Open-Source or Closed-Source AI: Which Should You Build Your SaaS Business Upon?

This report examines one of the most consequential infrastructure decisions facing SaaS companies in 2026: whether to build AI-powered products on top of proprietary models from Anthropic, OpenAI, and Google, or on open-weight alternatives like DeepSeek, GLM, Qwen, Kimi, Llama, and Mistral. We analyze the latest benchmark data, pricing, privacy implications, and business model dynamics to help SaaS CEOs and founders make informed architecture choices. Our research draws on current market data through July 2026, enterprise adoption surveys, and pricing from official API documentation. The bottom line: the answer is not a simple either/or, but the default is shifting faster than most companies realize.

This report is published by SaasRise, the #1 mastermind community for SaaS CEOs with $1M–$100M+ in ARR. Members have collectively raised $1B+ and have $3B+ in ARR.

Key Numbers Shaping the Decision

📋 Table of Contents

- The Great AI Architecture Question

- What "Open-Weight" Actually Means (And Why It Matters)

- The Current Model Landscape — Mid-2026

- Where Open-Weight Has Caught Up (And Where It Hasn’t)

- The Cost Equation — The #1 Driver

- Self-Hosting: When It Makes Sense (And When It Doesn’t)

- Data Privacy, Security & Compliance

- U.S. vs. Non-U.S. Models — The Geopolitical Landscape

- Strategic Independence & Vendor Lock-In

- Use-Case Playbook — What to Use Where

- The Hybrid Architecture — The Winning Playbook

- Are Anthropic & OpenAI’s Business Models at Risk?

- How Frontier Capability Diffuses to Open Weights

- Recommendations & Action Plan

Key Report Findings:

The best AI architecture for a SaaS company in 2026 is not "all proprietary" or "all open-weight." It is a hybrid model-routing architecture that uses open-weight models as the default for high-volume, cost-sensitive, and privacy-sensitive workloads while selectively routing to proprietary frontier models for the hardest tasks. Companies that have built exclusively on Claude or GPT should begin diversifying now. Open-weight models like GLM-5.2, DeepSeek V4 Pro, and Qwen 3.6 now match or exceed proprietary models on most benchmarks at 5–34x lower cost. The frontier capability gap has compressed from roughly 18 months to 6–12 months, and API prices for mid-tier tasks have collapsed over 90% in two years. For SaaS companies running AI agents in the background for every customer, this is no longer a technical curiosity — it is a margin and competitive strategy question.

1. The Great AI Architecture Question

Two years ago, the question for SaaS companies was simple: "Should we integrate AI into our product?" That question has been answered decisively — yes. The new question, and the one this report addresses, is fundamentally different: "Which AI models should we build on, and how should we architect our AI stack?"

This is not an abstract technology debate. It directly impacts four things every SaaS CEO cares about:

- Gross margin — AI model costs (called "inference costs") can become one of the largest line items in your cost of goods sold. Choosing the wrong model at the wrong price can destroy your unit economics.

- Data privacy — When you send your customers' data to an AI model provider's API, that data leaves your control. Some customers, especially in healthcare, finance, and enterprise software, care deeply about this.

- Vendor dependence — If your entire product depends on one model provider, you are exposed to their pricing changes, outages, model deprecations, and strategic decisions.

- Product quality — The smartest model is not always the best model for every task. Sometimes a specialized, cheaper model will outperform a general-purpose expensive one.

Enterprise AI spending hit $8.4 billion by mid-2025 and is projected to reach roughly $15 billion by end of 2026. Average enterprise AI spend on LLMs has risen from approximately $4.5 million to $7 million per company, and enterprises expect it to grow another 65% this year. The stakes are high enough that the architecture decision deserves serious analysis, not default inertia.

Figure 1: Enterprise LLM API spend by provider, 2023 vs. 2025. Anthropic's rise from 12% to 40% is the defining shift. (Source: Menlo Ventures)

The market dynamics tell the story: Anthropic has surged from 12% to 40% of enterprise LLM API spend in just two years, driven almost entirely by Claude Code's dominance in software development workflows. OpenAI dropped from 50% to 27%. Google climbed from 7% to 21%. The top three providers now account for roughly 88% of enterprise LLM API usage — but that concentration is exactly what creates risk for companies that bet everything on one provider.

