Anthropic’s Claude Mythos is the most capable AI model ever released. But the bigger story isn’t the model itself — it’s what it reveals about where the SaaS industry is headed. The cost of a unit of AI intelligence has fallen 150x in three years while capability has nearly tripled. For SaaS CEOs, this creates the most asymmetric opportunity since the shift to cloud: AI isn’t replacing software, it’s expanding what software can do. The winners will be the companies with distribution, brand, and fundamentals — not wrappers riding the hype.

This report is published by SaasRise, the #1 mastermind community for experienced SaaS CEOs with $1M–$100M+ in ARR. Members collectively have $3B+ in ARR.

The AI Era in Numbers

📋 Table of Contents

- The Claude Mythos Moment — What Just Changed

- The Token Intelligence Curve — A New Law for the AI Era

- AI Is a Subset of Software — The Optimistic Case

- The New Moats — Distribution, Brand, and Data

- Foundation Models Are NOT in a Bubble

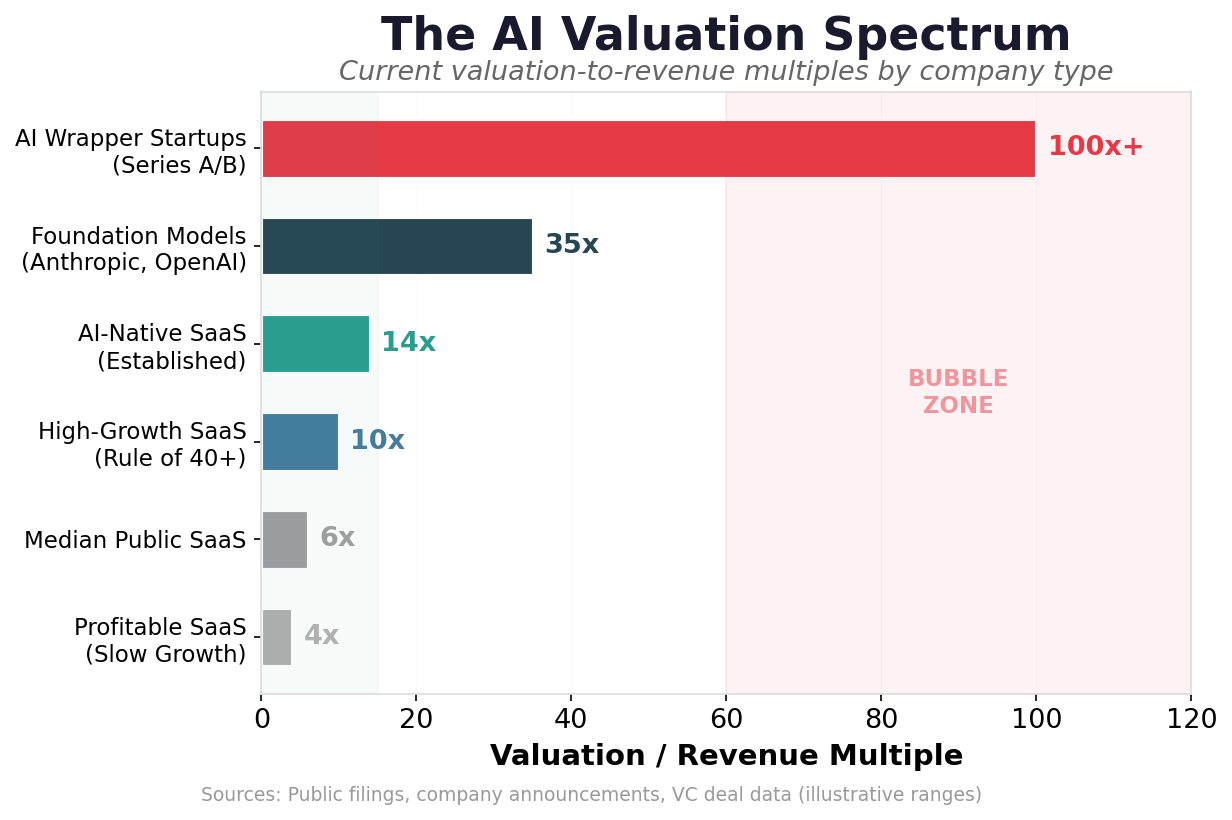

- The AI Wrapper Bubble — Where the Froth Is

- The Post-IPO Market Reset — Return to Fundamentals

- The Benedict Evans Counterpoint — Will Model Companies Keep Their Margins?

- How SaaS CEOs Should Position for the Mythos Era

- The 15-Year Outlook — Optimism Grounded in Reality

- Sources & Methodology

1. The Claude Mythos Moment — What Just Changed

On April 7, 2026, Anthropic first disclosed Claude Mythos — the most capable AI model ever built — initially making it available to select enterprise partners. On June 9, Anthropic publicly released Claude Mythos 5 alongside Claude Fable 5. At $10 per million input tokens and $50 per million output tokens, Mythos represents a step-change in what AI can do: deep multi-step research, agentic coding workflows, and reasoning at a level that consistently surpasses expert humans on the hardest benchmarks.

This isn’t just another model release. It’s a marker — the moment the SaaS industry has to reckon with a fundamental question: What happens when intelligence becomes a commodity?

