → Olo ($2.0B at ~6.2x Revenue) — Thoma Bravo’s take-private of restaurant technology platform Olo at a 65% premium signals continued PE confidence in vertical SaaS. Olo’s 750+ restaurant brand customers, 88,000 active locations, and 111% net revenue retention demonstrate the stickiness that makes vertical SaaS attractive to financial sponsors.

Clio → vLex ($1.0B) — Legal tech leader Clio used its $850 million Series G (at a $5 billion valuation) to fund the simultaneous acquisition of vLex, a legal research platform. The deal creates an end-to-end legal technology platform spanning practice management, client intake, and AI-powered legal research — the most comprehensive legal workflow suite in the market.

3. M&A Revenue Multiples by Vertical Sub-Segment

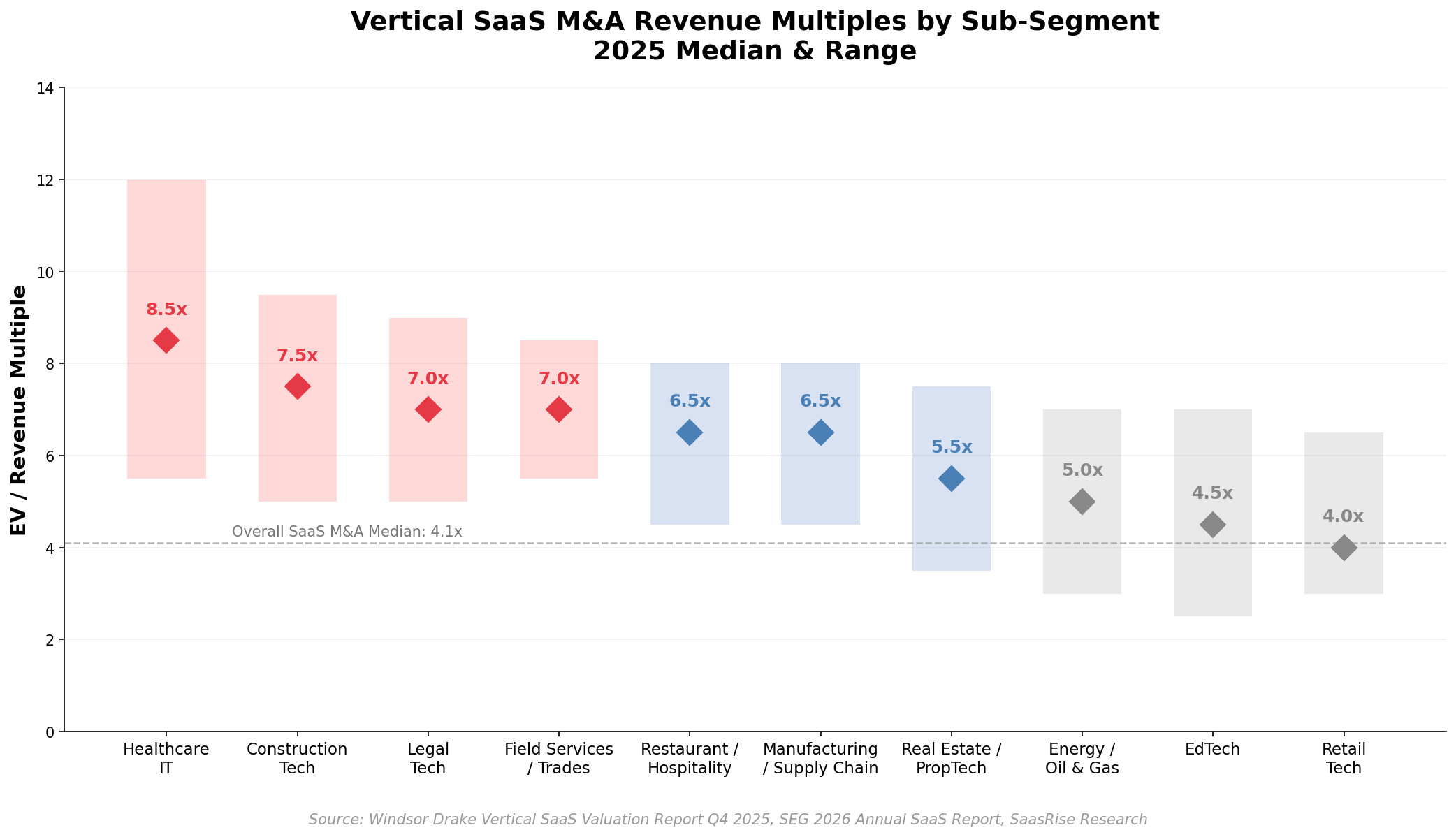

Not all vertical SaaS is valued equally. Revenue multiples vary dramatically by industry vertical, with healthcare IT commanding nearly 2x the multiple of education technology. The chart below shows the median M&A revenue multiple for each vertical SaaS sub-segment in 2025, along with the range of observed deal multiples.

Figure 2: Vertical SaaS M&A revenue multiples by sub-segment, 2025. Diamond = median; shaded range = observed deal spread.