2. What "Open-Weight" Actually Means (And Why It Matters)

Before diving into the analysis, we need to clear up terminology that even experienced technologists mix up. The distinction matters because it affects licensing, deployment options, and what you can actually do with a model.

🔓 Open-Weight Models

The developer releases the trained model "weights" — think of these as the model's learned knowledge, packaged as a downloadable file. You can run the model on your own servers, fine-tune it with your own data, and modify it for your use case. However, the company typically does not share the training data, training code, or exact recipe used to create the model.

Examples: DeepSeek V4 Pro, GLM-5.2, Qwen 3.6, Kimi K2.7, Llama 4, Gemma 4, Nemotron 3, Mistral, MiniMax M3, gpt-oss

🔒 Proprietary / Closed Models

The developer keeps everything behind an API. You send text to their servers, they process it, and send a response back. You cannot download the model, see how it works, run it on your own infrastructure, or customize it beyond basic prompt engineering.

Examples: Claude Opus 4.8, GPT-5.5, Gemini 3.1 Pro, Grok 4.3

💡 Why the distinction matters for SaaS companies: With an open-weight model, you can run it inside your own cloud environment so customer data never leaves your infrastructure. You can fine-tune it on your domain data to make it better at your specific use case. And you can pin it to a specific version so your product behavior doesn't change when the model provider decides to update. None of this is possible with a proprietary model.

3. The Current Model Landscape — Mid-2026

The AI model landscape has changed dramatically. Two years ago, the conversation was simple: use GPT-4 or Claude for anything hard, and maybe use an open model for experiments. Today, the competitive field is both deeper and more global, with several open-weight models matching or exceeding proprietary models on key benchmarks.

The Proprietary Leaders

Anthropic is the breakout story of 2026. Claude Code has taken the software development world by storm, driving Anthropic's run-rate revenue past $47 billion as of May 2026 — nearly double OpenAI's ~$24 billion. Anthropic's enterprise API market share reached approximately 40%, with 54% of the enterprise coding market. The company reached profitability in Q3 2026, filed for IPO in June, and is valued at $965 billion. Claude Opus 4.8 remains one of the strongest models for complex, long-horizon coding tasks and agentic workflows.

OpenAI retains enormous consumer reach with approximately 900 million weekly active ChatGPT users, generating roughly $24 billion in annualized revenue. GPT-5.5 is a strong all-rounder. However, ChatGPT's market share slipped below 50% for the first time in June 2026, and the company is projecting a $14 billion loss for the year.

Google has emerged as a serious third player with Gemini 3.1 Pro performing well on coding and multimodal tasks, and its Flash/Lite models offering compelling price-performance for high-volume workloads.

The Open-Weight Leaders

| Model | Provider | HQ | License | Price (Input/Output per 1M tokens) | Best At |

|---|---|---|---|---|---|

| GLM-5.2 | Zhipu AI (Z.ai) | Beijing, China | MIT | $1.40 / $4.40 | #1 open-weight on AI Intelligence Index (score: 51). Strong math, coding, and reasoning. |

| DeepSeek V4 Pro | DeepSeek | Hangzhou, China | MIT | $0.435 / $0.87 | Lowest cost frontier model. Competitive coding (80.6% SWE-bench Verified). |

| Kimi K2.5–K2.7 | Moonshot AI | Beijing, China | MIT | ~$1.00 / $3.00 | Best long-horizon agentic behavior. 200–300 sequential tool calls. |

| Qwen 3.5/3.6 | Alibaba | Hangzhou, China | Apache 2.0 | ~$1.00 / $2.50 | Largest open-weight ecosystem (113,000+ derivatives on HuggingFace). |

| MiniMax M3 | MiniMax | Shanghai, China | Modified MIT | ~$1.20 / $3.50 | First open-weight combining frontier coding + 1M context + native multimodality. |