To understand why that question matters, look at the progression. Claude has evolved from Haiku (a fast, cheap model for simple tasks) through Sonnet (the workhorse) and Opus (the thinker) to Mythos — a model that can read an entire codebase, understand the business logic, write tests, refactor the architecture, and deploy a working feature. Claude Code, Anthropic’s coding agent built on these models, hit $1 billion in annualized revenue within about six months of its May 2025 public launch — and by February 2026 had surged to $2.5 billion ARR.

For SaaS CEOs, the implication is immediate: your product roadmap just accelerated. What used to take a team of five engineers six months can now be scoped, prototyped, and shipped in weeks. The companies that recognize this — and embed AI deeply into their products and workflows — will pull ahead. The ones that treat it as a bolt-on feature will fall behind.

Key Insight: Claude Mythos isn’t the destination — it’s a waypoint. The models will keep getting better, faster, and cheaper. The question for SaaS CEOs isn’t “Should I use AI?” — it’s “How fast can I rebuild my product around it?”

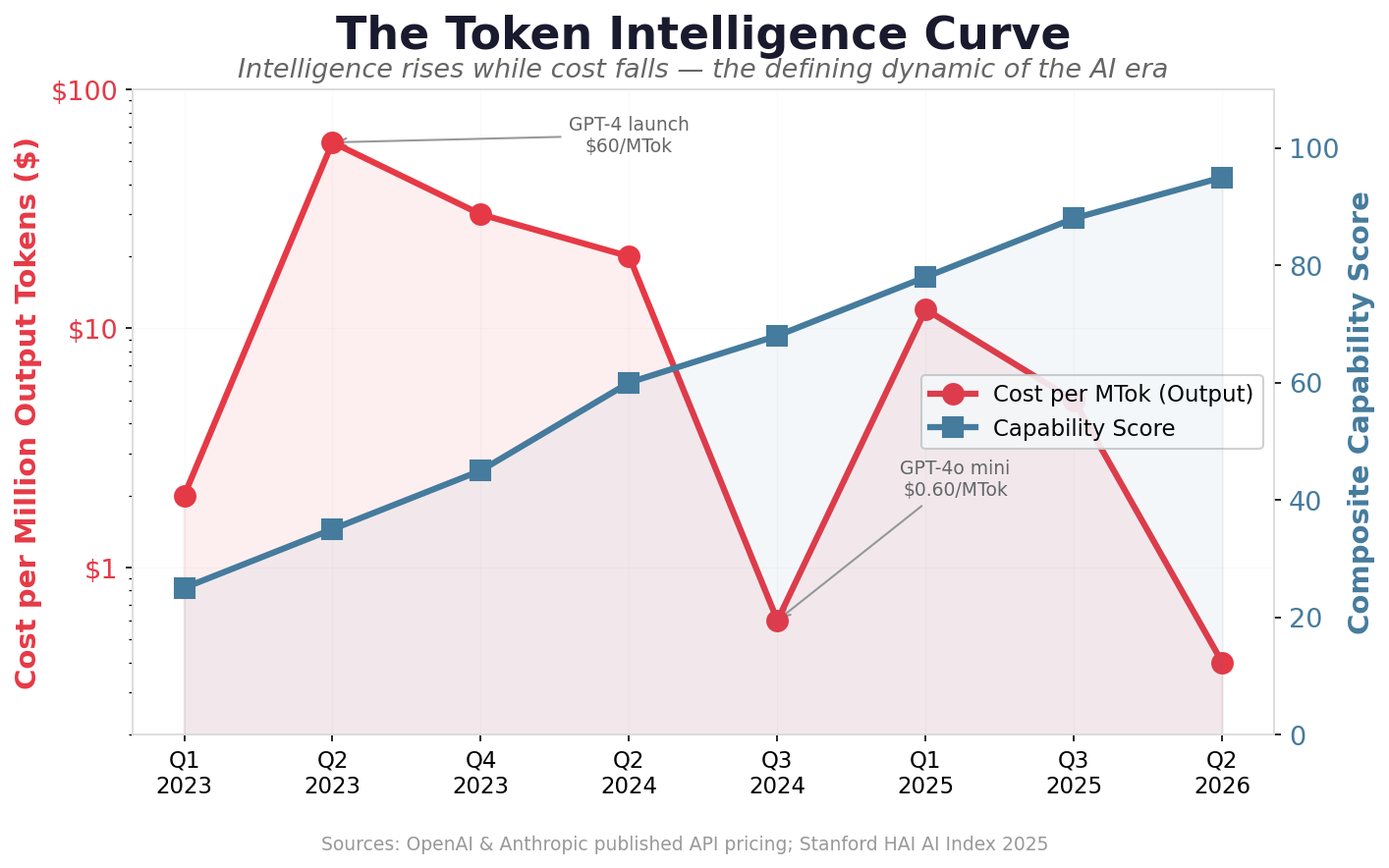

2. The Token Intelligence Curve — A New Law for the AI Era

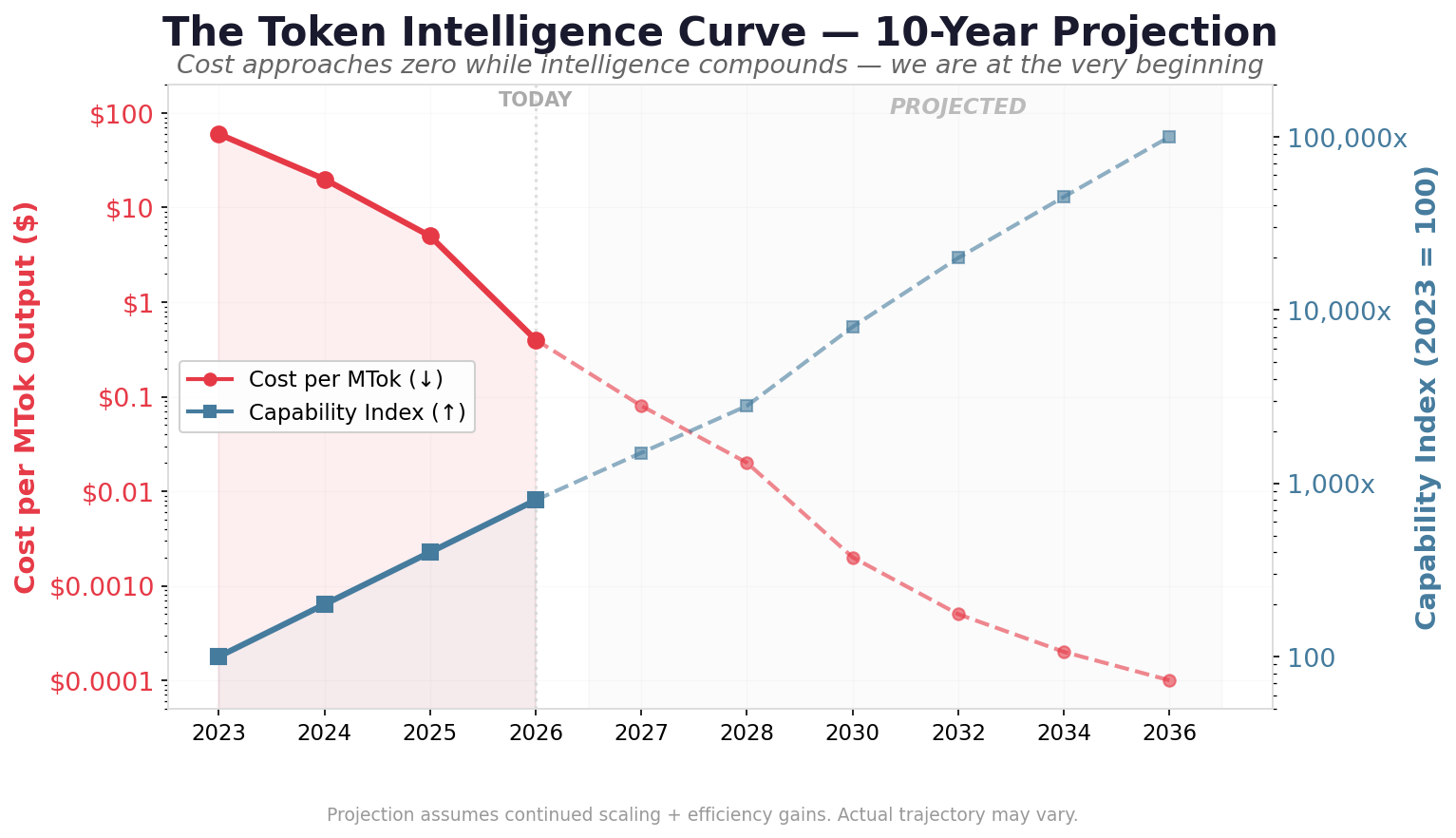

There is a pattern emerging in AI that is as reliable as Moore’s Law was for semiconductors, and it may prove even more consequential. We call it the Token Intelligence Curve:

The Token Intelligence Curve

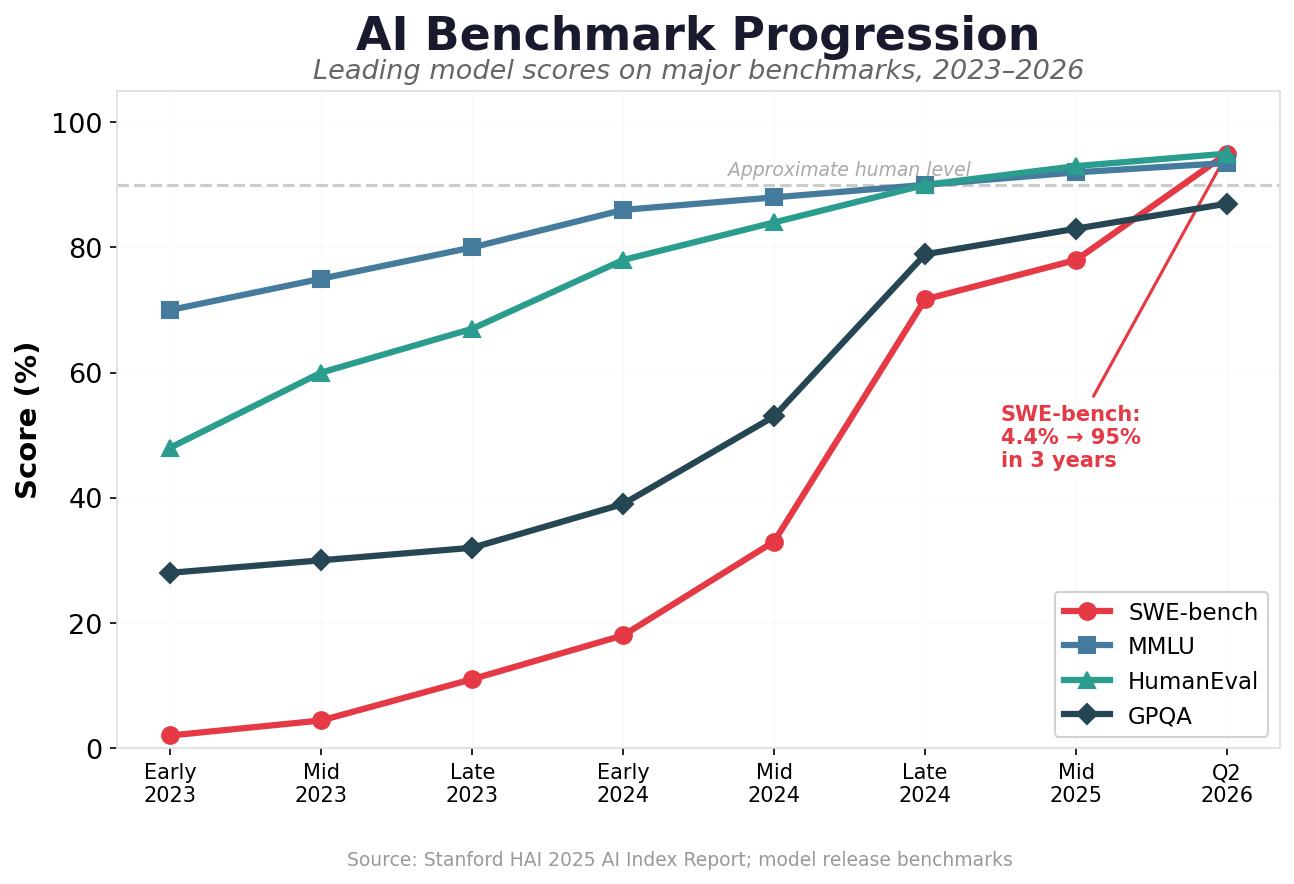

Per-token intelligence rises exponentially while per-token cost falls exponentially. The cost to achieve a fixed level of AI capability drops by approximately 10x every 12–18 months, while the frontier capability of the best models roughly doubles in the same period.

Consider: when GPT-4 launched in March 2023, it cost $60 per million output tokens. That was the only way to get GPT-4-level intelligence. Today, models that match or exceed GPT-4’s capability — like GPT-4o mini and GPT-5 nano — cost $0.40 per million tokens. That’s a 150x cost reduction in just over three years, while the frontier (Claude Mythos, GPT-5.2) has leapt far beyond what GPT-4 could do.

Figure 1: The Token Intelligence Curve — cost to match GPT-4 quality falls 150x while frontier capability nearly triples