📊 Vertical SaaS M&A Median Revenue Multiples

- Overall Vertical SaaS M&A Median (2025): 5.8x EV/Revenue

- Overall Vertical SaaS M&A Median (2026 YTD): 5.5x EV/Revenue

- Premium Vertical SaaS M&A Median (2025): 7.8x EV/Revenue

- Overall Horizontal SaaS M&A Median (2025): 4.1x EV/Revenue

- Vertical SaaS Premium over Horizontal (2025): +41%

The data reveals a clear hierarchy within vertical SaaS M&A valuations:

- Healthcare IT (8.5x median): The highest-valued vertical, driven by HIPAA compliance moats, mission-critical workflows, and embedded revenue cycle management. Clearlake’s $5.3B ModMed acquisition (~10.6x) and Cotiviti/Edifecs ($3.1B, ~8.0x) anchor this segment. Companies with embedded fintech (payment processing, claims management) command an additional 33–45% premium.

- Construction Tech (7.5x median): The second-highest vertical, benefiting from massive underdigitization in the $1.5 trillion North American construction industry. Procore ($9.2B market cap, $1.32B FY2025 revenue) sets the valuation benchmark. Sumeru’s $330M JobNimbus deal (~8.0x) and Procore’s acquisitions of Datagrid and FlyPaper demonstrate continued demand.

- Legal Tech (7.0x median): Strong recurring revenue, workflow integration depth, and growing AI adoption drive premium valuations. Clio’s $5B valuation at ~10.0x revenue and its $1B vLex acquisition showcase the category’s momentum.

- Field Services / Trades (7.0x median): ServiceTitan’s successful December 2024 IPO at ~$9B+ validated the vertical. Deep workflow integration across scheduling, dispatch, invoicing, and embedded payments creates high switching costs. The segment includes HVAC, plumbing, roofing, and landscaping software.

- Restaurant / Hospitality (6.5x median): Thoma Bravo’s $2B Olo take-private (~6.2x) and TPG’s $1.1B Sabre Hospitality buyout (~5.5x) reflect robust deal activity. Toast ($17B+ market cap, $5.5B+ revenue) remains the dominant public benchmark with its all-in-one restaurant operating system.

- Manufacturing / Supply Chain (6.5x median): TA Associates’ growth investment in iBase-t (aerospace/defense manufacturing MES) and continued demand for ERP-adjacent vertical platforms support solid multiples. AI-powered quality management and MRO automation are emerging deal catalysts.

- Real Estate / PropTech (5.5x median): Rocket Companies’ $1.75B Redfin acquisition and Blackstone’s $200M minority investment in Entrata ($4.3B valuation) anchor this segment. Transaction-dependent revenue models create multiple compression versus pure subscription verticals.

- Energy / Oil & Gas (5.0x median): Francisco Partners’ acquisition of Quorum Software from Thoma Bravo represents the primary data point. Energy vertical SaaS benefits from specialized regulatory requirements but faces cyclical end-market risk.

- EdTech (4.5x median): The Coursera-Udemy merger ($2.5B combined at ~1.7x revenue) compressed the segment median. Budget constraints in education, commoditization risk from free alternatives, and AI disruption fears weigh on EdTech multiples. Workday’s $1.1B acquisition of Sana AI (~9.0x) was a premium outlier driven by AI learning capabilities.

💡 Key Insight — The Vertical Premium is Real: According to Windsor Drake’s Q4 2025 Vertical SaaS Valuation Report, premium vertical SaaS companies trade at a 46% premium over horizontal SaaS peers (7.8x vs. 5.3x EV/Revenue). The premium is driven by three factors: gross revenue retention above 90% (vs. 80–85% for horizontal), embedded fintech generating 30–50% of revenue, and regulatory moats that limit competitive entry. Vertical SaaS platforms also achieve 25–30% better unit economics than horizontal SaaS, which translates directly into 15–20% higher valuations.

📈 Want to benchmark your company against these multiples?

SaasRise members get access to exclusive valuation benchmarks, M&A advisory introductions, and peer masterminds with other vertical SaaS CEOs navigating fundraising and exit decisions right now.