| Nemotron 3 Ultra | NVIDIA | Santa Clara, USA | NVIDIA Open | Varies (self-host) | Top U.S. open benchmark scores. 5x throughput. Built for agentic workflows. |

| Llama 4 Maverick | Meta | Menlo Park, USA | Llama License | ~$1.00 / $1.50 | Huge ecosystem. Multimodal. 1M context window. 400B total parameters. |

| Gemma 4 31B | Mountain View, USA | Apache 2.0 | ~$0.30 / $0.50 | Best quality-to-size ratio. Runs on a single GPU. Excellent for local deployment. | |

| gpt-oss-120b | OpenAI | San Francisco, USA | Apache 2.0 | Varies (self-host) | Strong reasoning and agentic capabilities. Full tool-use support. |

| Mistral Large | Mistral AI | Paris, France | Apache 2.0 | ~$2.00 / $6.00 | European sovereignty. Strong EU AI Act compliance story. |

Prices from official API documentation and third-party hosting as of July 2026. Self-hosted model costs vary by infrastructure.

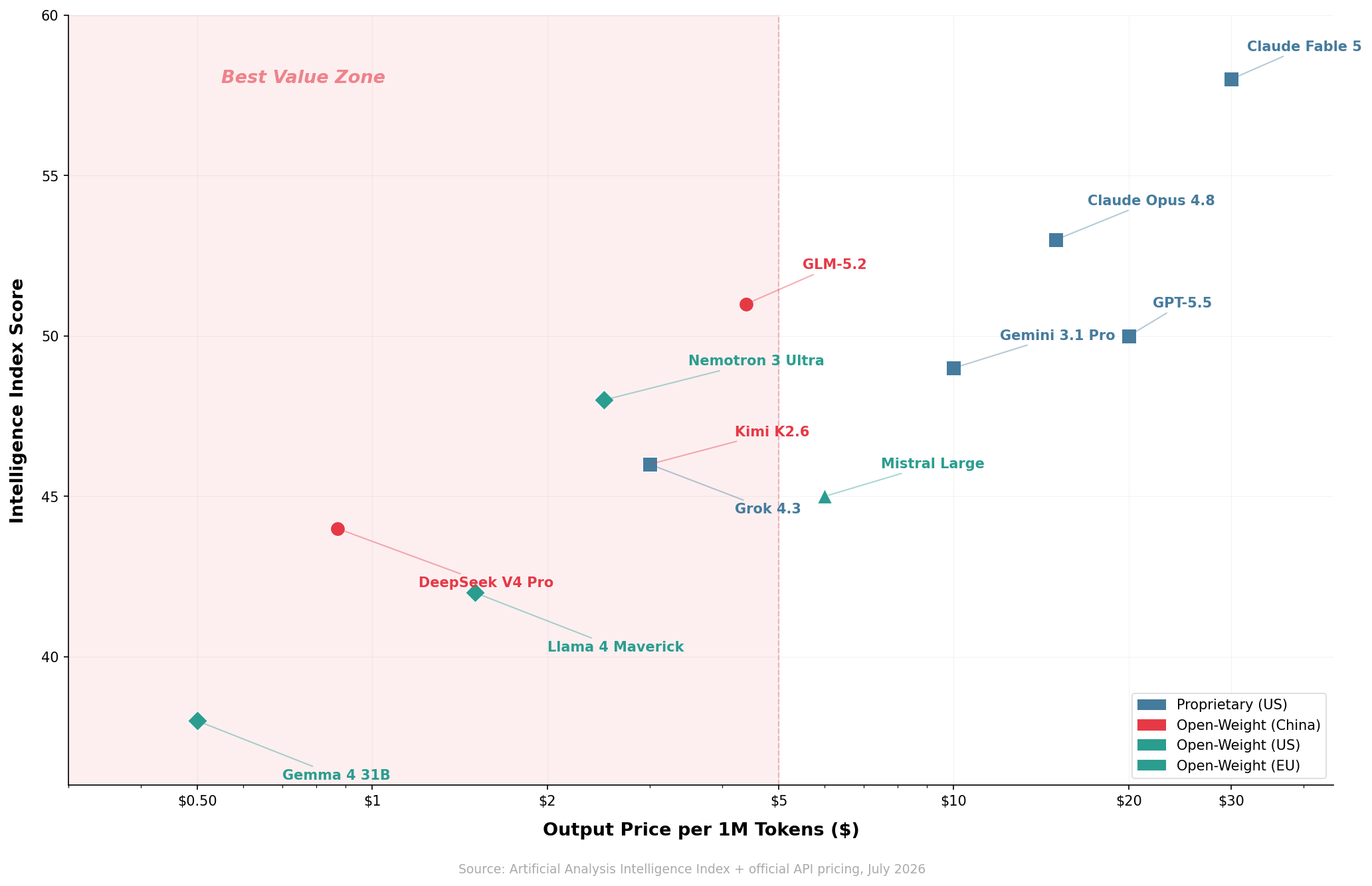

Figure 2: Intelligence Index score vs. output token price. Open-weight models (red, teal) cluster in the "best value zone" — high quality at a fraction of proprietary cost.

Scaling Your SaaS to $10M+ ARR?

Join 200+ SaaS CEOs who share growth strategies, benchmark metrics, and AI infrastructure best practices every week.

Join SaasRise →4. Where Open-Weight Has Caught Up (And Where It Hasn’t)

Here is the honest picture, without either the "open-source will eat everything" hype or the "proprietary is still miles ahead" dismissal:

Where Open-Weight Has Reached Parity

- Raw coding benchmarks: GLM-5.2 scored 73.33 on LiveBench Agentic Coding — beating GPT-5.4 Thinking (70.00). DeepSeek V4 Pro Max achieved 80.6% on SWE-bench Verified, tying Gemini 3.1 Pro.

- Math and reasoning: On standard math benchmarks, open-weight models from Qwen, GLM, and DeepSeek now trade wins with proprietary models regularly.

- General intelligence: GLM-5.2 ranks #4 overall on the Artificial Analysis Intelligence Index (score: 51), just 2 points behind Claude Sonnet 5 (53), and only 7 behind the frontier Claude Fable 5 (58).

- Token efficiency: Some open models like MiMo-V2.5-Pro reach comparable capability using 40–60% fewer tokens per task, which means faster responses and lower cost even at the same per-token price.

