Should Your SaaS Firm Add On Professional Services Revenue?

Services revenue makes enterprise SaaS founders nervous, but done right it's one of your best retention tools. Here's how to use forward deployed engineers and implementation services to lock customers in without sinking your software multiple.

Almost every enterprise SaaS founder I talk to has the same quiet worry the moment services revenue starts to grow. One founder in our mastermind put it well recently. He'd spent years telling people, "we're a software company, not a services company." Then his customers started coming back for a second, third, and fourth project, and the services line kept climbing. He was making good money on it, retention was going up, and he still felt nervous, because he'd run a services business before and sold it for one times revenue while software was trading at many multiples of that.

That tension is real and worth taking seriously. But the answer isn't to refuse services out of principle. It's to understand what services are doing for your business, structure them so they help rather than hurt, and keep the mix inside a range a future acquirer will still reward. The founders who solve this well end up with stickier customers and a more valuable company, not a less valuable one.

Services are how you get the customer "bolted down"

The phrase one founder kept using was "bolting down" the customer, and it's the right mental model. In enterprise SaaS, the biggest threat to your revenue isn't a competitor stealing the account. It's the customer who bought the software, never really implemented it, and quietly churns at renewal because they never got value. Services are the fastest way to close that gap. When his team started offering short implementation packages, roughly a project manager for forty hours, customers who got live on their first real process inside thirty days retained at dramatically higher rates, by orders of magnitude.

The data backs this up. Customers who reach first value within about two weeks retain at 80 percent or higher a year later, while those who don't get there within the first month retain at something like 35 to 50 percent. That swing is almost entirely determined in the first few weeks. And most customers won't get there on their own: industry activation rates hover around 37 percent, meaning fewer than four in ten signups ever experience the core thing your product is supposed to do. Services are how you drag that number up.

What surprised the founder most wasn't the upfront demand. It was that customers kept coming back. One state agency started as what looked like a single forty-hour project and, by the end of the year, was on track to consume around a thousand hours of one person's time, because they kept finding new things they wanted done. He wasn't chasing that revenue; the customer was pulling it out of him. And the strategic point: that agency was also buying more licenses, so the services person became instantly profitable and everything else they did for other prospects was effectively free.

If you're weighing whether services are worth the operational hassle, keep three things in front of you:

- Get to first value fast. The retention gap between customers who reach value in two weeks and those who stall past a month is enormous, so services should be aimed squarely at that window.

- Expect the pull, not just the push. Customers who get real help early tend to come back for more work on their own, which is a sign the services are landing rather than a problem to solve.

- Count the license lift. Services that also drive more seats can pay for themselves, making everything else that person does effectively free.

The forward deployed engineer model, and what Palantir figured out

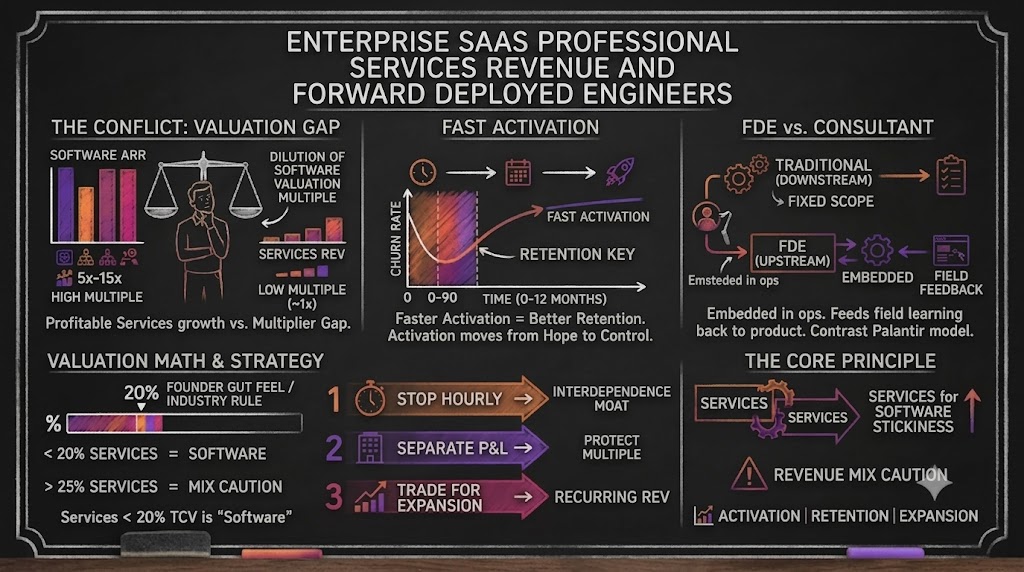

There's a specific version of this worth naming, because it's become the reference model for the category. Palantir built its business around what it calls forward deployed engineers, people who embed directly with the customer, write real code against the customer's data, and own the loop from raw data to a working decision. Early on, Palantir deploys these engineers close to cost to get the platform genuinely wired into the customer's operations. Once the workflows are established, the heavy engineering tapers off and the relationship becomes higher-margin software. Their professional services have historically run around 18 to 20 percent of revenue, and the model is a big part of why their commercial business has grown the way it has.