Explore SaasRise Membership →4. Vertical SaaS Venture Capital & Funding Rounds

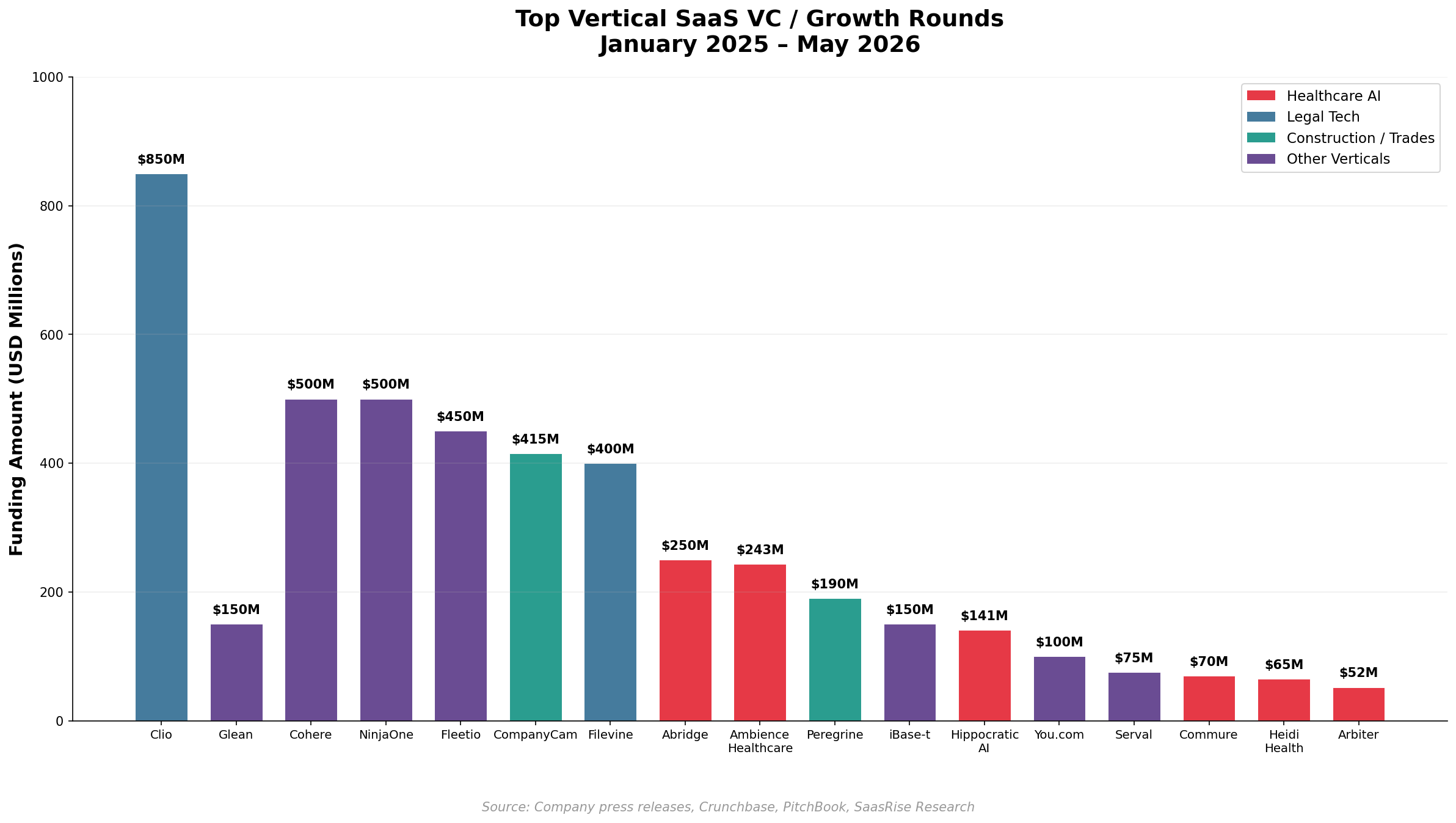

Venture capital activity in vertical SaaS surged in 2025. According to Euclid Ventures’ Vertical Report 2026, vertical startups captured 53% of all VC deal volume across 4,395 software and AI financing deals totaling $186 billion in the U.S. and Canada. Healthcare and financial services remained the twin pillars of vertical investing, combining for nearly 1,100 deals, while manufacturing & industrials, legal, and construction emerged as the fastest-growing categories.

Figure 3: Selected notable Vertical SaaS VC funding rounds, January 2025 — April 2026

Key Vertical SaaS VC Deals & Valuations

| Date | Company | Round | Amount | Valuation | Vertical | Est. Multiple |

|---|---|---|---|---|---|---|

| Nov 10, 2025 | Clio | Series G | $850M | $5.0B | Legal Tech | ~10.0x |

| 2025 | Glean | Funding Round | Undisclosed | ~$7.2B | Enterprise Productivity | N/A |

| 2025 | Cohere | Funding Round | $500M | $6.8B | Enterprise AI | N/A |

| May 6, 2025 | NinjaOne | Series C Ext. | $500M | $5.0B | IT/MSP Mgmt | ~12.0x |

| Mar 25, 2025 | Fleetio | Series D | $450M | $1.5B | Fleet Management | ~10.0x |

| Aug 2025 | CompanyCam | Series C | $415M | $2.0B | Construction / Trades | ~12.0x |

| Sep 23, 2025 | Filevine | All-Equity | $400M | Undisclosed | Legal Tech | ~10.0x |

| Jan 9, 2025 | Hippocratic AI | Series B | $141M | $1.64B | Healthcare AI | ~15.0x |

| Feb 2025 | Abridge | Funding Round | $250M | ~$850M | Healthcare AI | ~12.0x |

| Jul 29, 2025 | Ambience Healthcare | Series C | $243M | Undisclosed | Healthcare AI | ~12.0x |

| Mar 6, 2025 | Peregrine | Series C | $190M | $2.5B | Construction AI | ~10.0x |

| Mar 31, 2026 | iBase-t | Growth (TA) | $150M | Undisclosed | Manufacturing | ~8.0x |