Where Proprietary Still Leads

- Hardest long-horizon tasks: On SWE-bench Pro — which tests the ability to fix complex, real-world software bugs autonomously — proprietary models still score around 90% versus 59–67% for the best open models. This is where Claude and GPT still justify their premium.

- Cross-category consistency: Proprietary models tend to perform well across every category simultaneously. Open models spike on specific benchmarks but can be weaker on others.

- Multi-step agent reliability: When an AI agent needs to plan, execute, recover from errors, and complete a complex workflow over many steps, proprietary models still fail less often. This is particularly important for production software and autonomous agents.

- Browsing and OS-level agents: Tasks that require navigating websites, controlling a desktop, or operating system-level automation still favor proprietary models.

Figure 3: Artificial Analysis Intelligence Index scores. GLM-5.2 (#1 open-weight) is within striking distance of proprietary leaders.

💡 The practical takeaway: For roughly 70–80% of production AI tasks in a typical SaaS product — summarization, classification, data extraction, content drafting, code generation, customer support triage — open-weight models are now "good enough" or better. The remaining 20–30% of tasks where proprietary models genuinely outperform are typically the hardest, lowest-volume, highest-value tasks. A smart architecture uses different models for different tiers of work.

5. The Cost Equation — The #1 Driver

For most SaaS CEOs, cost is where this decision gets real. The pricing gap between proprietary and open-weight models is not a small optimization — it is a structural difference that can determine whether your AI features are profitable or a cash furnace.

The Raw Numbers

Figure 4: API pricing per million tokens across proprietary and open-weight models. DeepSeek V4 Pro output tokens cost 34x less than GPT-5.5.

Let’s make this concrete. If your product processes 1 million tokens per day (a moderate workload for a SaaS product with AI features), here’s what you’d pay monthly:

Figure 5: Monthly API cost at three volume levels. The gap between proprietary and open-weight compounds dramatically at scale.

