How to Sell Your SaaS (from a Founder with a $169m exit)

I sold my SaaS company for $169M. In this guide, I break down exactly how to sell a SaaS business—from timing and preparation to bankers, deal structure, and the mistakes that quietly cost founders tens of millions.

.jpg)

In February of 2012, I sold my company, iContact, for $169 million.

It took almost a decade to get there. We started from nothing, grew the business to more than $50M in annual recurring revenue, and eventually sold to a publicly traded company. At the time, I didn’t realize how rare it was to have a clean, competitive exit process. I only understood that later, after helping dozens of SaaS founders through exits of their own.

If you’re reading this, there’s a good chance you’ve built something real. Maybe you’re doing a few million in ARR. Maybe you’re past that and starting to get inbound interest from private equity or strategics. Either way, this post is meant to be practical. No theory. No hype. Just the actual mechanics of selling a SaaS company, based on what I lived through and what I’ve seen since.

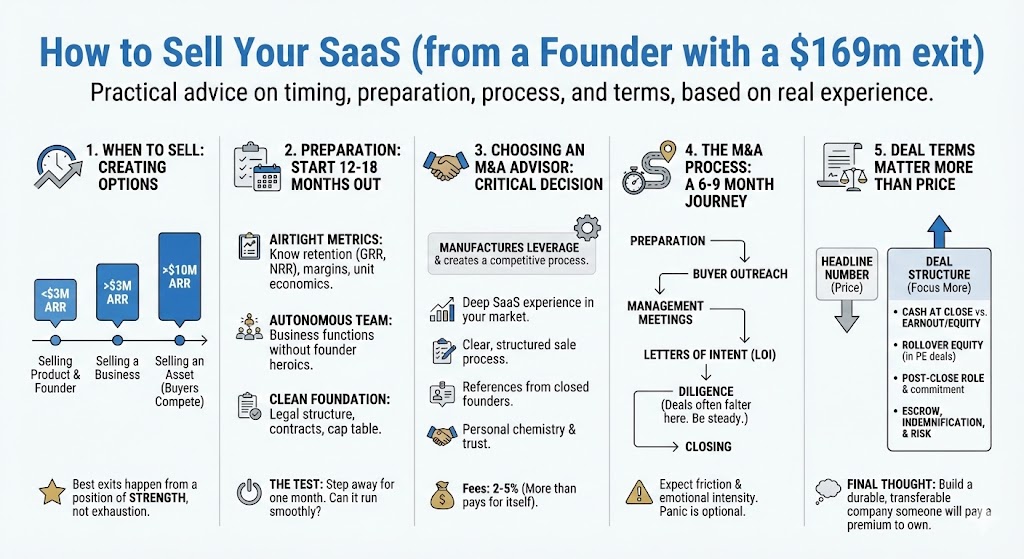

When Is the Right Time to Sell?

This is the first question founders ask, and it’s usually the wrong one. The better question is whether your company has options.

You can sell a SaaS business at almost any size, but the quality of the outcome changes dramatically as you scale. Early exits often feel good in the moment and disappointing in hindsight.

Here’s the reality most founders don’t hear early enough:

- Below $3M ARR, you’re selling a product and a founder.

- Above $3M ARR, you’re selling a business.

- Above $10M ARR, you’re selling an asset buyers compete for.

The biggest mistake I see is selling too early. Founders exit at $2M ARR and later realize that another few years of disciplined growth could have changed their family’s financial trajectory permanently. That said, waiting forever is also a mistake. Markets change. Energy fades. Personal goals evolve.

The best exits happen when performance is strong, the growth story is credible, and the founder is choosing to sell from a position of strength rather than exhaustion.

Preparing Your Company for Sale (This Starts Earlier Than You Think)

If you want a good outcome, preparation starts 12 to 18 months before you plan to close. This phase is unglamorous, but it’s where most of the value is created or destroyed.

Buyers don’t just look at growth. They look for confidence. Confidence in the numbers. Confidence in the team. Confidence that the business will keep running after you’re gone.

That means your metrics need to be airtight. You should know your retention, churn, margins, and unit economics without hesitation. But more importantly, the business needs to function without founder heroics.

There are a few things buyers consistently care about:

- Revenue quality and retention, especially GRR and NRR

- A management team that owns day-to-day execution

- Clean legal structure, contracts, and cap table

- Evidence the company can grow without the founder in every decision

One test I often recommend is stepping away for a full month. No Slack. No email. No calls. If the company struggles, buyers will sense that dependency instantly. If it runs smoothly, your leverage goes up.

.jpg)

Choosing the Right M&A Advisor

Hiring the right M&A advisor is the single most important decision in the entire process. A good advisor doesn’t just “run a sale.” They manufacture leverage.

Founders sometimes try to save money here. That almost always costs them far more than the advisor’s fee. A strong banker creates a competitive process, shapes the narrative, controls momentum, and protects you when things get tense, which they will.

What matters when choosing an advisor:

- Deep SaaS experience, ideally in your specific market

- A clear, structured process for running a sale

- References from founders who’ve actually closed

- Personal chemistry, because you’ll be working closely for months

Fees typically range from 2–5% depending on deal size, often with a small retainer. It’s not cheap, but in most cases a good advisor more than pays for themselves in higher valuation and better terms.

How the M&A Process Really Works

From the outside, acquisitions look quick. From the inside, they’re slow, intense, and emotionally draining. Expect the full process to take six to nine months once you formally begin.

At a high level, the process flows through preparation, buyer outreach, management meetings, letters of intent, diligence, and finally closing. Every one of those phases has friction.

Due diligence is where deals almost die. Buyers will find issues. Always. Your job isn’t to pretend the business is perfect. It’s to be transparent, prepared, and steady when pressure increases.

Nearly every successful deal has at least one moment where it feels like it’s falling apart. That’s normal. Panic is optional.

Why Deal Terms Matter More Than Price

Most founders focus on the headline number. That’s understandable, but it’s rarely what determines the quality of the exit.

The structure of the deal dictates how much money you actually receive, when you receive it, and how much risk you carry after the sale.

Key elements to pay close attention to include:

- How much is cash at close versus equity or earnout

- Whether rollover equity is required in a PE deal

- Your post-close role and time commitment

- Escrow size, indemnification, and downside risk

I’ve seen founders accept higher nominal prices with worse terms and walk away with less cash, more stress, and less freedom. This is where experienced advisors and lawyers are invaluable. They help you see past the headline and negotiate what really matters.

Final Thoughts

Selling your SaaS company isn’t a single decision. It’s the outcome of years of choices around growth, team, systems, and discipline.

The founders who get great exits don’t get lucky. They build businesses that are durable, transferable, and understandable to outsiders. They prepare earlier than feels necessary. And they surround themselves with people who have done this before.

If you’re already doing $5M+ ARR and thinking about an exit someday, the work starts now. If you’re earlier, that’s fine too. Just know that every system you build today either expands or limits your future options.

The goal isn’t just to build a company.

It’s to build a company someone else will pay a premium to own.