| Sep 2025 | You.com | Series C | $100M | $1.5B | Enterprise AI | N/A |

| Dec 2025 | Serval | Series B | $75M | $1.0B | IT / Enterprise Ops | ~13.0x |

| May 2026 | Commure | Financing | $70M | $7.0B | Healthcare | ~25.0x |

| Oct 2025 | Heidi Health | Series B | $65M | ~$465M | Healthcare AI | ~15.0x |

| Nov 2025 | Arbiter | Seed | $52M | $400M | Healthcare | N/A |

Vertical SaaS VC Deal Multiples

Clio ($5.0B valuation, $850M Series G) stands as the period’s marquee vertical SaaS VC event. The legal technology platform raised $500 million in equity plus $350 million in debt, using the capital to simultaneously acquire vLex for $1 billion. At roughly 10.0x revenue, Clio’s valuation reflects its dominant position in legal practice management, 150,000+ legal professionals on its platform, and the massive opportunity to digitize the traditionally underserved legal industry.

Fleetio ($1.5B valuation, $450M Series D) demonstrates the growing interest in logistics and fleet management vertical SaaS. Fleetio used the round to acquire Auto Integrate, creating a one-stop platform for fleet maintenance, inspections, and fuel management. The combined entity’s ~10.0x valuation reflects embedded fintech opportunities in fleet payments and financing.

CompanyCam ($415M Series C at $2.0B valuation) and Filevine ($400M all-equity financing) highlight the scale of late-stage vertical SaaS rounds in 2025. CompanyCam became Nebraska’s first unicorn by dominating construction site documentation for trades businesses, while Filevine is building the legal operating intelligence system. Both attracted nine-figure capital at premium multiples. In healthcare AI, Ambience Healthcare ($243M Series C) and Hippocratic AI ($141M Series B at $1.64B) represent the convergence of vertical SaaS and AI — Ambience automates clinical documentation at scale while Hippocratic builds AI agents for healthcare staffing. All four attracted venture capital at estimated 10–15x revenue multiples, consistent with the premium placed on AI-native vertical SaaS platforms that solve regulated, mission-critical workflows.