Another founder runs the same playbook at a smaller scale, selling to mid-market companies that have budget but no internal team to deploy the software. The software might be a modest annual number, and the first-year professional services attached to it can be four or five times that, delivered as forward deployed engineers who integrate the product into the customer's daily operations. The next year the services drop way down, often to a premium support or advisory tier at roughly ten percent of the software cost, while the software revenue grows. As he described it, that first-year services money isn't a distraction from the software. It's what pays for the custom integration that gets the product truly embedded, which is exactly what protects the renewal.

A few things make this model work rather than turn into a consulting shop:

- Over-invest early, on purpose. The engineering is deployed near cost at the start because its job is to make the software impossible to rip out, not to be a profit center in year one.

- Tie it to activation you control. Self-serve onboarding kept stalling because customers wouldn't follow through. Putting a person in the room, pulling the right departments onto calls, and reporting weekly moved activation from the customer's hands into his.

- Let the services taper. The whole point is that year-two services shrink while software keeps growing. If services stay flat as a share of the account forever, you've built a services business, not a software one.

One accounting note that trips people up: Palantir reports forward deployed engineering revenue inside its services line, not as pure subscription. Some operators combine the two in how they talk about it, and you can argue it either way, but be honest with yourself internally. If you're calling labor revenue "ARR," you're fooling yourself and eventually your investors. Know which dollars are recurring software and which are people-driven services, because the market knows the difference.

The ratio that actually matters for valuation

Here's the part that keeps founders up at night, and it's legitimate. Buyers do not pay the same multiple for every dollar of revenue. When services grow faster than software, your blended gross margin drops even if each line is individually healthy, and acquirers notice immediately. The numbers to keep in mind:

- Know your margin per line. Subscription software typically runs 75 to 85 percent gross margin; implementation, onboarding, and consulting usually run 20 to 40 percent.

- Watch the blended number. When services outgrow software, blended margin falls even if both lines are healthy, and that's what a buyer underwrites.

- Mind the buyer's cutoff. Most buyers want software gross margin above 75 percent, and below roughly 70 percent blended they start digging into your costs and discounting the multiple.

The rough benchmarks are worth memorizing. Across SaaS companies, professional services tend to sit around 15 percent of total revenue at the median, and many experienced operators treat 20 percent as a soft ceiling, measured as services against subscription revenue. So the fear the founder expressed, that going from a few percent services toward 15 or 18 percent might change how a buyer sees the company, is a reasonable instinct. His own line in the sand was that he'd get nervous above 20 percent, and that's a sensible place to draw it.

The clearest way to see why the mix matters is in the multiples themselves. Recurring software revenue gets valued on a revenue multiple, and for most private SaaS companies that lands around three to five times ARR, more for fast growers with strong margins. Services revenue, because it's labor-driven and doesn't recur cleanly, typically gets valued at roughly one times. That's the gap a member pointed to offhandedly: whatever you do, you'll get three to four times on the software and about one on the services. A dollar booked as subscription can be worth four or five dollars of enterprise value, while the same dollar in services is worth about one. So a mix that drifts from 5 percent services to 20 percent doesn't just dent your margin, it reprices a chunk of your revenue at a fraction of the multiple.

But notice what the benchmark is really saying. Fifteen percent services is normal and healthy. The problem isn't having services. The problem is letting them run past the point where the market still reads you as a software company that uses services to drive adoption, rather than a services company that happens to sell some software.

Keeping services from taking over the company

So how do you get the retention benefits without waking up one day as a body shop? A few practical moves came out of the discussion, and they line up with what works across the industry.

- Productize the common work. Figure out what you can turn into a fixed, repeatable package. If a job is 40 hours of work but 150 hours of value to the customer, price it on the value and standardize the delivery instead of billing hours.

- Watch the attach rate as a real metric. Track services revenue per new deal explicitly, and set a trajectory for it to decline over time as your product gets easier to deploy. What gets measured here doesn't drift.

- Consider a separate entity for the messy long tail. One founder suggested spinning the heavier services work into its own small business with its own P&L owner. It isolates the services margin from your software financials and removes the acquisition risk of looking services-heavy.

- Push the truly custom work to partners when you can. For work outside your packages, a good consulting partner can carry it, sometimes paying a referral fee or bringing you deals in return, so you stay focused on subscription revenue.

That last one comes with a warning. Founders have been burned handing work to partners who assigned junior people or treated the engagement as filler between bigger contracts, then had to rescue the project to keep the customer happy. There's a structural risk too: one founder watched a strong services partner win a large multi-year government contract and disappear overnight, because a pure services shop will always chase the biggest deal. If partner quality keeps failing you, that's the signal to bring the work in-house and productize it rather than keep outsourcing your customer's first impression.

The balance to aim for

If I had to compress all of this into a single operating principle, it's the one another member offered almost in passing: as long as it improves churn and speeds up onboarding, do the services. Priced against that one-times multiple, they're close to free from a valuation standpoint while doing real work to protect the recurring base underneath. The mistake isn't selling services. It's selling services that don't make the software stickier, or letting the mix drift so far the market stops seeing the software at all.

So keep the software at the center. Use services, including forward deployed engineers, to get customers live, prove value in the first few weeks, and bolt the product into their operations so deeply that leaving becomes unthinkable. Watch the ratio, aim to stay comfortably under that 20 percent line, let services taper as the product matures, and be honest about which dollars are recurring and which aren't. Do that, and services stop being a threat to your company's value and become one of the best retention tools you have.