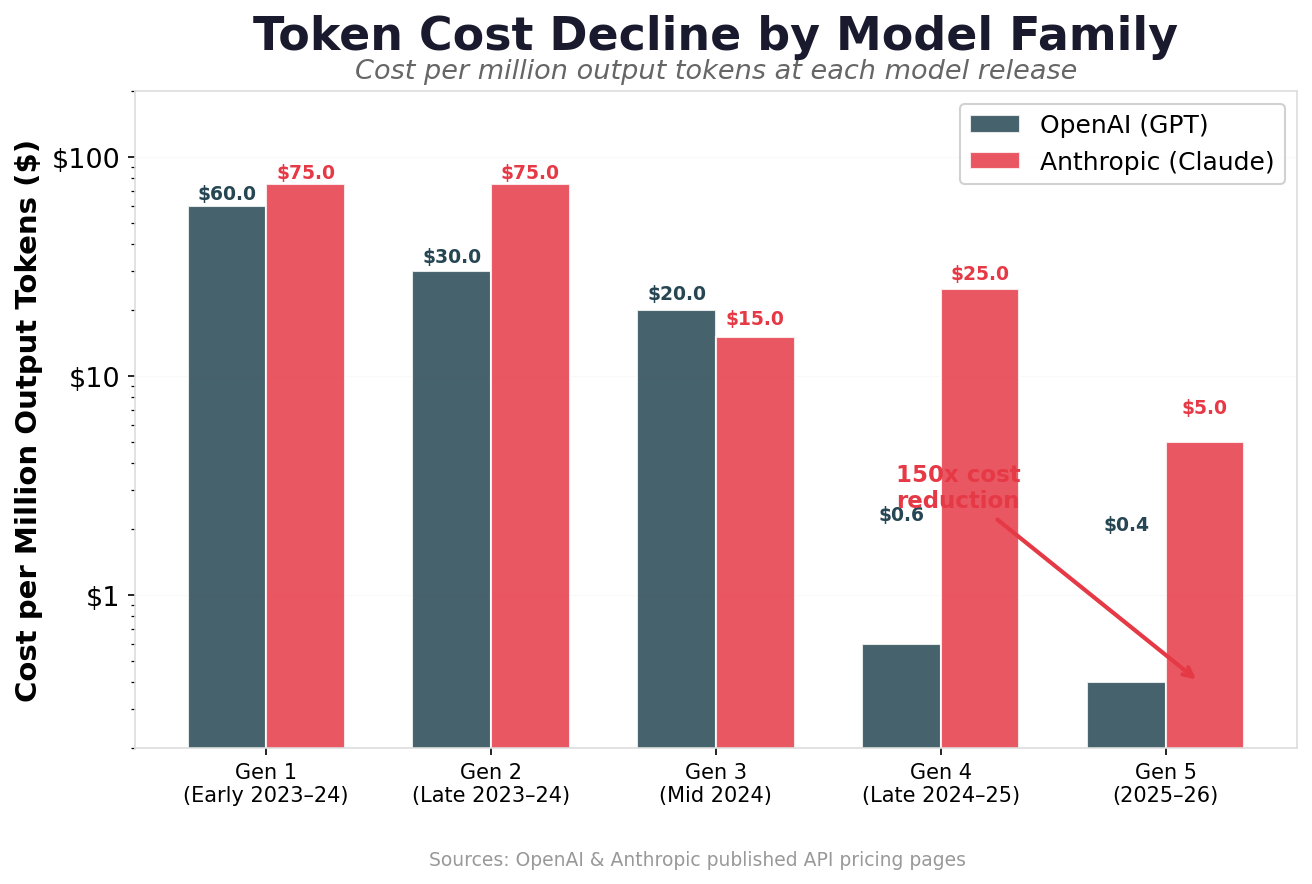

The numbers are striking. On SWE-bench Verified — a benchmark that measures an AI’s ability to resolve real GitHub issues — the best model scored 4.4% in mid-2023. By late 2024, that had jumped to 71.7%. As of June 2026, Claude Fable 5 leads at 95.0%, with Claude Opus 4.8 at 88.6% and GPT-5.5 at 82.6%. On GPQA, a graduate-level science benchmark, scores rose by nearly 49 percentage points in two years. Researchers have documented dramatic improvements in parameter efficiency — meaning models achieve the same capability with drastically fewer resources.

Figure 2: Token cost decline by model family — both OpenAI and Anthropic show dramatic price compression across generations

This isn’t just about price drops. It’s about the compounding of two exponential curves. When intelligence goes up and cost goes down simultaneously, the result is an explosion in what’s economically feasible. Use cases that were absurdly expensive 18 months ago — like having an AI review every customer support ticket and draft a personalized response — are now pennies per interaction.

What the Token Intelligence Curve means for SaaS CEOs: Every product feature that requires intelligence is getting cheaper to deliver. The AI that cost you $10,000/month to run 18 months ago now costs $66. Plan your product roadmap accordingly — capabilities that seem expensive today will be essentially free within two years.

Scale Smarter with SaasRise

Join 400+ SaaS CEOs and founders in the #1 mastermind community for growth, scaling, and exit prep. Weekly mastermind calls with peers who’ve been there.

Apply to Join →3. AI Is a Subset of Software — The Optimistic Case

There’s a persistent narrative that AI will destroy the software industry. It won’t. AI is expanding it.

Technology analyst Benedict Evans, in a recent episode of Lenny’s Podcast (“The most rational take on AI you’ll hear this year,” May 2026), made this point with a vivid historical parallel. He showed an IBM ad from 1961 that reads: “An IBM electronic calculator… replaces 150 engineers.” The pitch is nearly identical to what you’d read in a Claude Code marketing page today. And yet, there are more engineers alive today than at any point in human history. The calculator didn’t eliminate engineering — it made engineering accessible to more people and expanded what engineering could accomplish.

“Even if models stopped getting better tomorrow, this is still an incredibly useful technology.”

— Benedict Evans, Lenny’s Podcast (May 2026)

Evans draws the VisiCalc analogy: when the first spreadsheet software arrived, people predicted it would eliminate accountants. Instead, it made financial modeling so cheap and fast that companies did more of it. The number of accountants grew. This is Jevons paradox applied to intelligence — when the cost of something drops dramatically, total consumption increases by more than the cost decrease.

This isn’t theoretical. We’re seeing it happen in real time. One SaasRise member — the CEO of a social media management SaaS company with over $20M in ARR — recently told the group: “We will not exist in five years as we exist today.” But rather than retreating, he’s investing. His team is rebuilding the entire product around AI, launching an AI-native version that does in seconds what previously required a marketing team and weeks of work.

As he put it: “I told the team we have to disrupt ourselves. That’s the first step.”

This is precisely the lesson from Clayton Christensen’s The Innovator’s Dilemma. I had Christensen as a professor at Harvard Business School in 2012 — about eight years before he passed away — and his core teaching was clear: the companies that survive disruption are the ones willing to cannibalize their own products before someone else does. The ones that protect their existing business at the expense of the future are the ones that die.

For SaaS CEOs, the optimistic case is this: AI isn’t shrinking the market for software. It’s making software able to do things that previously required expensive human judgment. Every workflow that was “too complex to automate” is now automatable. The total addressable market for software is growing, and the companies that embed AI into their products will capture a disproportionate share of that growth.