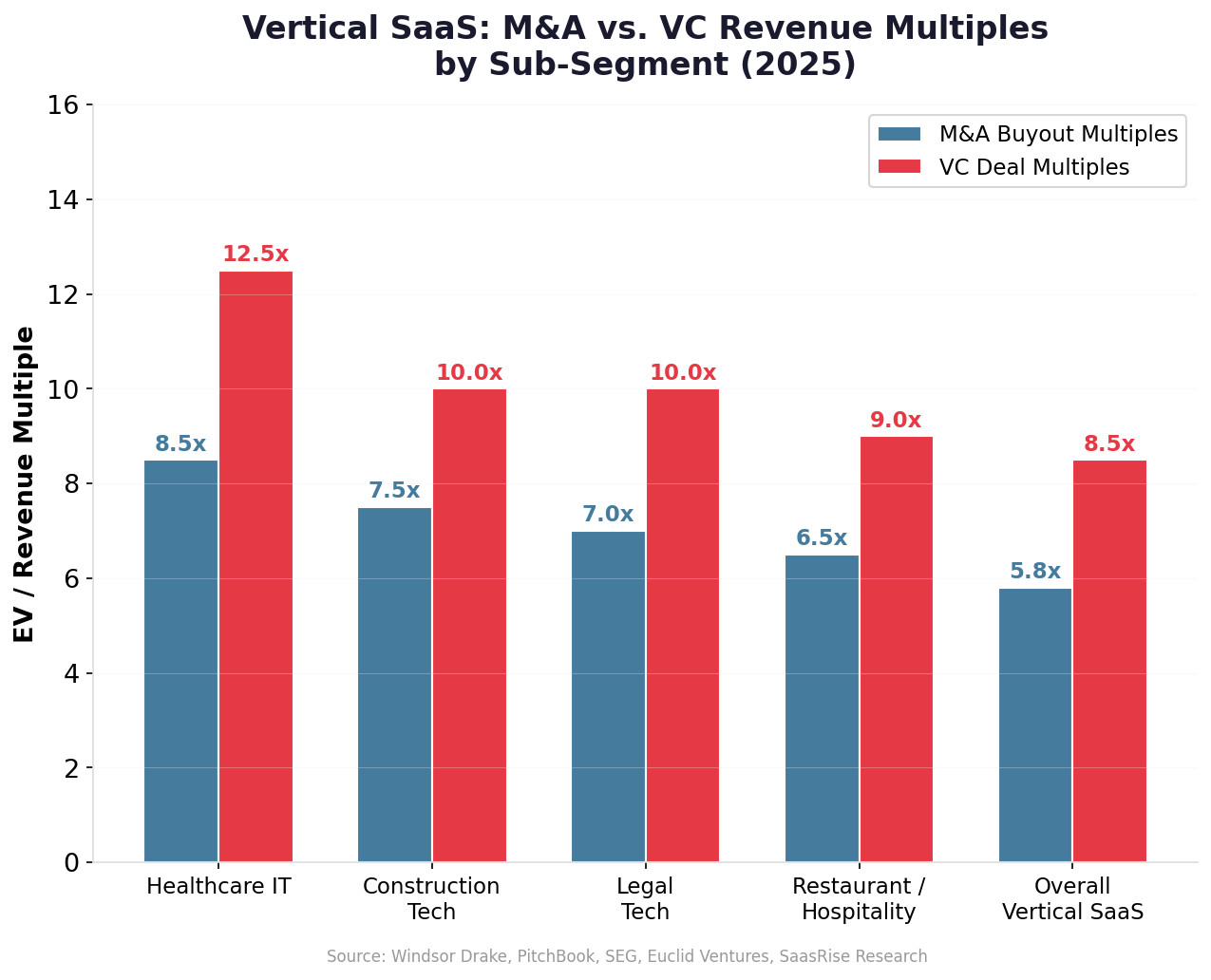

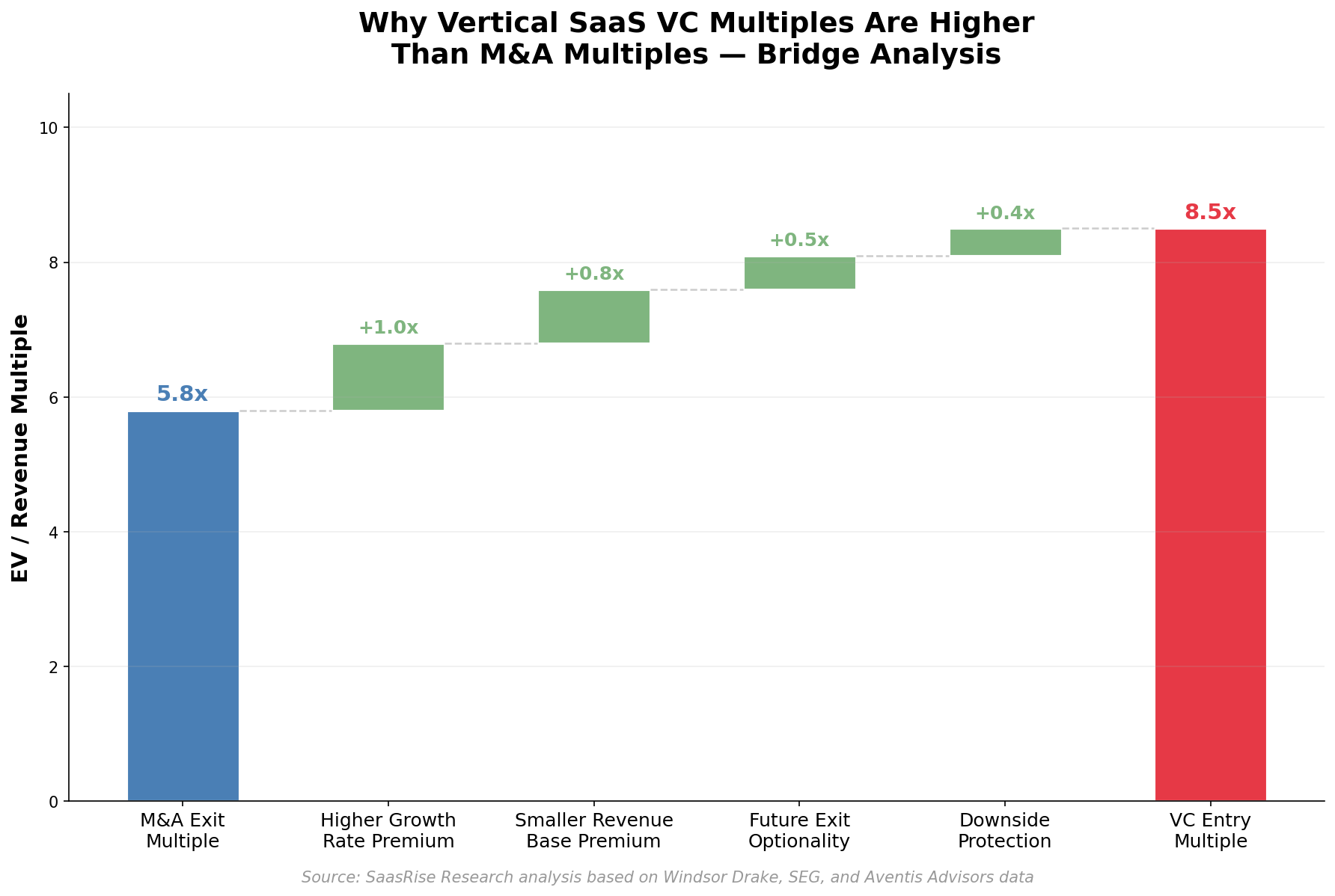

5. M&A vs. VC Multiples: Why the Gap Exists

One of the most important concepts for vertical SaaS founders to understand is the structural gap between M&A and VC revenue multiples. Across all vertical SaaS sub-segments, VC deal multiples consistently exceed M&A multiples by 35–50%, depending on the vertical.

Figure 4: M&A buyout multiples vs. VC minority investment multiples across five vertical SaaS categories

Why Are VC Multiples Higher Than M&A Multiples?