Why This Matters Even More for Agentic Workflows

Here’s something many SaaS founders miss: agentic AI workflows multiply token usage by 10–100x compared to a simple chatbot.

A basic chatbot generates one response per user request. An AI agent, on the other hand, might plan its approach, call tools, inspect results, retry if something failed, validate its own output, branch into sub-tasks, and generate a final response. The same user-visible action can consume 10 to 100 times more tokens behind the scenes.

If your product runs AI agents in the background for every customer, every day — for things like data enrichment, report generation, monitoring, or automated workflows — then model cost is not just an engineering line item. It becomes a strategic margin issue that directly affects your gross margin and ability to scale profitably.

💡 Real-world example: A SaaS company running background AI agents for 1,000 customers, each consuming 10M tokens/day of agentic workflows, would spend approximately $157,500 per month on GPT-5.5 versus $5,760 per month on DeepSeek V4 Pro. That’s a difference of over $1.8 million per year — enough to fund an entire engineering team. Companies using intelligent model routing (sending easy tasks to cheap models, hard tasks to expensive ones) report 30–50% cost reductions compared to single-model architectures.

6. Self-Hosting: When It Makes Sense (And When It Doesn’t)

One of the advantages of open-weight models is that you can download them and run them on your own servers ("self-hosting"), potentially cutting costs to near-zero marginal cost per token. But the reality is more nuanced than "free model = free inference."

The Hidden Costs of Self-Hosting

The rule of thumb from infrastructure analysis: self-hosting costs 3–5x the raw GPU rental price once you add everything needed to run it in production:

- GPU rental or purchase: The base cost everyone calculates.

- DevOps labor: $750–$3,000/month minimum for monitoring, patching, model updates, and incident response.

- Infrastructure overhead: Autoscaling, load balancing, logging, metrics — $200–$500/month.

- Idle capacity waste: You pay for GPUs 24/7 even when demand is low.

- Model update cycles: Every 2–4 months, a better model comes out and you need to evaluate, test, and deploy it. Budget $40K–$100K/year in engineering time.

Figure 6: Cumulative cost comparison over 12 months at 200M tokens/month. Self-hosting beats proprietary APIs but rarely beats open-weight APIs.

When Self-Hosting Genuinely Wins

- Regulatory compliance forces it: Your customers or regulators require that data never leave your infrastructure.

- Sustained volume above 100M+ tokens/month: At this volume, the economics tilt in your favor — but only if GPU utilization stays high.

- You need domain fine-tuning: Training a model on your specific data to improve accuracy for your use case.

- Latency is critical: Running a model close to your users can reduce response time.

The Pragmatic Middle Ground

For most SaaS companies, the best path is hosted open-weight APIs — services like Together, DeepInfra, Fireworks, or the model providers' own APIs (DeepSeek, GLM, Qwen). You get most of the cost benefit of open-weight models with zero infrastructure burden. Self-hosting can come later when you have both the volume and the team to justify it.

How Do Your AI Costs Compare?

SaasRise members benchmark their infrastructure spend, AI costs, and gross margins against peers. See where you stand.

Benchmark Your SaaS →7. Data Privacy, Security & Compliance

For SaaS companies handling customer data — especially in healthcare, finance, legal, or enterprise software — the privacy dimension of the model choice can be just as important as cost.

The Case for Open-Weight on Privacy

When you self-host an open-weight model, your customers' data never leaves your infrastructure. No third-party model provider sees the prompts or the responses. This is the strongest possible privacy posture and can be decisive for:

- HIPAA-covered health data

- Financial records and trading data

- Customer source code

- Legal documents and case files

- Enterprise trade secrets

- Any data where customers contractually require it stays within your environment

The EU AI Act, which reached full enforcement for general-purpose AI rules in August 2025, includes specific exemptions for open-weight model providers from some compliance obligations — as long as the model's license meets the Act's definition of "free and open-source." This creates a regulatory advantage for open-weight models in European markets.