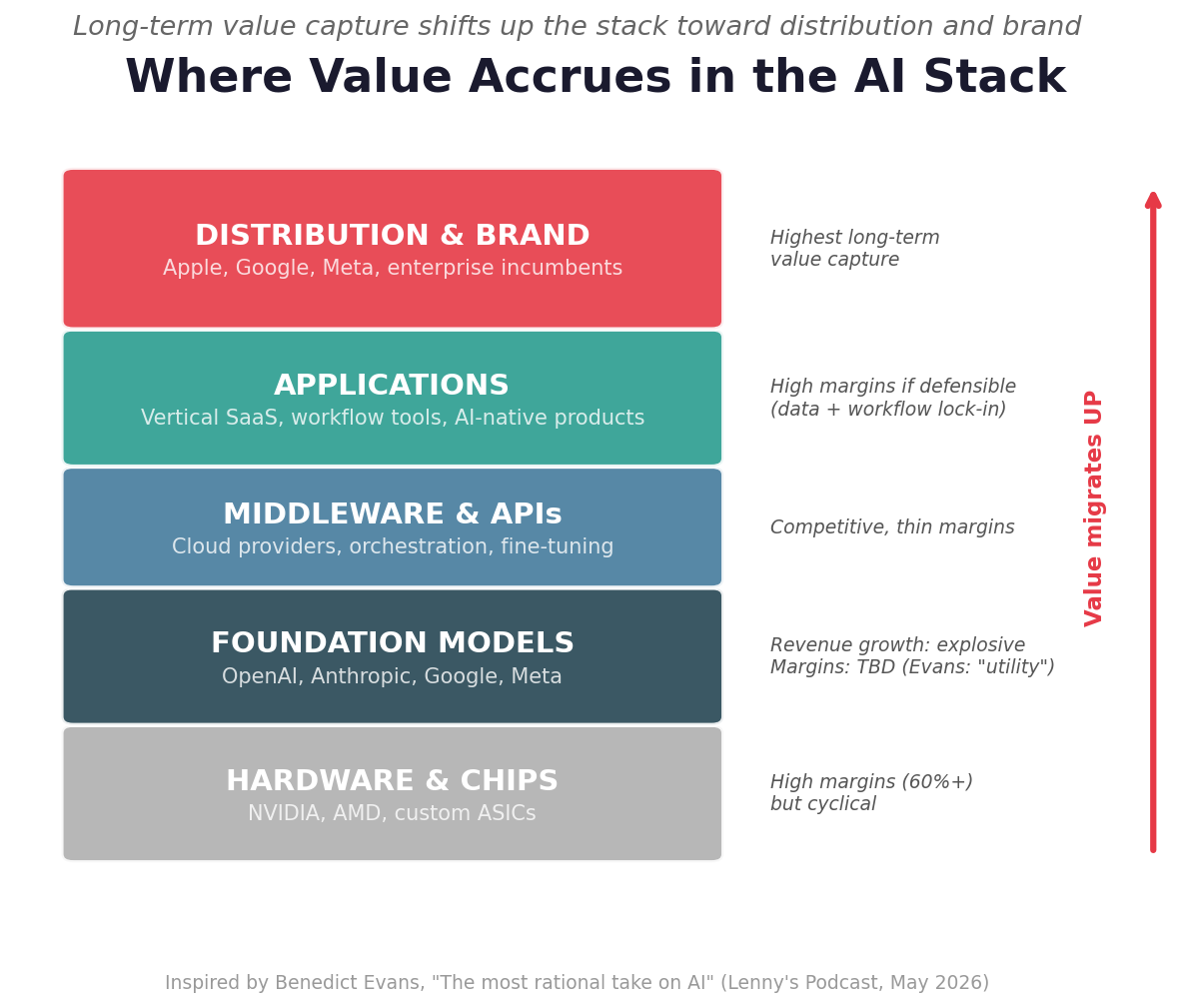

4. The New Moats — Distribution, Brand, and Data in the AI Era

If AI models are becoming commodities — and they are — then the competitive advantage shifts up the stack. The model is the infrastructure. The value is in what you build on top of it.

Benedict Evans frames this through the browser analogy: Microsoft won the browser war through distribution, bundling Internet Explorer with every copy of Windows. But the real value didn’t accrue to the browser maker — it went further up the stack to companies like Google, Facebook, and Amazon that built applications on top of the open web. The browser became invisible infrastructure.

We’re watching the same pattern play out with AI models. Google is spraying Gemini across every product. Meta is embedding Llama into Instagram, WhatsApp, and Facebook. Apple Intelligence runs on a billion edge devices. The model itself is becoming a utility — like electricity or cloud compute. Nobody asks which AWS region powers their favorite app. Soon, nobody will ask which LLM powers their favorite SaaS product.

Figure 3: Where value accrues in the AI stack — long-term value migrates up toward distribution and brand

For SaaS CEOs, this means the moat has shifted. The five defensible assets in the AI era are:

The Five AI-Era Moats

- Distribution: How many customers do you reach? How embedded are you in their workflows? Switching costs matter more than ever.

- Brand: In a world where anyone can build an AI-powered tool in a weekend, trust and reputation become the differentiator. Customers buy from brands they know.

- Proprietary Data: The model is commodity. Your customer data, usage patterns, and domain-specific training data are not. Every interaction with your product makes your AI better — and harder to replicate.

- API Integrations & Partnerships: Deep integrations with the tools your customers already use create lock-in that no standalone AI tool can match.

- Workflow Embedding: If your product is the system of record for a critical business process, you’re defensible. If you’re a thin layer over an API, you’re not.

The model is commodity infrastructure — like AWS powering applications. The companies that own the customer relationship, the data, and the distribution will capture the lion’s share of value. The ones that are “basically reselling tokens,” as Evans puts it, will not.