This is a question we receive frequently from SaaS founders, and the answer is rooted in four key factors that structurally inflate VC entry multiples relative to M&A exit multiples:

1. Higher Growth Rate Premium (+1.0x)

VC investments typically occur when a vertical SaaS company is growing 50–150%+ annually. Investors are paying for future revenue that doesn’t yet exist. M&A buyouts typically occur when growth has moderated to 15–40%, and acquirers are pricing current performance rather than speculative upside. In vertical SaaS, the growth premium is even more pronounced because industry-specific TAMs are well-defined, making high-growth companies appear scarce. This single factor explains the largest share of the gap.

2. Smaller Revenue Base Premium (+0.8x)

VC-stage vertical SaaS companies often have $5M–$50M in revenue, meaning each dollar is “worth more” because it can plausibly multiply 5–10x over the investment horizon. M&A targets typically have $50M–$500M+ in revenue, where the law of large numbers limits upside. ModMed at $500M+ revenue was valued at ~10.6x; a $20M ARR healthcare SaaS startup might command 15–20x in a VC round. Smaller companies carry higher per-dollar growth expectations, directly inflating multiples.

3. Future Exit Optionality (+0.5x)

VC investors model based on future exit value — what the business will be worth in 5–7 years — and price in the optionality of multiple possible outcomes (IPO, strategic sale, or secondary). Strategic M&A buyers and PE firms model acquisitions based on current cash flow and identifiable synergies. VC investors also price embedded fintech optionality aggressively (payments, lending, insurance layered onto the SaaS platform), while M&A buyers tend to value only realized fintech revenue. This time-horizon and optionality gap consistently adds 0.3–0.7x to VC entry multiples.

4. Downside Protection (+0.4x)

VC investments are minority stakes with structural protections — liquidation preferences, anti-dilution clauses, board seats, and information rights — that limit downside risk. M&A buyers acquire 100% of the business and assume 100% of the risk: integration complexity, employee retention, competitive disruption, and technology obsolescence. Because VC investors face an asymmetric risk-reward profile (limited downside, uncapped upside), they can afford to pay higher entry multiples. Notably, while M&A buyers do pay a control premium for full ownership, this premium is more than offset by the total risk they absorb.

Figure 5: Bridge analysis showing how four structural factors add +2.7x to M&A multiples (5.8x) to reach VC entry multiples (8.5x)

💡 Practical Takeaway for Vertical SaaS Founders: If you raise a VC round at 10x revenue, don’t assume you’ll exit via M&A at 10x. The median vertical SaaS M&A multiple of 5.8x means you need to grow into your valuation — or build embedded fintech revenue streams that justify premium exit multiples. The Rule of 40 matters: companies scoring above 50 on Rule of 40 consistently exit at 7x–9x ARR in M&A. Add embedded payments generating 30%+ of revenue, and the exit multiple can reach 9x–12x.

🤝 Preparing for a raise or exit?

SaasRise CEO masterminds connect you with SaaS founders who have recently raised rounds, sold companies, or navigated PE transactions. Learn from their experience — not just the data.

Join the SaasRise Community →6. Vertical vs. Horizontal Multiples Over Time (2020–2026)