The Counterargument: Proprietary APIs Have Gotten Better

To be fair, the major proprietary model providers have significantly improved their privacy terms:

- OpenAI: API data is not used to train models by default. Zero-data-retention (ZDR) arrangements available for eligible customers.

- Anthropic: Offers standard and zero-data-retention API arrangements. Enterprise terms provide strong contractual protections.

- Google: Paid Gemini API prompts and responses are not used to improve products. ZDR options available.

However, even with these improvements, sending data to a third-party API is still a data-boundary event. Some enterprise customers and regulated industries simply will not accept it, regardless of the contractual protections.

Geopolitical Considerations

Five of the top open-weight model providers are headquartered in China. For SaaS companies using Chinese-origin models like DeepSeek, GLM, Qwen, Kimi, or MiniMax, this creates a perception challenge — even though self-hosting means data never goes to China. The Qualitate study found that DeepSeek converts well below the 73% industry average specifically due to Chinese ownership concerns around data privacy and security.

💡 Practical recommendation: If your customers are sensitive to model provenance, use U.S. or European open-weight alternatives (Nemotron, Llama, Gemma, gpt-oss, Mistral) as your default, and reserve Chinese-origin models for internal-only workloads or for customers who have no such concerns. The capability is available from both geographies.

8. U.S. vs. Non-U.S. Models — The Geopolitical Landscape

One of the most striking features of the current AI landscape is that the open-weight frontier is dominated by Chinese labs, while American companies dominate proprietary/closed models. This creates a geopolitical dimension to the architecture decision that SaaS CEOs need to understand.

Figure 7: Headquarters of the 15 leading AI model developers across 4 countries. The U.S. leads in total companies (8), but China dominates open-weight releases (5 companies, all open-weight).

The Geographic Split

- United States (8 companies): OpenAI, Anthropic, Google, Meta, NVIDIA, xAI, Microsoft, Allen AI. Mix of proprietary and open-weight, but the strongest proprietary models (Claude, GPT-5.5) are all American.

- China (5 companies): Zhipu AI (GLM), DeepSeek, Alibaba (Qwen), Moonshot AI (Kimi), MiniMax. All release open-weight models. Currently produce some of the best open-weight models in the world.

- Europe (1 company): Mistral AI (Paris). Strong EU data sovereignty story. Benefits from GDPR/EU AI Act alignment.

- Canada (1 company): Cohere (Toronto). Focused on enterprise RAG and search pipelines.

Best U.S. Open-Weight Models

For SaaS companies that want the cost and flexibility benefits of open-weight models without using Chinese-origin weights, strong American alternatives exist at every capability tier:

| Model | Company | Parameters | License | Key Strengths |

|---|---|---|---|---|

| Nemotron 3 Ultra | NVIDIA | 550B (55B active MoE) | NVIDIA Open | Tops all U.S. open benchmarks. 5x throughput vs. comparable models. Built specifically for long-running agents. |

| Gemma 4 31B | 31B dense | Apache 2.0 | Exceptional quality for size. Runs on a single GPU. Apache 2.0 is the cleanest commercial license. | |

| Llama 4 Maverick | Meta | 400B total (17B active MoE) | Llama License | Largest open ecosystem. Native multimodal. 1M context window. 113,000+ community derivatives. |

| gpt-oss-120b | OpenAI | 120B MoE | Apache 2.0 | Strong reasoning and agentic capabilities. Full tool-use and browsing support. |

| Phi-4 | Microsoft | 14B dense | MIT | Best-in-class small model. Runs on a laptop. Perfect for edge deployment and cost-sensitive tasks. |

| OLMo 3 32B | Allen AI (Ai2) | 32B dense | Apache 2.0 | The most open model on earth — fully open training data, code, and weights. Research-grade transparency. |

💡 Bottom line on geopolitics: No SaaS company needs to use Chinese-origin model weights. Strong U.S. and European alternatives exist at every tier. However, if you self-host a Chinese-origin model on U.S.-controlled infrastructure, the data never leaves your environment — the model origin becomes a procurement optics question, not a security one. Choose based on your customers' comfort level.