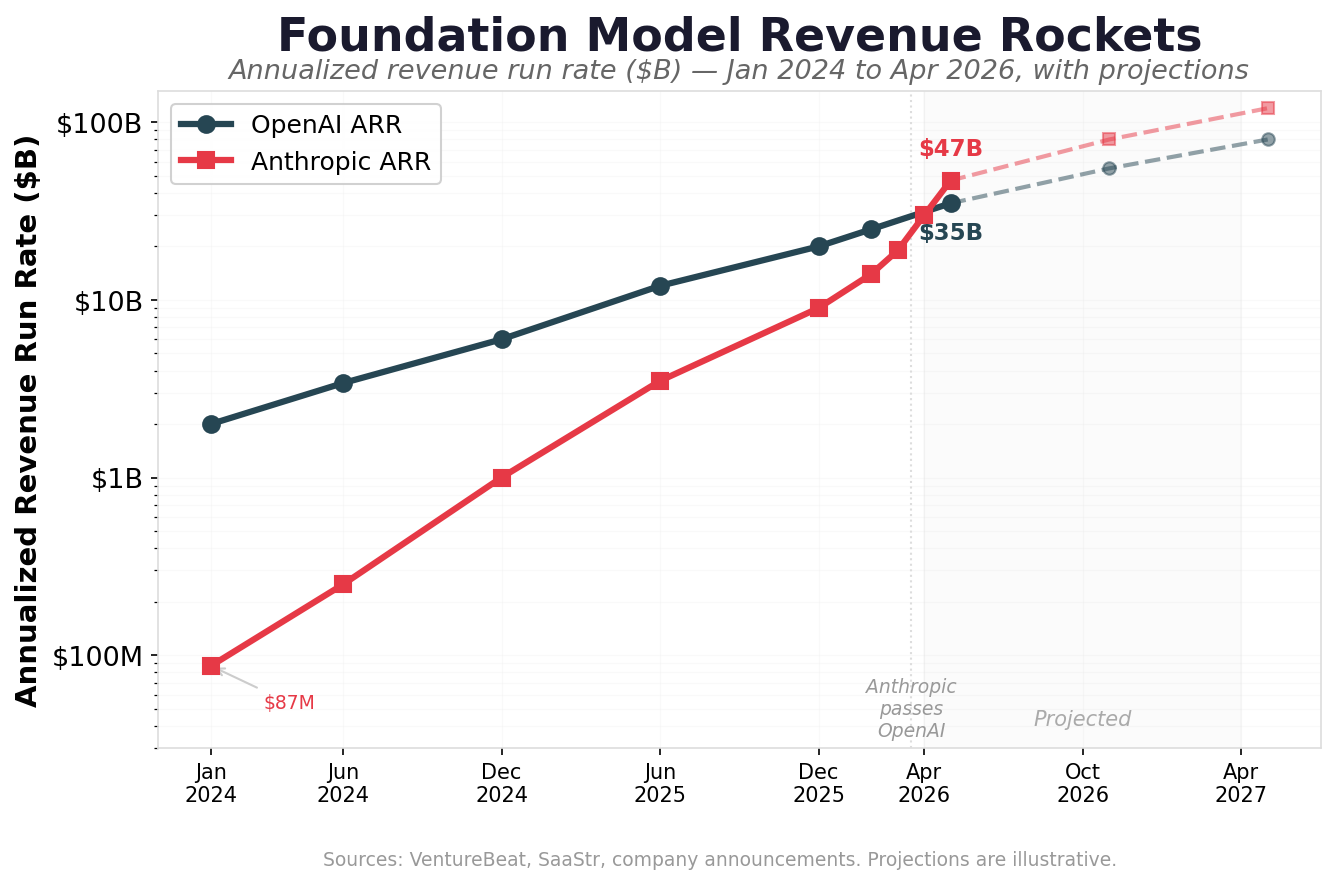

5. Foundation Models Are NOT in a Bubble

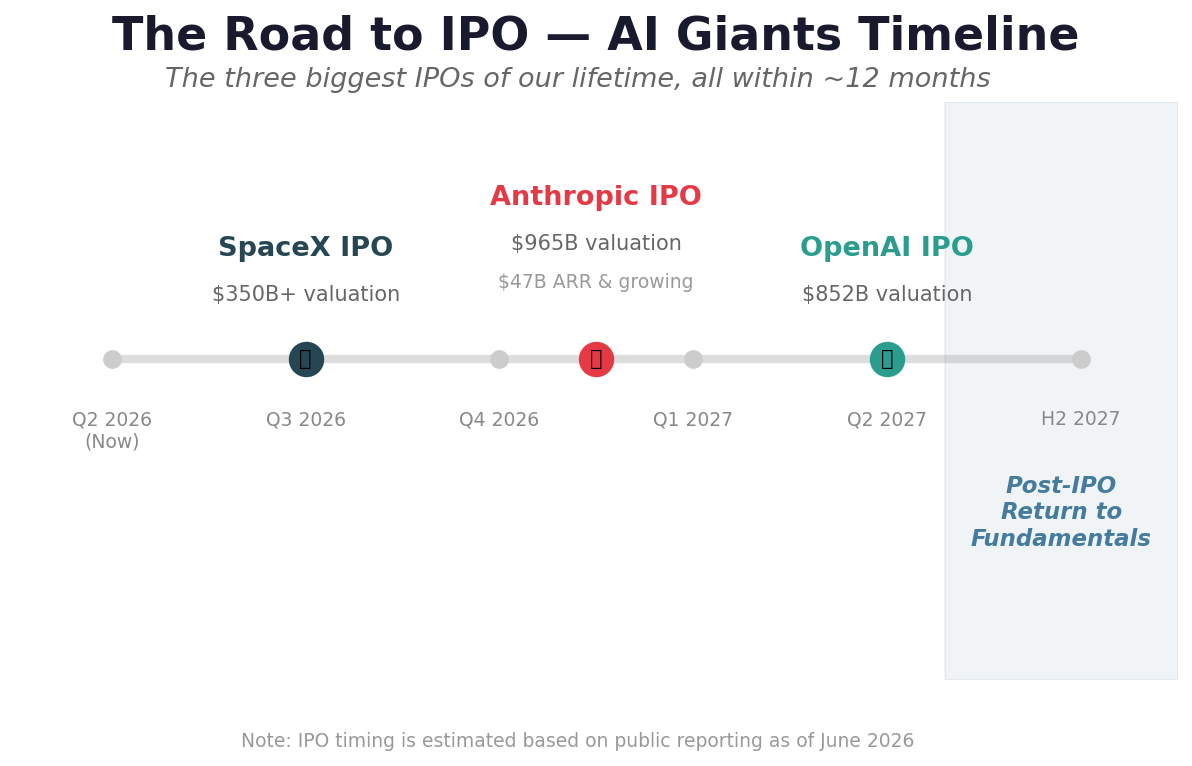

Let’s address the elephant in the room. Are the big AI model companies overvalued? OpenAI at $852 billion. Anthropic at $965 billion after its May 2026 Series H. Are these bubble valuations?

No. And the revenue numbers tell you why.

Anthropic has executed what may be the most extraordinary revenue trajectory in the history of enterprise software. In January 2024, the company was doing roughly $87 million in annualized revenue. By December 2024, it hit $1 billion. By December 2025, it reached $9 billion. By April 2026 it crossed $30 billion, and as of its Series H announcement on May 28, Anthropic disclosed a run-rate of $47 billion in annualized revenue. OpenAI, meanwhile, has climbed to roughly $35 billion ARR as of May 2026. Combined, the two leading foundation model companies are generating over $82 billion in annualized revenue — a figure that was essentially zero three years ago.

Figure 4: Foundation model revenue rockets — Anthropic hit $47B ARR by May 2026, surpassing OpenAI

Claude Code alone — a single product — hit $1 billion in ARR within roughly six months of its May 2025 public launch, then doubled to $2.5 billion ARR by February 2026. There is no precedent for this kind of revenue velocity in enterprise software. Slack took about seven years to reach $1 billion ARR. Zoom took about seven as well. Claude Code did it in six months — and then doubled it again three months later.

| Date | OpenAI ARR | Anthropic ARR | Key Milestone |

|---|---|---|---|

| Jan 2024 | $2.0B | $87M | Anthropic at seed-stage revenue |

| Dec 2024 | $6.0B | $1.0B | Anthropic crosses $1B |

| Jun 2025 | $12.0B | $3.5B | Claude Code launches |

| Dec 2025 | $20.0B | $9.0B | Claude Code hits $1B ARR |

| Feb 2026 | $25.0B | $14.0B | OpenAI hits $2B/month |

| Apr 2026 | ~$25.0B | $30.0B | Anthropic surpasses OpenAI |

| May 2026 | ~$35.0B | $47.0B | Both accelerating; combined $82B ARR |