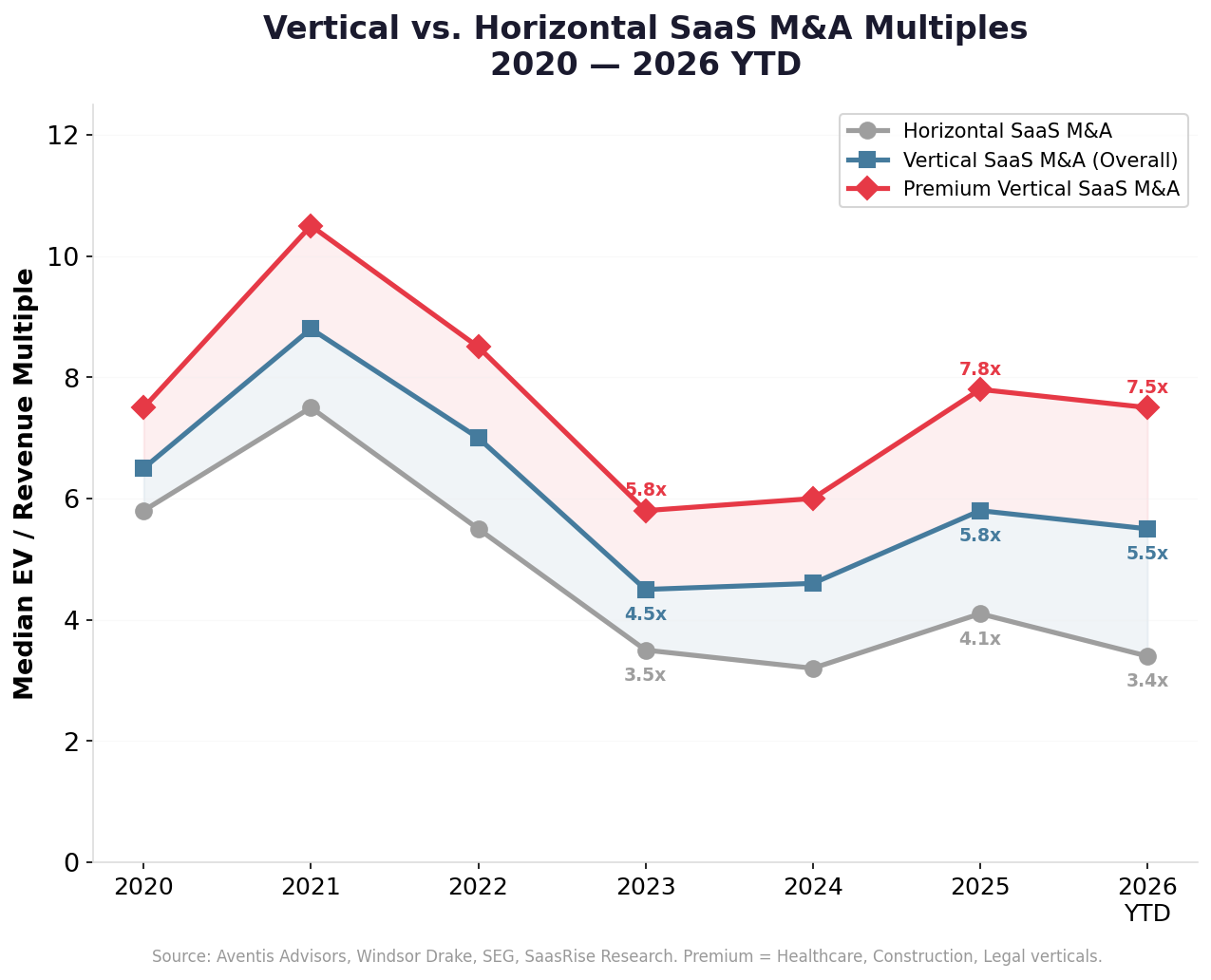

Vertical SaaS M&A revenue multiples have consistently outperformed horizontal SaaS across the full valuation cycle. The chart below shows the trajectory from the COVID-era boom through the 2022–2024 correction and into the current bifurcated market, highlighting the growing gap between vertical and horizontal SaaS.

Figure 6: Vertical vs. Horizontal SaaS M&A median revenue multiples from 2020 through 2026 YTD

Key Trends in Vertical vs. Horizontal Multiples

- 2020–2021 (Boom): Both vertical and horizontal SaaS surged during the pandemic. Vertical SaaS peaked at 8.8x in 2021, while horizontal SaaS reached 7.5x. Premium verticals (healthcare, construction) hit 10.5x. The gap between vertical and horizontal was modest (~1.3x turns) because all SaaS was riding the same wave.

- 2022–2024 (Correction): The valuation correction hit horizontal SaaS harder. Horizontal multiples fell 57% from peak to a 3.2x trough in 2024, while vertical SaaS fell only 48% to 4.6x. The difference? Vertical SaaS retention remained strong (GRR >90%) even as horizontal tools faced churn from budget cuts and AI substitution.

- 2025 (Bifurcation): The gap between vertical and horizontal widened dramatically. Vertical SaaS rebounded to 5.8x while horizontal recovered only to 4.1x — a 41% premium, up from ~10% in 2024. Premium vertical categories reached 7.8x, nearly double the horizontal median.

- 2026 YTD (Compression with Vertical Resilience): Broader SaaS multiples compressed as AI disruption fears intensified (Aventis Advisors reports median at 3.4x). Vertical SaaS softened slightly to 5.5x but maintained its premium, while premium verticals held at 7.5x. The gap between vertical and horizontal is now the widest in the data set’s history at 2.1x turns.

💡 Why Vertical SaaS Outperforms in Downturns: During the 2022–2024 correction, vertical SaaS multiples fell 48% peak-to-trough versus 57% for horizontal SaaS. Three factors explain this resilience: (1) vertical software is mission-critical infrastructure — a restaurant can’t remove Toast, a law firm can’t remove Clio; (2) embedded fintech revenue is recession-resistant because it’s tied to transaction volume, not discretionary software budgets; (3) regulatory compliance requirements prevent customers from switching even under budget pressure.

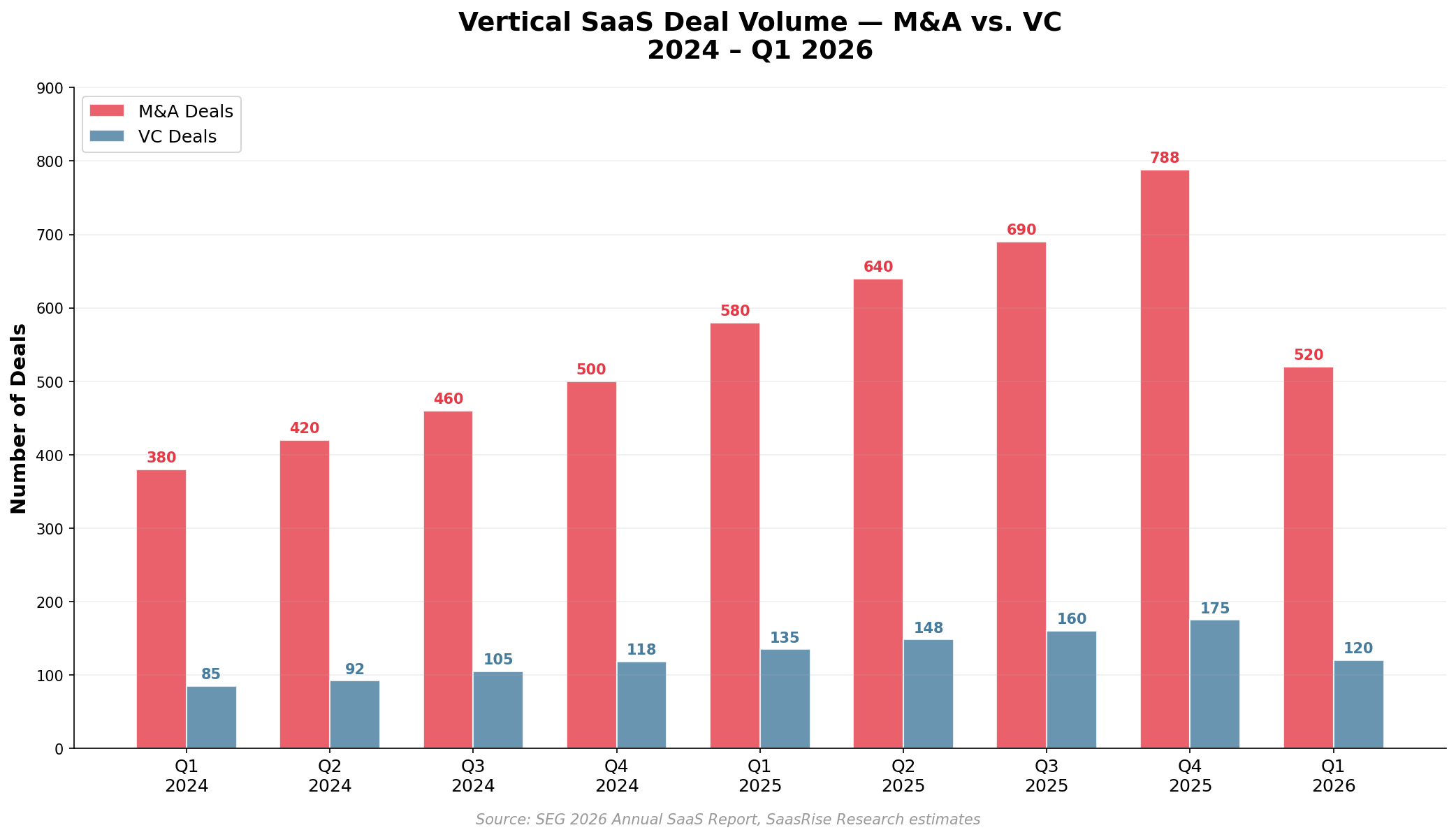

7. Deal Volume & Market Activity

Vertical SaaS M&A deal volume reached record levels in 2025. According to data aggregated from SEG, PitchBook, and Euclid Ventures, the vertical SaaS sector saw approximately 1,275+ M&A transactions (46–54% of the 2,698 total SaaS deals) and 2,300+ VC rounds (53% of all VC deal volume) between January 2025 and April 2026.

Figure 7: Vertical SaaS M&A and VC deal activity by quarter, January 2025 — Q1 2026

Who Is Buying Vertical SaaS?

The acquirer landscape for vertical SaaS breaks into three categories:

Private Equity Buyers (57% of deals):

- Thoma Bravo — Olo ($2.0B restaurant SaaS), Quorum Software (energy, sold to Francisco Partners), portions of Boeing Digital

- Clearlake Capital — ModMed ($5.3B healthcare SaaS), the largest vertical SaaS PE deal in history

- TPG — Sabre Hospitality Solutions ($1.1B), expanding into hotel property management SaaS

- Francisco Partners — Quorum Software (~$800M energy SaaS) from Thoma Bravo

- Sumeru Equity Partners — JobNimbus ($330M roofing operations SaaS)

- TA Associates — iBase-t (manufacturing MES for aerospace & defense)

- Blackstone — Entrata ($200M minority at $4.3B valuation, property management)

Strategic Buyers (35% of deals):

- Xero — Melio ($2.5B) to add embedded SMB payments to its accounting platform

- Coursera — Udemy ($2.5B merger) to create the world’s largest EdTech skills platform

- Veeva Systems — Ostro ($100M) for AI-powered brand engagement in life sciences

- Procore — Datagrid (~$250M, construction AI), Novorender & FlyPaper (BIM capabilities)

- Rocket Companies — Redfin ($1.75B) and Mr. Cooper ($9.4B) for vertically integrated real estate

Vertical Platform Acquirers (8% of deals):

- Cotiviti (KKR-backed) — Edifecs ($3.1B) to build a healthcare data and interoperability platform

- Clio — vLex ($1.0B) to build end-to-end legal technology suite

- Fleetio — Auto Integrate (~$500M) to create one-stop fleet maintenance platform

A notable trend is the emergence of vertical SaaS platforms as acquirers. As highlighted by SaasIntelligence and Euclid Ventures, leading vertical SaaS companies like Procore, Clio, Toast, and Veeva are now consolidating their industries through M&A, rather than being acquisition targets themselves. This “platform play” dynamic is unique to vertical SaaS and reflects the maturation of the sector.