At its $965 billion valuation (Series H, May 2026) against $47 billion in ARR, Anthropic trades at roughly 20x revenue. That’s a premium — but for a company that grew revenue from $1 billion to $47 billion in 17 months, it’s remarkably restrained. For context, Salesforce trades at approximately 4x revenue with 12% growth. Anthropic is growing orders of magnitude faster, and the gap is narrowing fast: Anthropic has told investors it expects to be profitable in Q2 2026, with quarterly revenue projected at $10.9 billion — which would put it on a $43 billion+ annualized pace. By the time Anthropic IPOs, the multiple could compress to single digits.

OpenAI’s $852 billion valuation (its last private round; it has since filed a confidential S-1 targeting up to $1 trillion at IPO) against roughly $35 billion in current ARR is approximately 24x — pricing in the company’s massive consumer install base (ChatGPT with 900 million+ weekly active users), developer platform, and the prospect of achieving artificial general intelligence. OpenAI is projecting a $14 billion loss in 2026 as it invests in compute infrastructure, but revenue growth remains strong at $2 billion per month.

The fundamental thesis is straightforward: these companies are building the infrastructure layer that every application in the economy will eventually run on. If software ate the world, AI is eating software. OpenAI and Anthropic alone are already valued at nearly $2 trillion combined, generating over $82 billion in ARR. A combined valuation of $4 trillion or more for the leading foundation model companies is not unreasonable on a 3–5 year horizon if revenue trajectories hold — particularly with Anthropic achieving profitability and both companies approaching or exceeding $100 billion in annualized revenue by year-end.

The bottom line: Foundation models are expensive, but they’re growing into their valuations at an unprecedented pace. The revenue is real, growing, and enormous. This is not tulips.

Benchmark Your SaaS with the Best

SaasRise members share real revenue, churn, and growth data in a confidential peer group. Get the benchmarks you can’t find anywhere else.

Learn More →